Curtiss-Wright currently trades at $325.36 per share and has shown little upside over the past six months, posting a small loss of 1%.

Given the underwhelming price action, is now a good time to buy CW? Or should investors expect a bumpy road ahead? Find out in our full research report, it’s free.

Why Is Curtiss-Wright a Good Business?

Formed from a merger of 12 companies, Curtiss-Wright (NYSE: CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

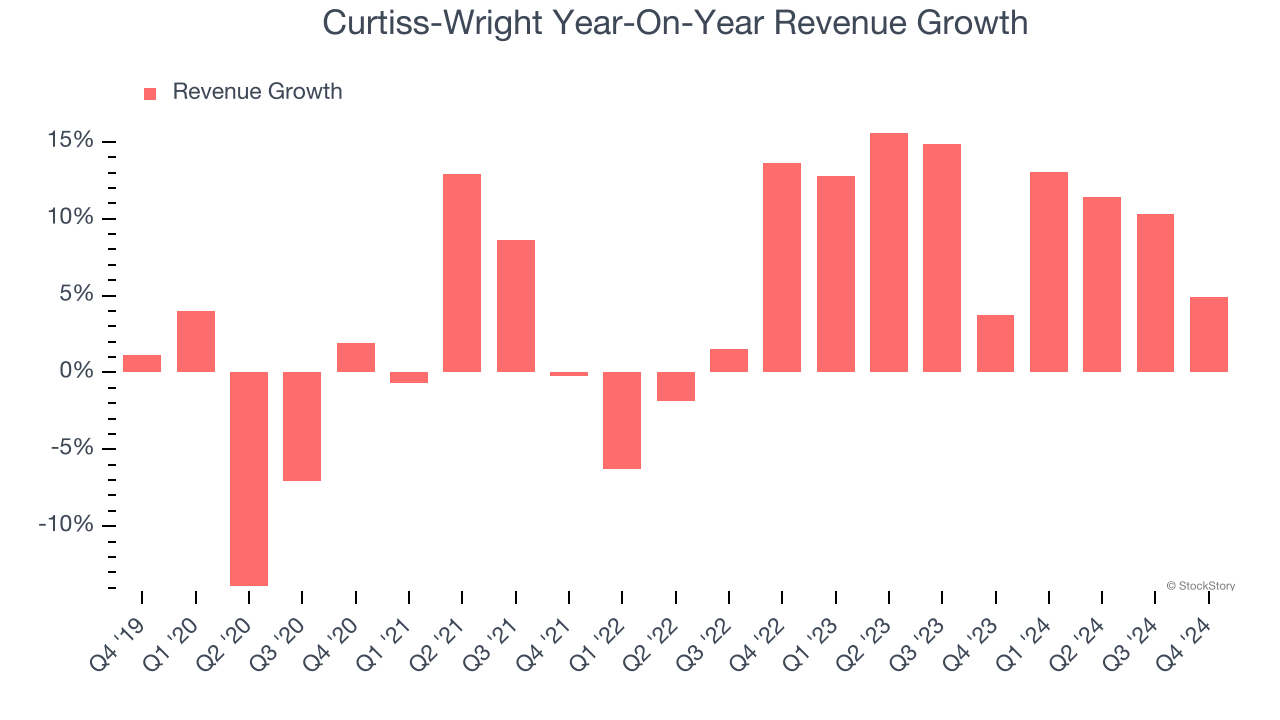

1. Encouraging Short-Term Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Curtiss-Wright’s annualized revenue growth of 10.5% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

