Over the past six months, Lam Research’s shares (currently trading at $74.44) have posted a disappointing 8.8% loss while the S&P 500 was down 1.4%. This may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for LRCX? Find out in our full research report, it’s free.

Why Does LRCX Stock Spark Debate?

Founded in 1980 by David Lam, the man who pioneered semiconductor etching technology, Lam Research (NASDAQ: LRCX) is one of the leading providers of wafer fabrication equipment used to make semiconductors.

Two Positive Attributes:

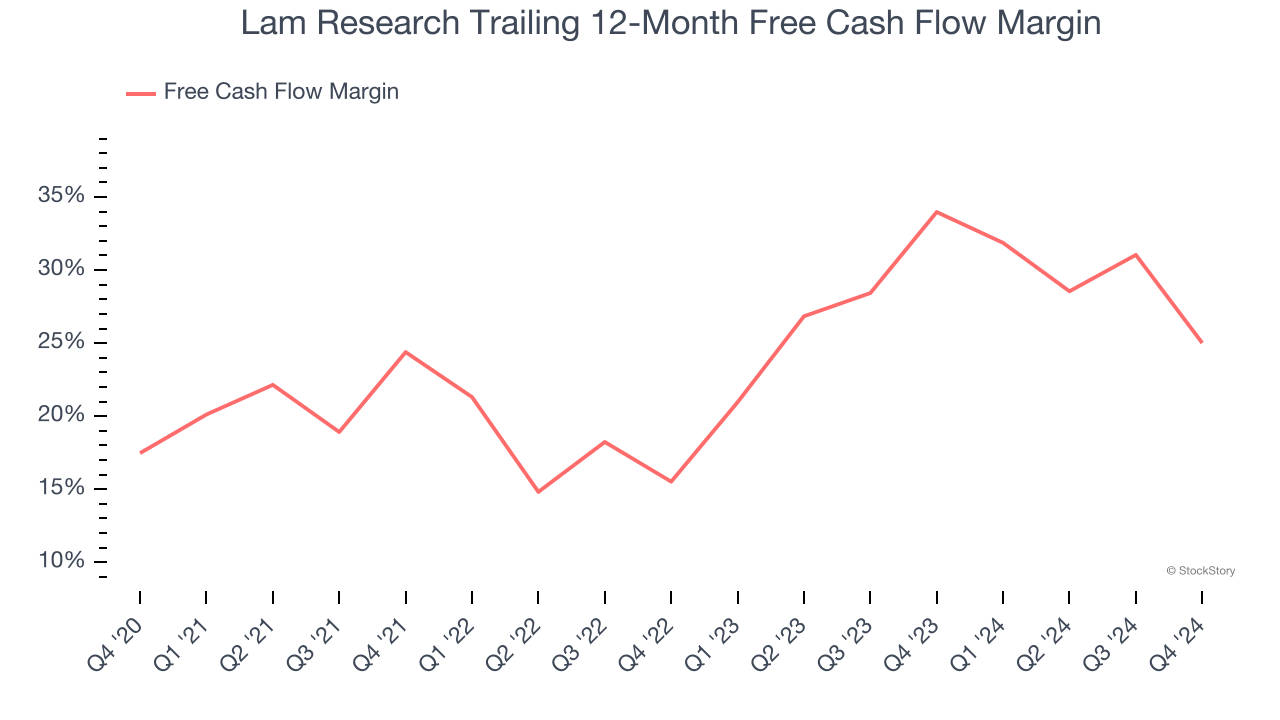

1. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Lam Research has shown terrific cash profitability, and if sustainable, puts it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the semiconductor sector, averaging 29.2% over the last two years.

