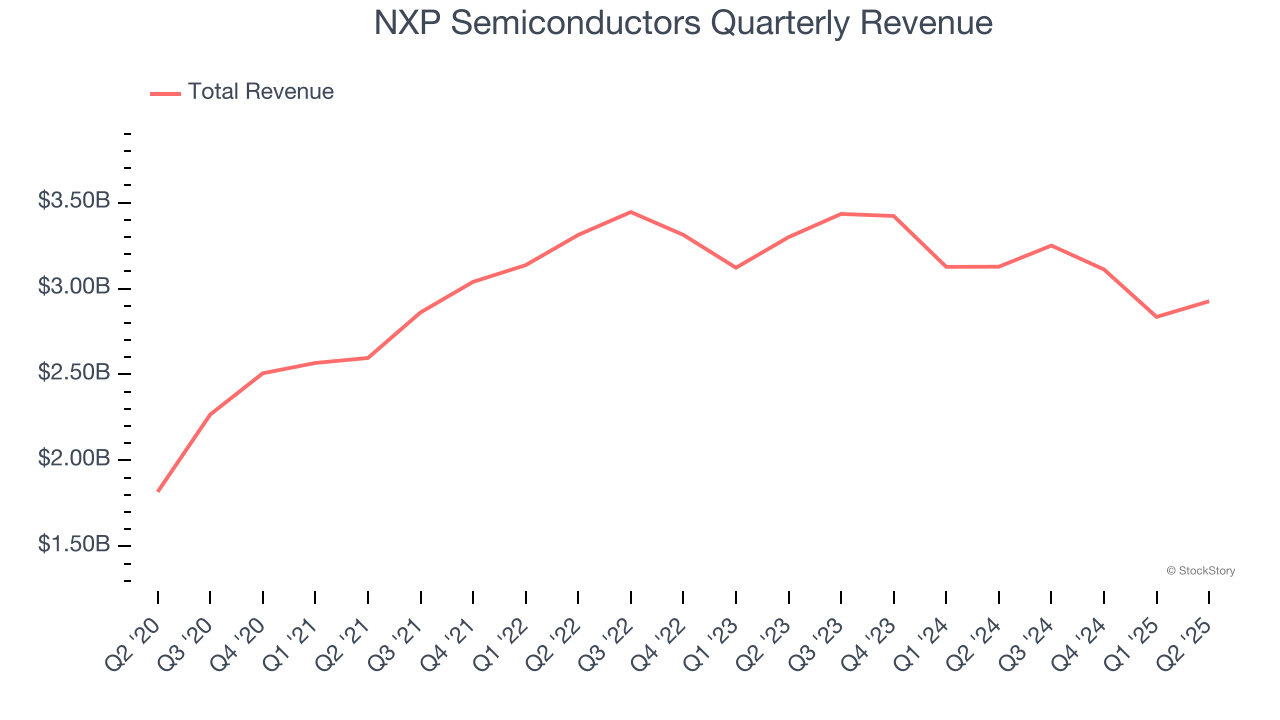

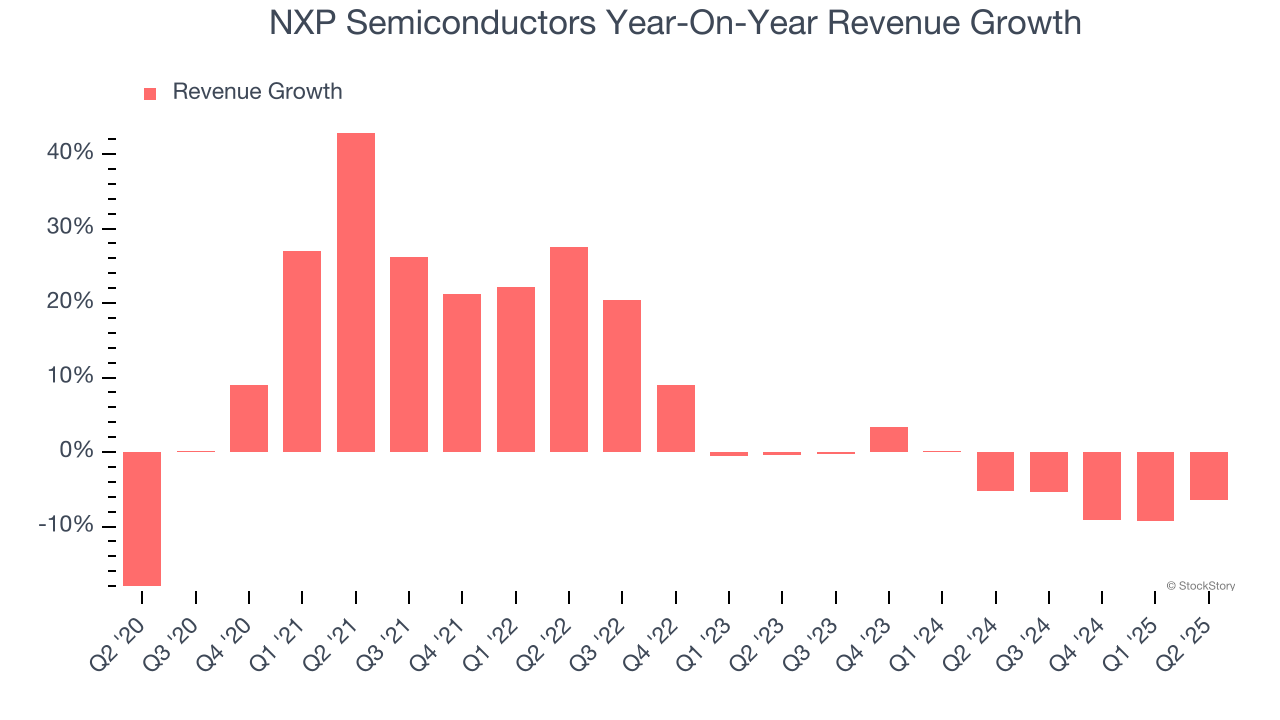

Chip manufacturer NXP Semiconductors (NASDAQ: NXPI) reported Q2 CY2025 results topping the market’s revenue expectations, but sales fell by 6.4% year on year to $2.93 billion. Guidance for next quarter’s revenue was optimistic at $3.15 billion at the midpoint, 2.2% above analysts’ estimates. Its non-GAAP profit of $2.72 per share was 2.3% above analysts’ consensus estimates.

Is now the time to buy NXP Semiconductors? Find out by accessing our full research report, it’s free.

NXP Semiconductors (NXPI) Q2 CY2025 Highlights:

- Revenue: $2.93 billion vs analyst estimates of $2.9 billion (6.4% year-on-year decline, 0.8% beat)

- Adjusted EPS: $2.72 vs analyst estimates of $2.66 (2.3% beat)

- Revenue Guidance for Q3 CY2025 is $3.15 billion at the midpoint, above analyst estimates of $3.08 billion

- Adjusted EPS guidance for Q3 CY2025 is $3.10 at the midpoint, above analyst estimates of $3.04

