What a time it’s been for Nature's Sunshine. In the past six months alone, the company’s stock price has increased by a massive 66.9%, reaching $27.54 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Nature's Sunshine, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Nature's Sunshine Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about Nature's Sunshine. Here are three reasons there are better opportunities than NATR and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

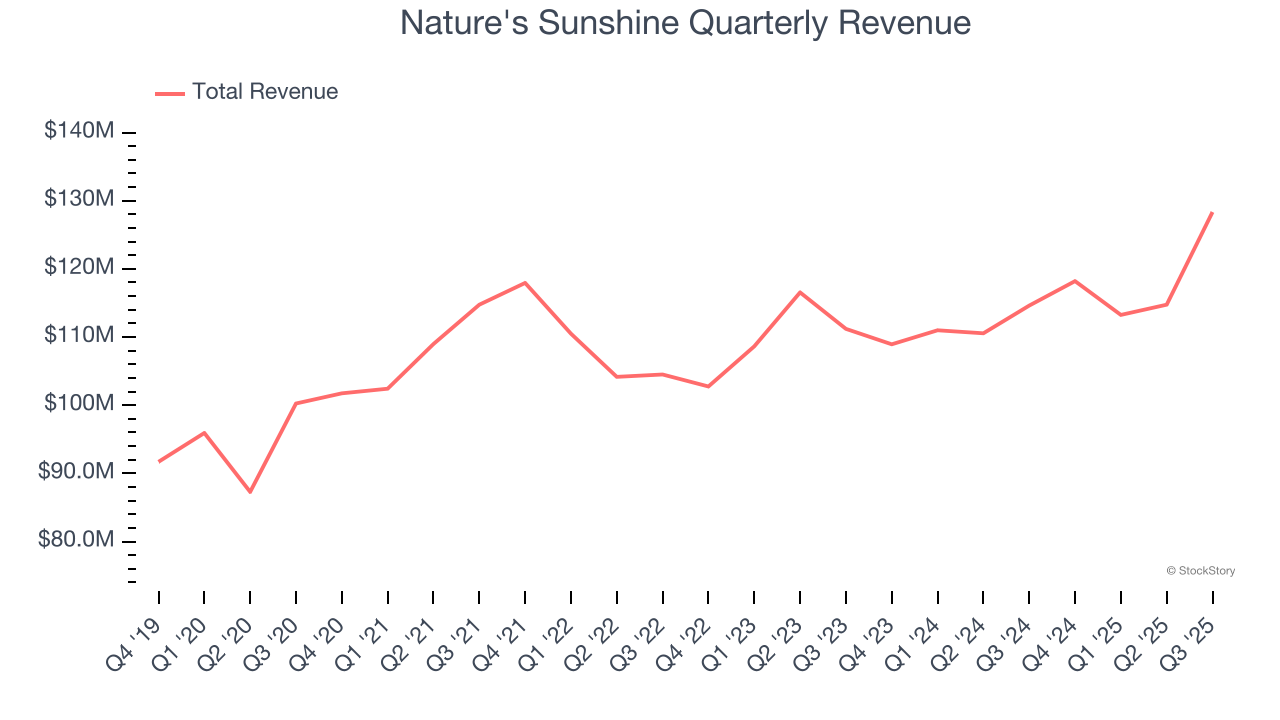

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Nature's Sunshine’s 2.8% annualized revenue growth over the last three years was sluggish. This was below our standards.

2. Fewer Distribution Channels Limit its Ceiling

With $474.5 million in revenue over the past 12 months, Nature's Sunshine is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Nature's Sunshine’s revenue to rise by 3.1%, close to This projection doesn't excite us and implies its newer products will not lead to better top-line performance yet.

Final Judgment

Nature's Sunshine isn’t a terrible business, but it doesn’t pass our bar. After the recent rally, the stock trades at 29.2× forward P/E (or $27.54 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d recommend looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.