Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at MarineMax (NYSE: HZO) and its peers.

At their essence, cars and boats get you from point A to point B, but the former is usually a necessity in everyday life while the latter is a luxury or leisure product. The retailers that sell these vehicles therefore cater to different needs and populations. There are also retailers that may not sell cars and boats themselves but the parts and accessories needed to keep these complex machines in tip top shape.

The 12 automotive and marine retail stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.5%.

While some automotive and marine retail stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 4.8% since the latest earnings results.

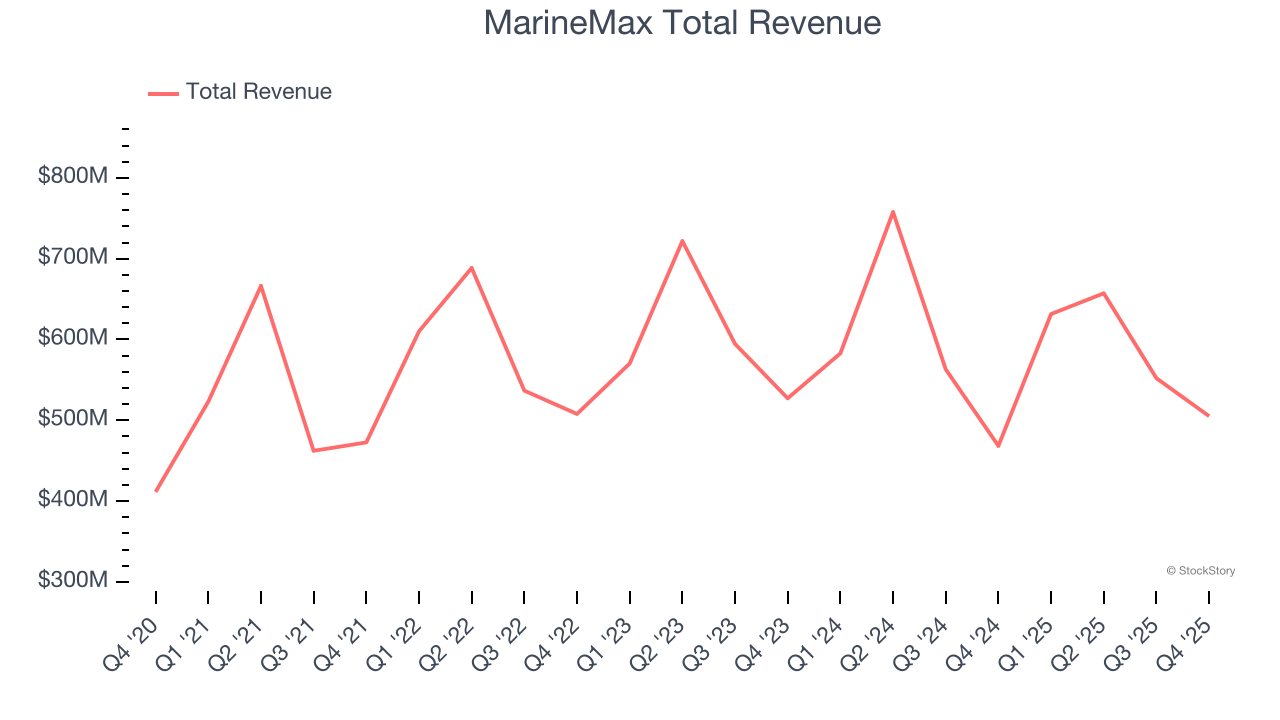

Best Q4: MarineMax (NYSE: HZO)

Appropriately headquartered in Clearwater, Florida, MarineMax (NYSE: HZO) sells boats, yachts, and other marine products.

MarineMax reported revenues of $505.2 million, up 7.8% year on year. This print exceeded analysts’ expectations by 4.6%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ gross margin estimates.

“As anticipated, retail margin pressure persisted across the recreational boating industry in the December quarter, reflecting continued uncertainty and competitive dynamics, including elevated promotional activity, as the industry continues to right-size inventory,” said Brett McGill, CEO and President of MarineMax.

MarineMax scored the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 16.4% since reporting and currently trades at $31.28.

Read our full report on MarineMax here, it’s free.

