What a fantastic six months it’s been for Coursera. Shares of the company have skyrocketed 40.8%, hitting $11.24. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Coursera, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Coursera Not Exciting?

Despite the momentum, we're sitting this one out for now. Here are three reasons we avoid COUR and a stock we'd rather own.

1. Customer Spending Decreases, Engagement Falling?

Average revenue per customer (ARPC) is a critical metric to track because it measures how much the average customer spends. ARPC is also a key indicator of how valuable its customers are (and can be over time).

Coursera’s ARPC fell over the last two years, averaging 6.4% annual declines. This isn’t great, but the increase in paying users

is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Coursera tries boosting ARPC by taking a more aggressive approach to monetization, it’s unclear whether customers can continue growing at the current pace.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Coursera’s revenue to rise by 5.6%, a deceleration versus This projection doesn't excite us and suggests its products and services will see some demand headwinds.

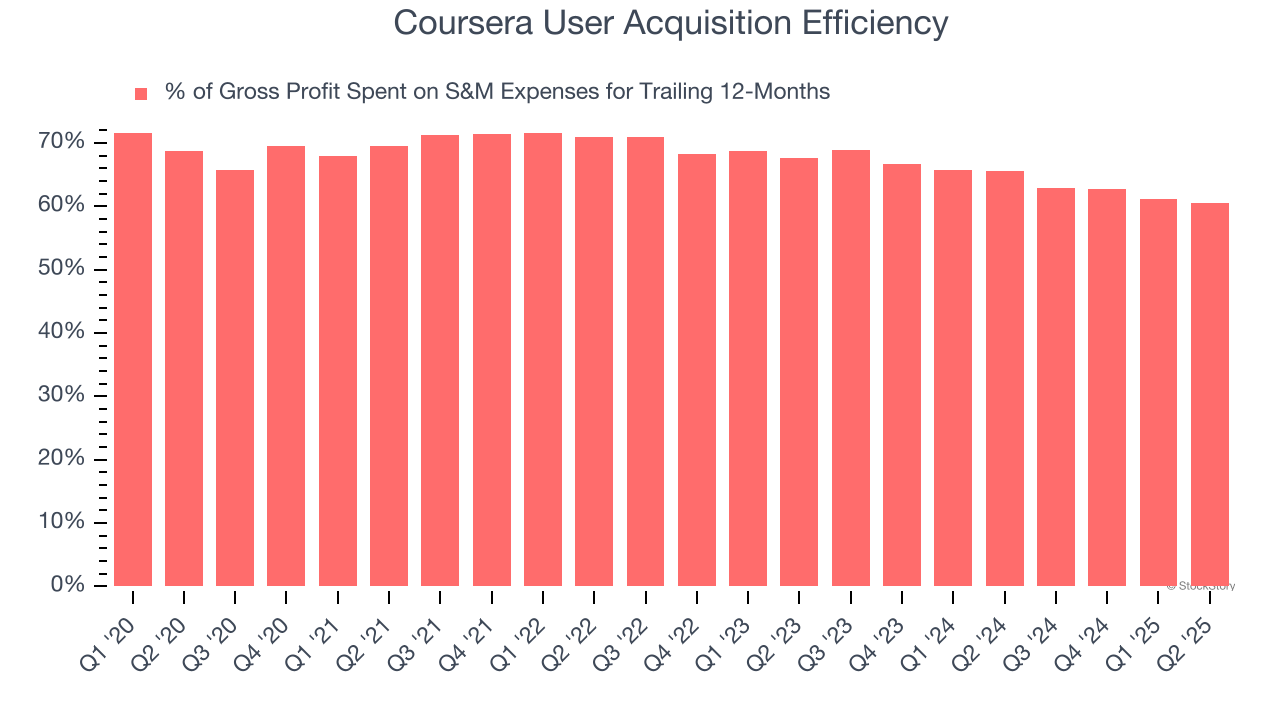

3. Poor Marketing Efficiency Drains Profits

Consumer internet businesses like Coursera grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s very expensive for Coursera to acquire new users as the company has spent 60.5% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between Coursera and its peers.

Final Judgment

Coursera isn’t a terrible business, but it isn’t one of our picks. After the recent rally, the stock trades at 34.9× forward EV/EBITDA (or $11.24 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.