Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Byrna (NASDAQ: BYRN) and the best and worst performers in the aerospace and defense industry.

Emissions and automation are important in aerospace, so companies that boast advances in these areas can take market share. On the defense side, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression toward Taiwan–have highlighted the need for consistent or even elevated defense spending. As for challenges, demand for aerospace and defense products can ebb and flow with economic cycles and national defense budgets, which are unpredictable and particularly painful for companies with high fixed costs.

The 31 aerospace and defense stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was 1.8% above.

In light of this news, share prices of the companies have held steady as they are up 1.7% on average since the latest earnings results.

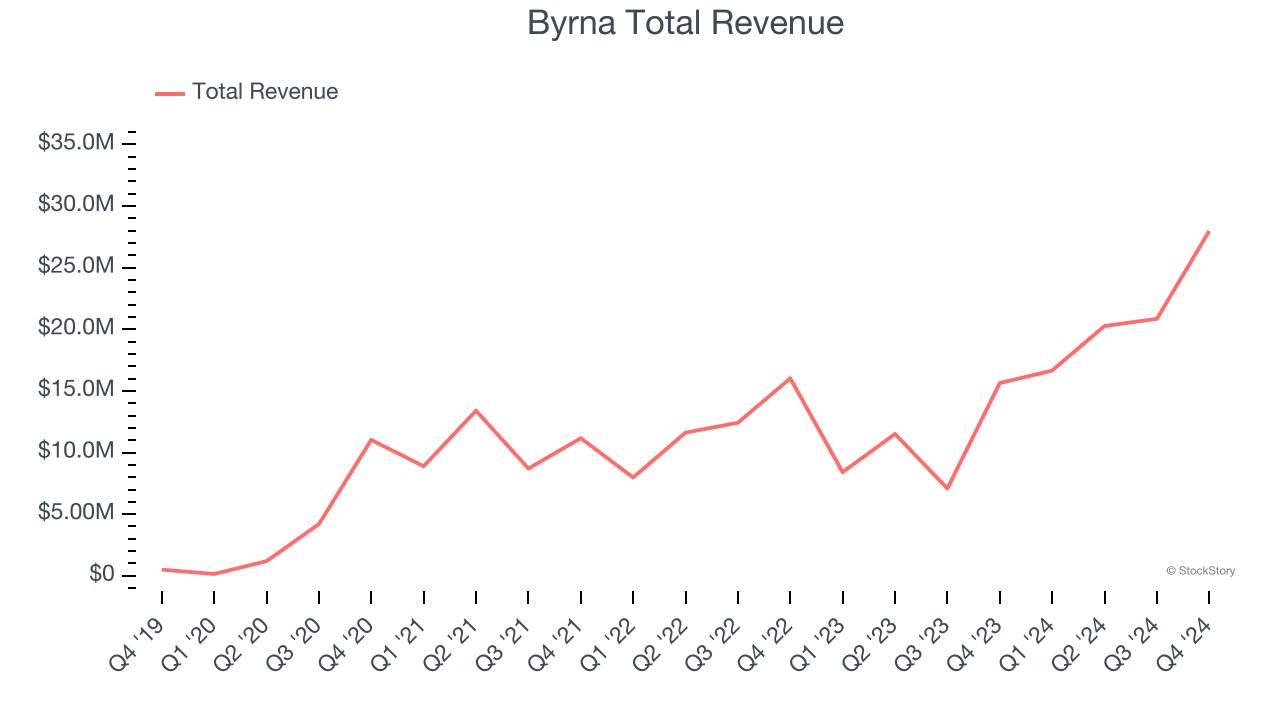

Byrna (NASDAQ: BYRN)

Providing civilians with tools to disable, disarm, and deter would-be assailants, Byrna (NASDAQ: BYRN) is a provider of non-lethal weapons.

Byrna reported revenues of $27.98 million, up 78.9% year on year. This print was in line with analysts’ expectations, and overall, it was an exceptional quarter for the company with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Management CommentaryByrna CEO Bryan Ganz stated: “The fourth quarter was the culmination of a remarkable year for Byrna. We successfully generated a record $28.0 million in revenue while also expanding our gross margins to 62.8%. This success allowed us to deliver a 101% increase in revenue from the full year 2023 to 2024 and underscores the overall growth in brand recognition and normalization of the less-lethal space.

The stock is down 30.6% since reporting and currently trades at $19.08.

