Since October 2024, Braze has been in a holding pattern, floating around $30.70.

Is now the time to buy BRZE? Or does the price properly account for its business quality and fundamentals? Find out in our full research report, it’s free.

Why Does BRZE Stock Spark Debate?

Founded in 2011 after the co-founders met at NYC Disrupt Hackathon, Braze (NASDAQ: BRZE) is a customer engagement software platform that allows brands to connect with customers through data-driven and contextual marketing campaigns.

Two Things to Like:

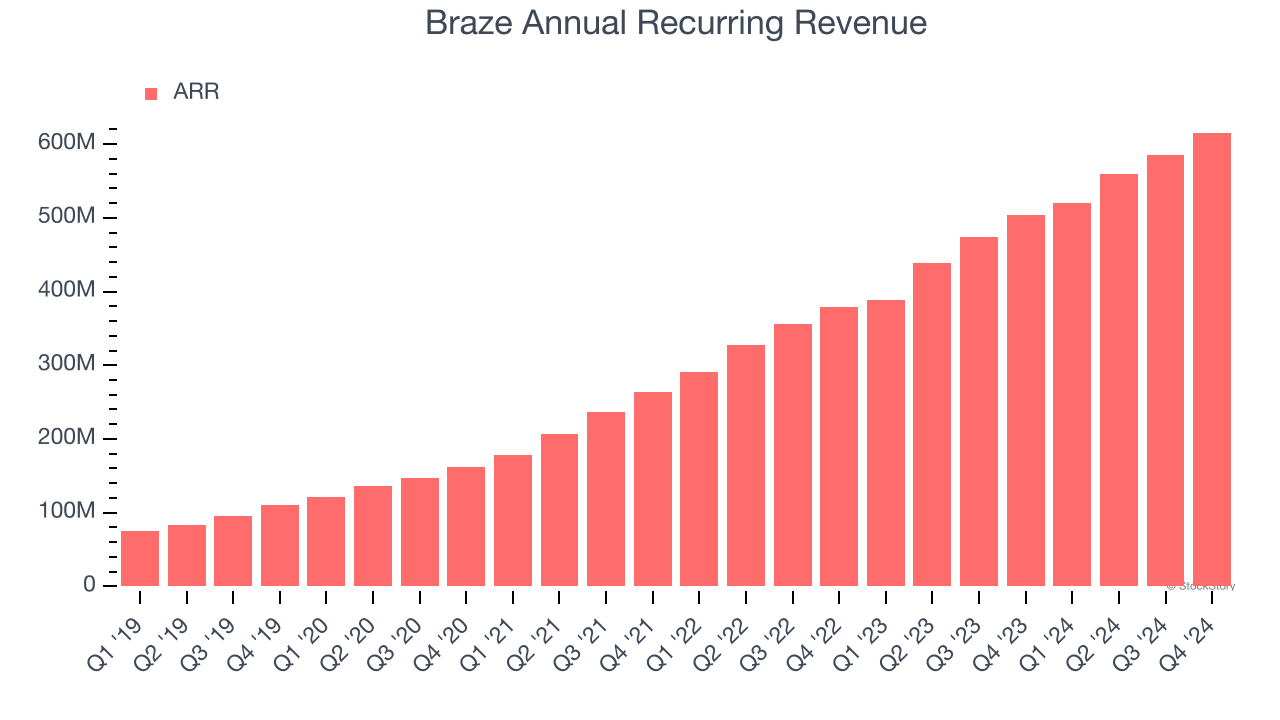

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Braze’s ARR punched in at $615.6 million in Q4, and over the last four quarters, its year-on-year growth averaged 26.8%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Braze a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

