Nicolet Bankshares has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 7.7% to $141.55 per share while the index has gained 9.5%.

Is now a good time to buy NIC? Find out in our full research report, it’s free.

Why Are We Positive On NIC?

Starting as Green Bay Financial Corporation in 2000 before rebranding in 2002, Nicolet Bankshares (NYSE: NIC) is a regional bank holding company that provides commercial, agricultural, and consumer banking services primarily in Wisconsin, Michigan, and Minnesota.

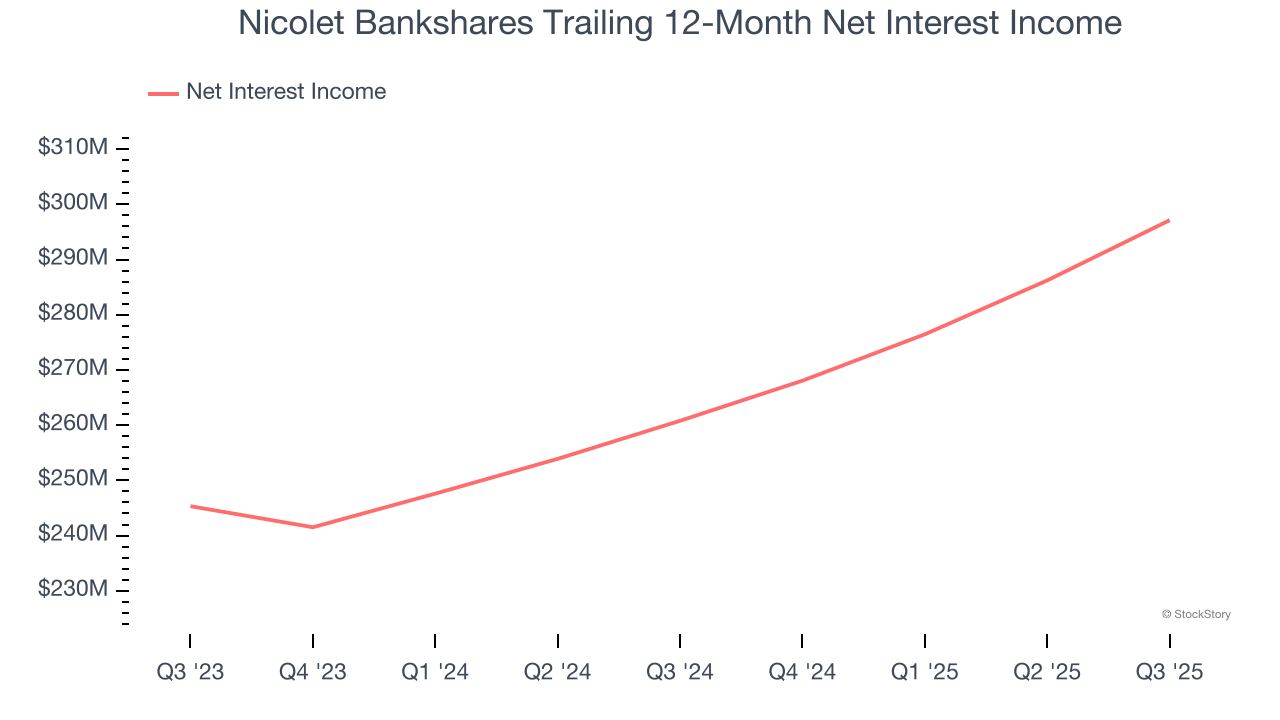

1. Net Interest Income Skyrockets, Fueling Growth Opportunities

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Nicolet Bankshares’s net interest income has grown at a 18.8% annualized rate over the last five years, much better than the broader banking industry and faster than its total revenue.

2. Projected Net Interest Income Growth Is Remarkable

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Nicolet Bankshares’s net interest income to rise by 60.4%, an improvement versus its 10.1% annualized growth for the past two years.

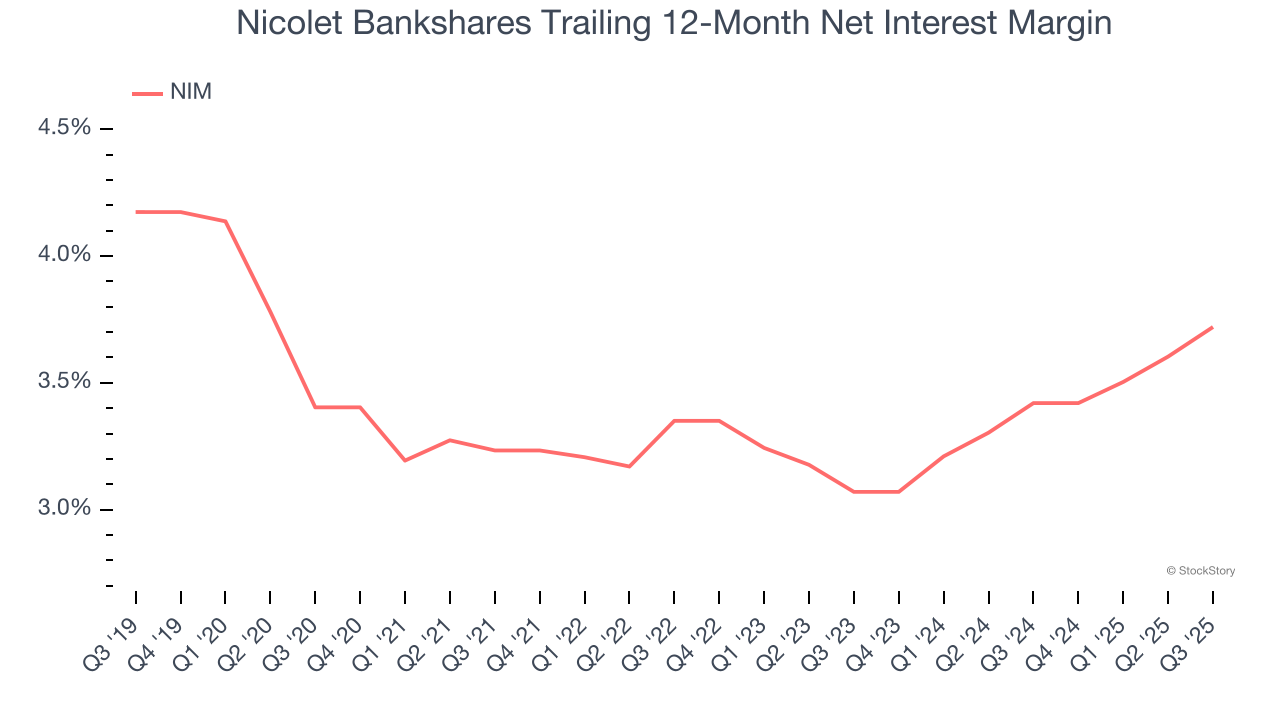

3. Increasing Net Interest Margin Juices Financials

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Nicolet Bankshares’s net interest margin averaged 3.6%, climbing by 65 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

Final Judgment

These are just a few reasons Nicolet Bankshares is a rock-solid business worth owning, but at $141.55 per share (or 1.7× forward P/B), is now the right time to buy the stock? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Nicolet Bankshares

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.