Amalgamated Financial has been treading water for the past six months, recording a small loss of 1.4% while holding steady at $26.73. The stock also fell short of the S&P 500’s 24.7% gain during that period.

Is now the time to buy AMAL? Find out in our full research report, it’s free.

Why Are We Positive On Amalgamated Financial?

Founded in 1923 by labor unions seeking a financial institution aligned with worker values, Amalgamated Financial (NASDAQGM:AMAL) operates a values-oriented bank that provides commercial banking, trust services, and investment management to socially responsible organizations and individuals.

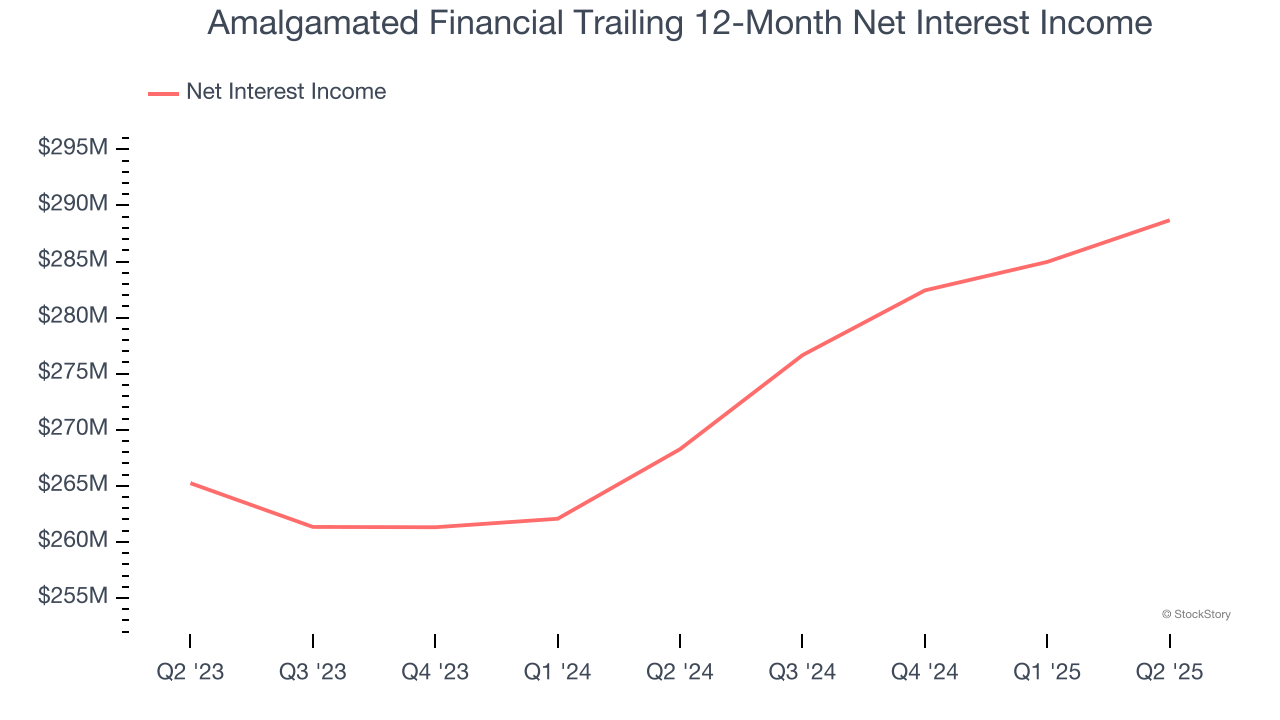

1. Net Interest Income Drives Additional Growth Opportunities

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Amalgamated Financial’s net interest income has grown at a 10% annualized rate over the last five years, a step above the broader banking industry and in line with its total revenue.