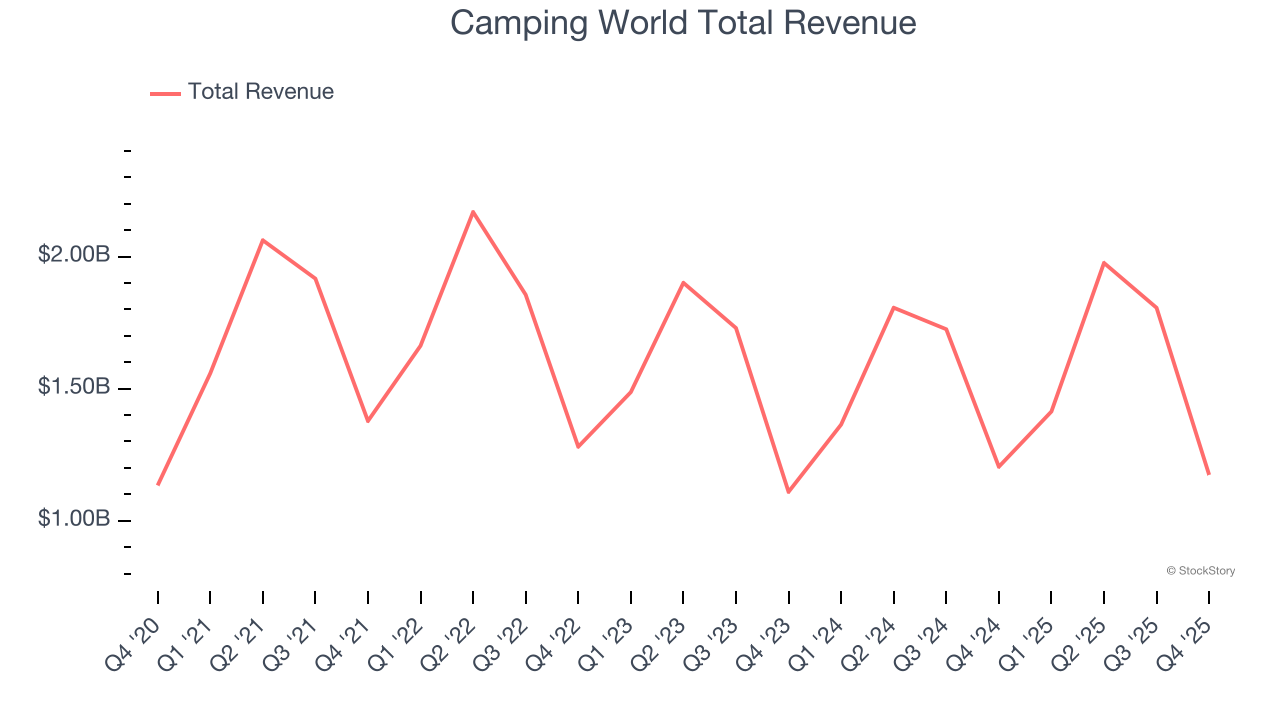

Camping World (NYSE: CWH)

Founded in 1966 as a single recreational vehicle (RV) dealership, Camping World (NYSE: CWH) still sells RVs along with boats and general merchandise for outdoor activities.

Camping World reported revenues of $1.17 billion, down 2.6% year on year, outperforming analysts’ expectations by 1.2%. The business performed better than its peers, but it was unfortunately a softer quarter with a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ gross margin estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 16.3% since reporting. It currently trades at $9.08.

Is now the time to buy Camping World? Access our full analysis of the earnings results here, it’s free.

Slowest Q4: AutoNation (NYSE: AN)

With a vast network of over 300 locations strategically concentrated in America's Sunbelt region, AutoNation (NYSE: AN) operates one of America's largest networks of automotive dealerships, selling new and used vehicles, parts, and services across multiple brands.

AutoNation reported revenues of $6.93 billion, down 3.9% year on year, falling short of analysts’ expectations by 3.6%. It was a softer quarter as it posted a significant miss of analysts’ EBITDA estimates and a miss of analysts’ revenue estimates.

AutoNation delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 3.8% since the results and currently trades at $196.36.

Read our full analysis of AutoNation’s results here.

OneWater (NASDAQ: ONEW)

A public company since early 2020, OneWater Marine (NASDAQ: ONEW) sells boats, yachts, and other marine products.

OneWater reported revenues of $380.6 million, up 1.3% year on year. This print was in line with analysts’ expectations. Overall, it was a strong quarter as it also put up a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

OneWater pulled off the highest full-year guidance raise among its peers. The stock is down 10.7% since reporting and currently trades at $11.80.

Read our full, actionable report on OneWater here, it’s free.

Monro (NASDAQ: MNRO)

Started as a single location in Rochester, New York, Monro (NASDAQ: MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Monro reported revenues of $293.4 million, down 4% year on year. This result came in 0.6% below analysts' expectations. Aside from that, it was a strong quarter as it recorded a beat of analysts’ EPS estimates and a decent beat of analysts’ EBITDA estimates.

The stock is up 10.9% since reporting and currently trades at $22.21.

Read our full, actionable report on Monro here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.