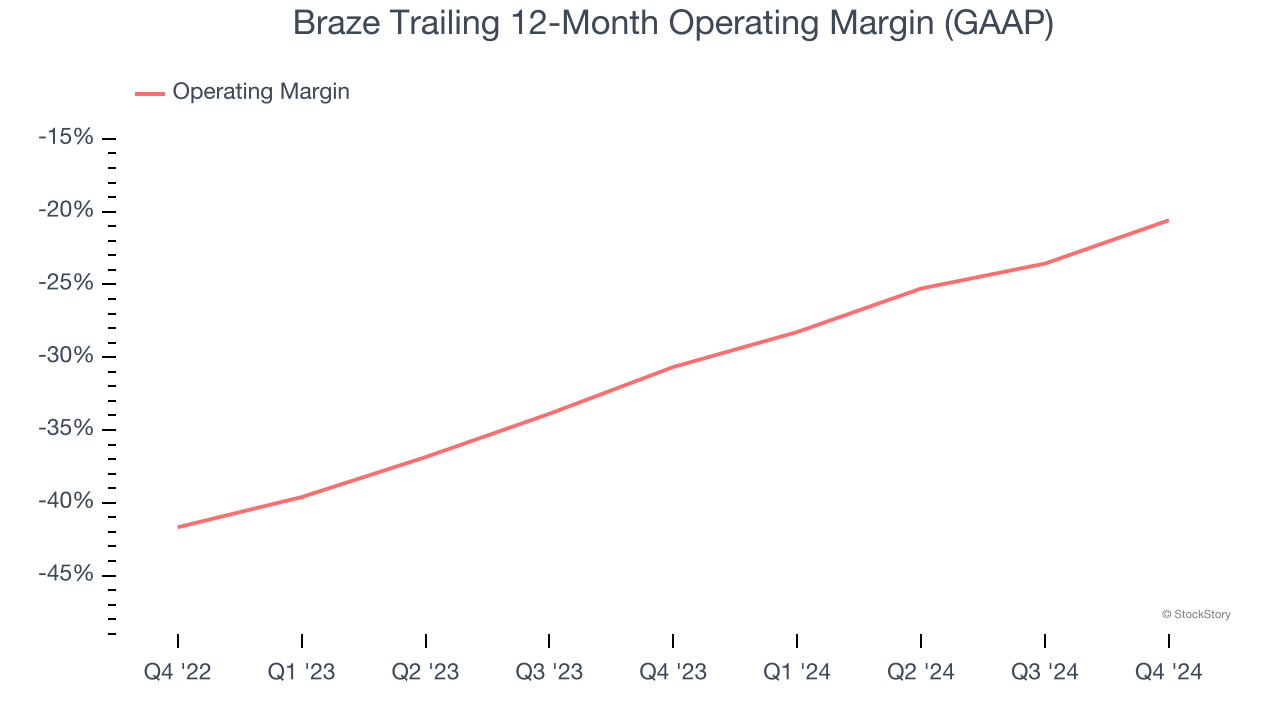

2. Operating Margin Rising, Profits Up

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Over the last year, Braze’s expanding sales gave it operating leverage as its margin rose by 10.1 percentage points. Although its operating margin for the trailing 12 months was negative 20.6%, we’re confident it can one day reach sustainable profitability.

One Reason to be Careful:

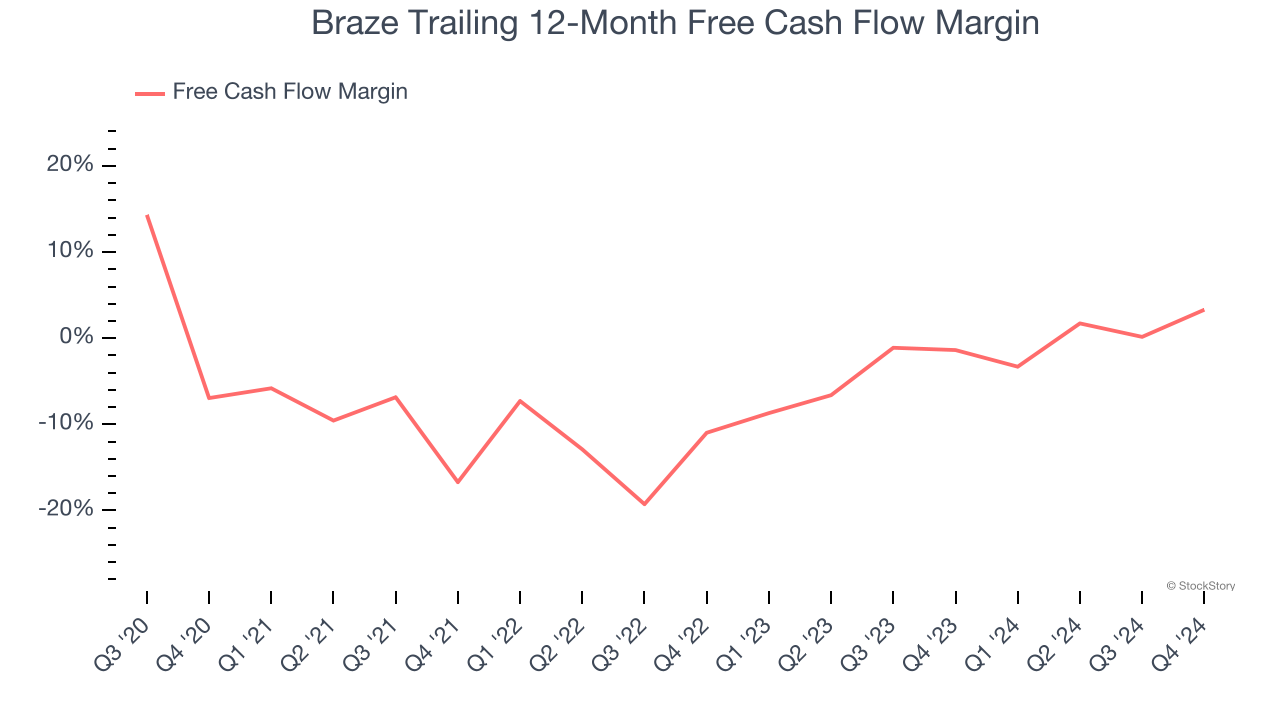

Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Braze has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.3%, subpar for a software business.

Final Judgment

Braze’s positive characteristics outweigh the negatives, but at $30.70 per share (or 4.7× forward price-to-sales), is now the right time to buy the stock? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Braze

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.