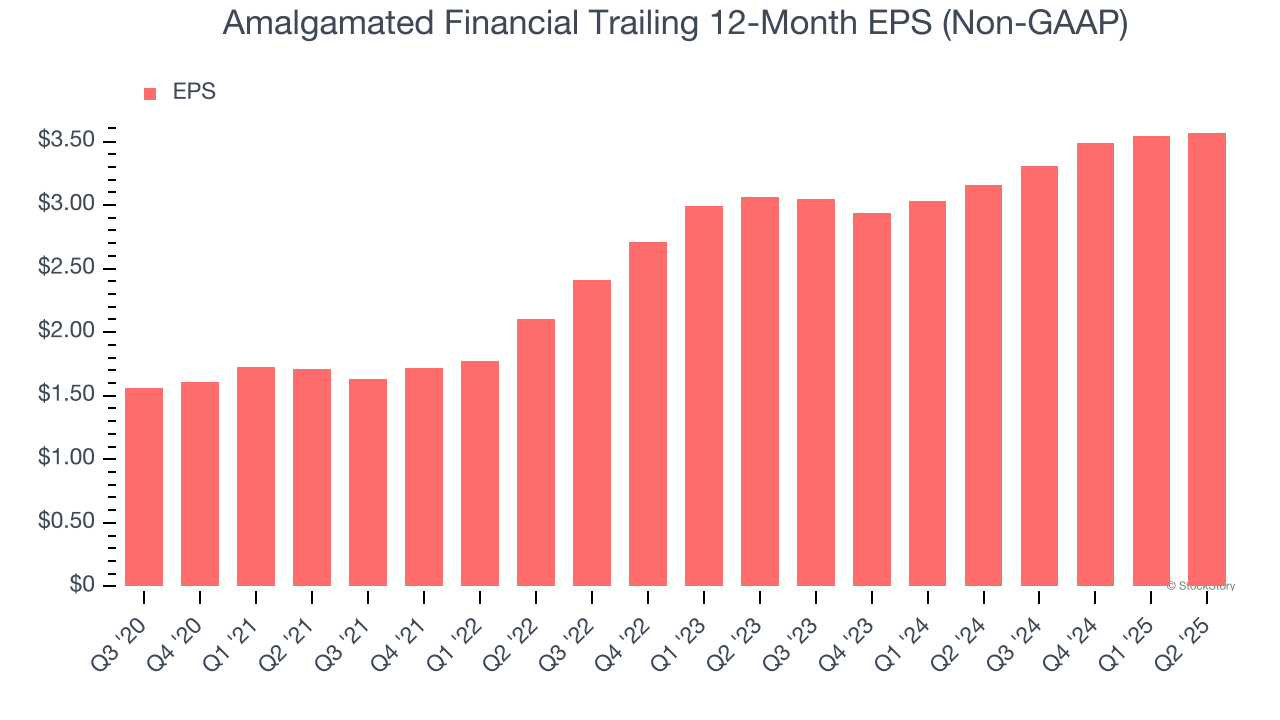

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Amalgamated Financial’s EPS grew at an astounding 21.1% compounded annual growth rate over the last five years, higher than its 9.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

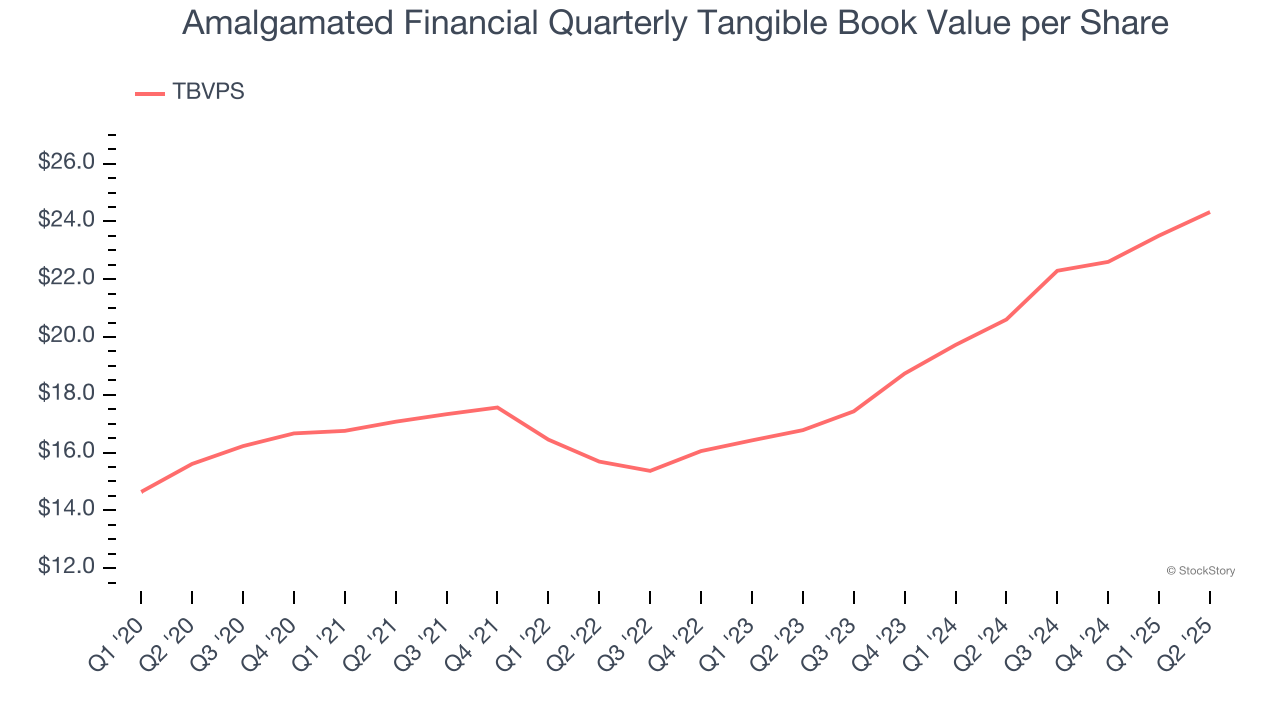

3. Growing TBVPS Reflects Strong Asset Base

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Amalgamated Financial’s TBVPS increased by 9.3% annually over the last five years, and growth has recently accelerated as TBVPS grew at an incredible 20.4% annual clip over the past two years (from $16.78 to $24.33 per share).

Final Judgment

These are just a few reasons Amalgamated Financial is a rock-solid business worth owning. With its shares lagging the market recently, the stock trades at 1× forward P/B (or $26.73 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.