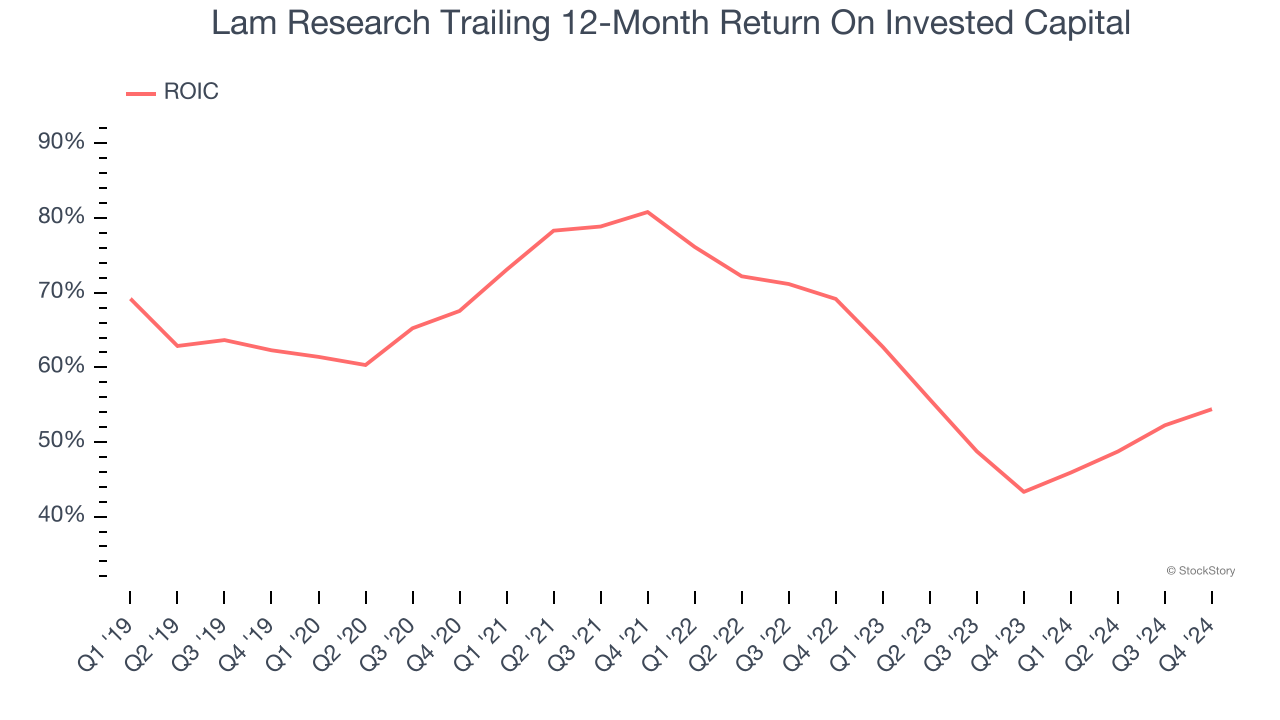

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Lam Research’s five-year average ROIC was 63.1%, placing it among the best semiconductor companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to be Careful:

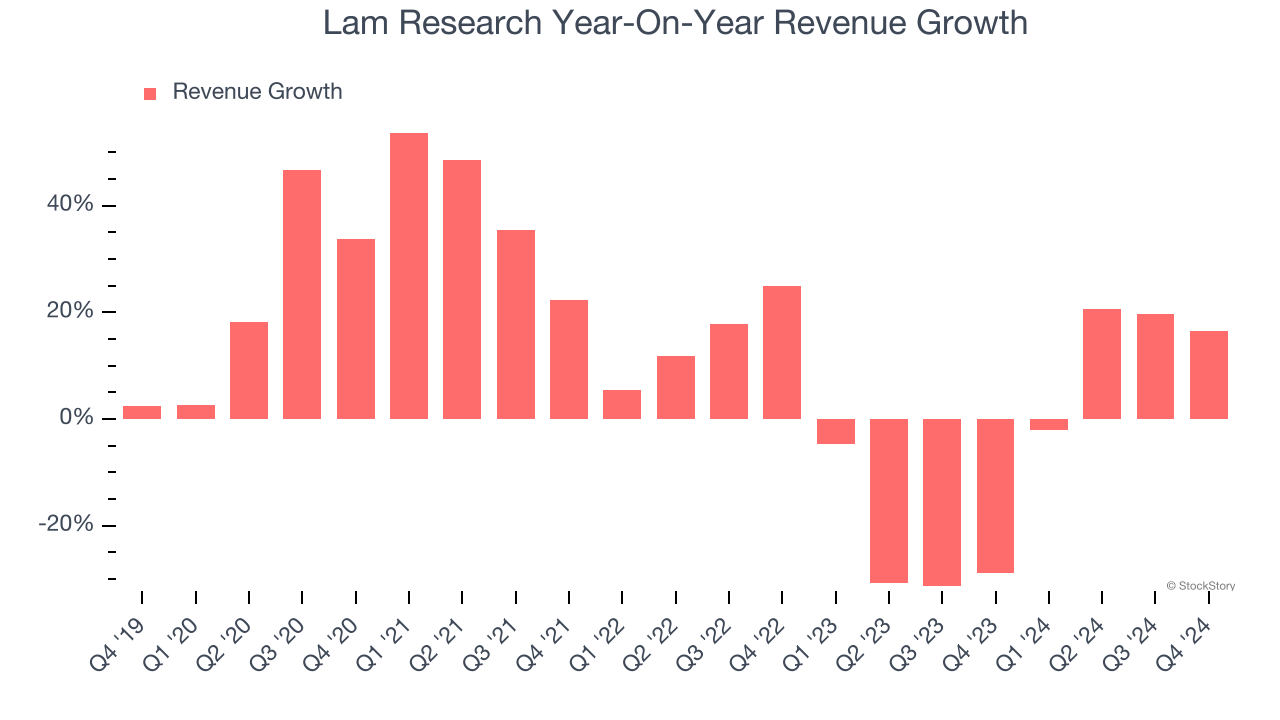

Revenue Tumbling Downwards

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Lam Research’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 7.8% over the last two years.

Final Judgment

Lam Research’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 20.4× forward price-to-earnings (or $74.44 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Lam Research

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.