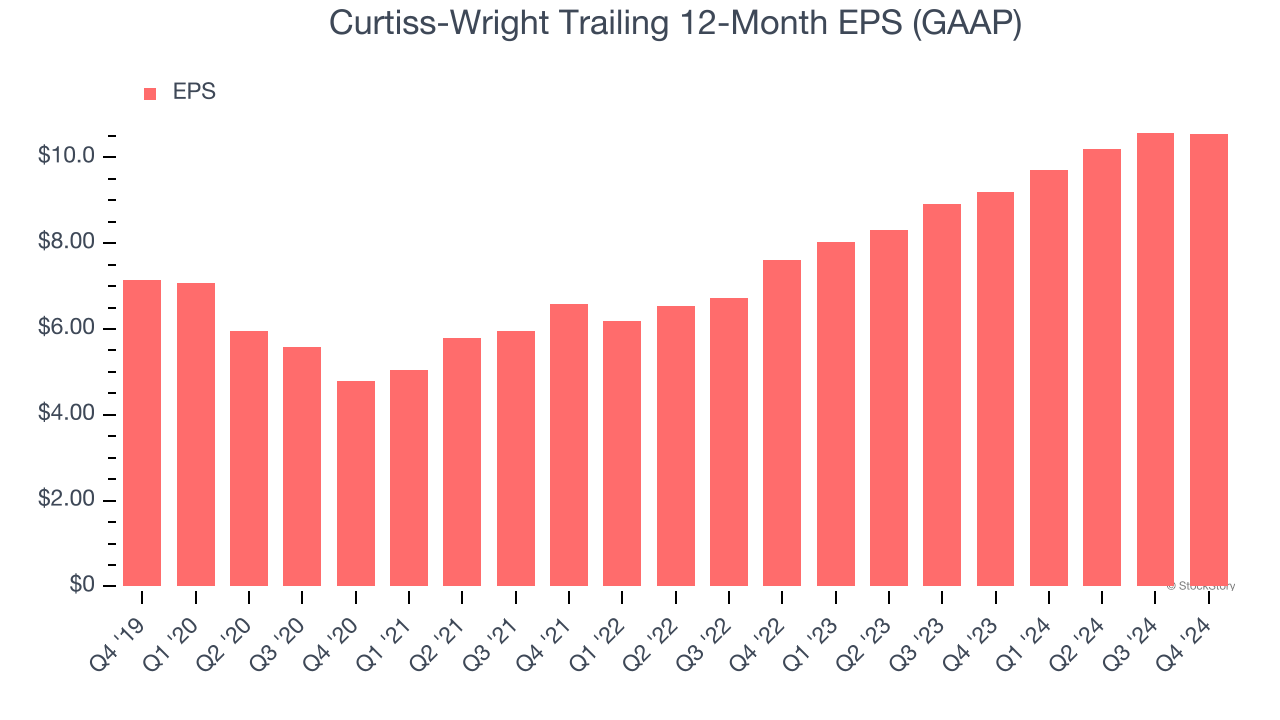

2. EPS Moving Up Steadily

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Curtiss-Wright’s EPS grew at a decent 8.1% compounded annual growth rate over the last five years, higher than its 4.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

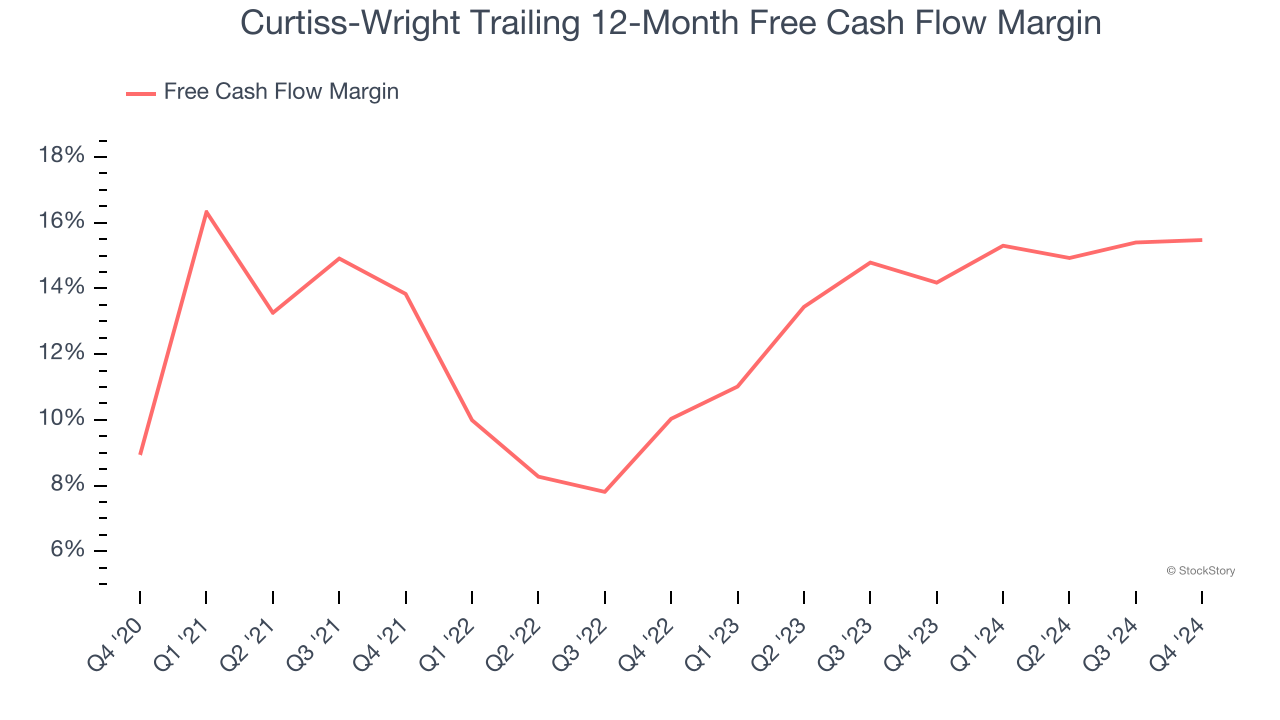

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Curtiss-Wright’s margin expanded by 6.5 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Curtiss-Wright’s free cash flow margin for the trailing 12 months was 15.5%.

Final Judgment

These are just a few reasons Curtiss-Wright is a rock-solid business worth owning, but at $325.36 per share (or 27.1× forward price-to-earnings), is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Curtiss-Wright

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.