- Operating Margin: 23.5%, down from 28.7% in the same quarter last year

- Free Cash Flow Margin: 23.8%, up from 18.4% in the same quarter last year

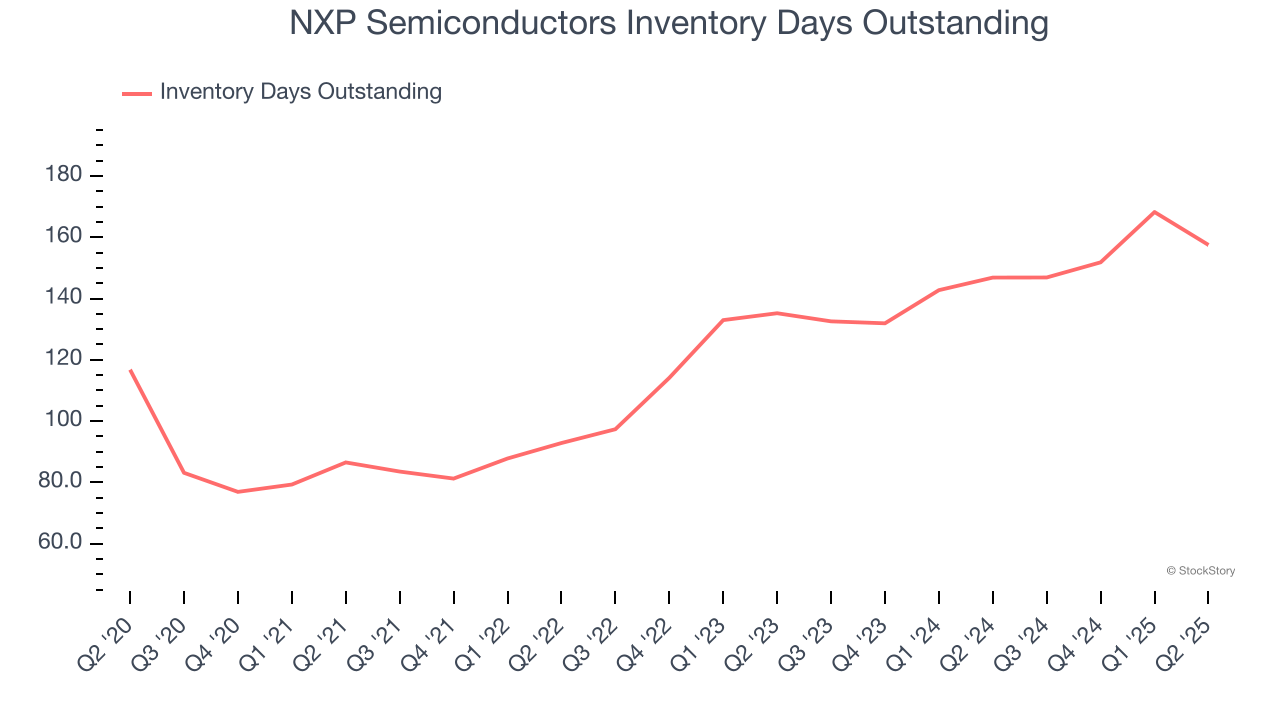

- Inventory Days Outstanding: 158, down from 168 in the previous quarter

- Market Capitalization: $57.07 billion

EINDHOVEN, The Netherlands, July 21, 2025 (GLOBE NEWSWIRE) -- NXP Semiconductors N.V. (NASDAQ: NXPI) today reported financial results for the second quarter, which ended June 29, 2025. “NXP delivered quarterly revenue of $2.93 billion, above the midpoint of our guidance, with all our focus end-markets performing above expectations. Our guidance for the third quarter reflects the combination of an emerging cyclical improvement in NXP's core end markets as well as the performance of our company specific growth drivers. We continue to drive solid profitability and earnings, by strengthening our competitive portfolio and by aligning our wafer fabrication footprint consistent with our hybrid manufacturing strategy,” said Kurt Sievers, NXP Chief Executive Officer.

Company Overview

Spun off from Dutch electronics giant Philips in 2006, NXP Semiconductors (NASDAQ: NXPI) is a designer and manufacturer of chips used in autos, industrial manufacturing, mobile devices, and communications infrastructure.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, NXP Semiconductors’s 7.6% annualized revenue growth over the last five years was decent. Its growth was slightly above the average semiconductor company and shows its offerings resonate with customers. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. NXP Semiconductors’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 4.1% over the last two years.

This quarter, NXP Semiconductors’s revenue fell by 6.4% year on year to $2.93 billion but beat Wall Street’s estimates by 0.8%. Despite the beat, the drop in sales could mean that the current downcycle is deepening. Company management is currently guiding for a 3.1% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, NXP Semiconductors’s DIO came in at 158, which is 41 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

Key Takeaways from NXP Semiconductors’s Q2 Results

It was great to see a material improvement in NXP Semiconductors’s inventory levels. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. Revenues and operating margin was down year-on-year, but overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 4.8% to $217.49 immediately following the results.

So do we think NXP Semiconductors is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.