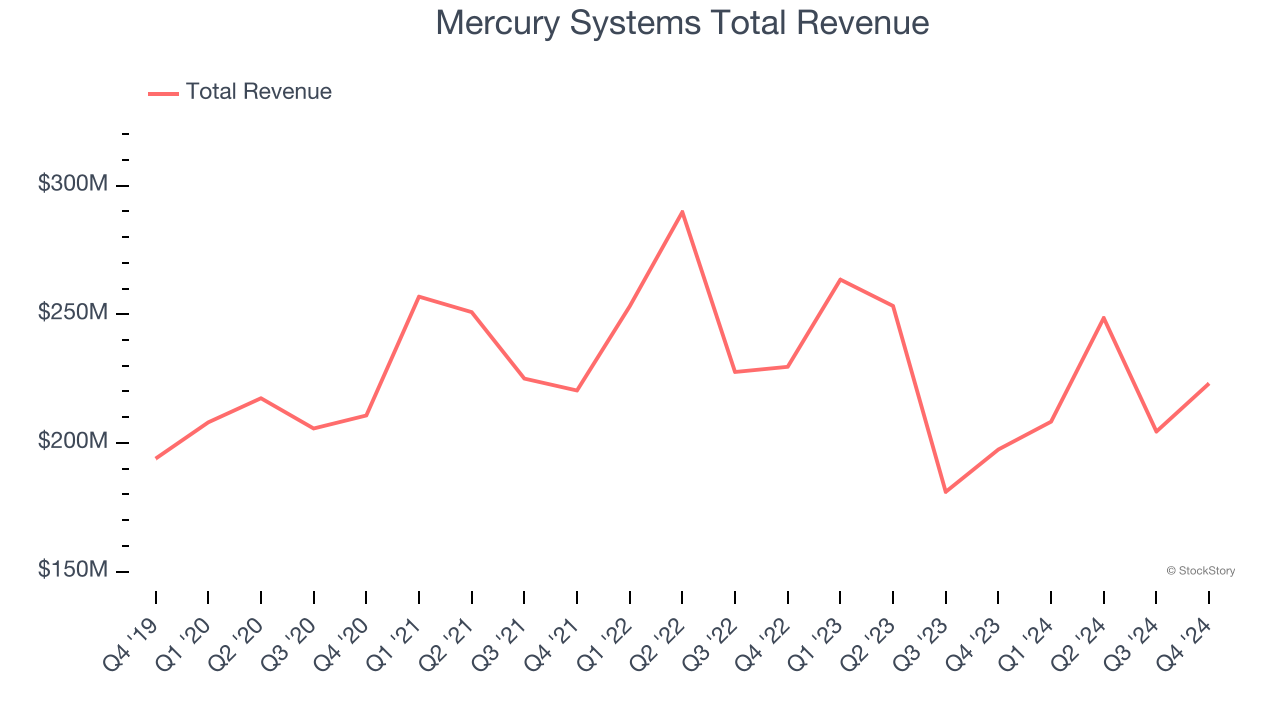

Best Q4: Mercury Systems (NASDAQ: MRCY)

Founded in 1981, Mercury Systems (NASDAQ: MRCY) specializes in providing processing subsystems and components for primarily defense applications.

Mercury Systems reported revenues of $223.1 million, up 13% year on year, outperforming analysts’ expectations by 23.9%. The business had an incredible quarter with an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ EPS estimates.

Mercury Systems pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 9.4% since reporting. It currently trades at $46.05.

Is now the time to buy Mercury Systems? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Boeing (NYSE: BA)

One of the companies that forms a duopoly in the commercial aircraft market, Boeing (NYSE: BA) develops, manufactures, and services commercial airplanes, defense products, and space systems.

Boeing reported revenues of $15.24 billion, down 30.8% year on year, falling short of analysts’ expectations by 6.4%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

Boeing delivered the slowest revenue growth in the group. Interestingly, the stock is up 3.1% since the results and currently trades at $180.59.

Read our full analysis of Boeing’s results here.

Woodward (NASDAQ: WWD)

Initially designing controls for water wheels in the early 1900s, Woodward (NASDAQ: WWD) designs, services, and manufactures energy control products and optimization solutions.

Woodward reported revenues of $772.7 million, down 1.8% year on year. This number met analysts’ expectations. Zooming out, it was a slower quarter as it produced a significant miss of analysts’ adjusted operating income estimates and a slight miss of analysts’ organic revenue estimates.

The stock is up 2.4% since reporting and currently trades at $192.49.

Read our full, actionable report on Woodward here, it’s free.

Ducommun (NYSE: DCO)

California’s oldest company, Ducommun (NYSE: DCO) is a provider of engineering and manufacturing services for high-performance products primarily within the aerospace and defense industries.

Ducommun reported revenues of $197.3 million, up 2.6% year on year. This print topped analysts’ expectations by 1.1%. More broadly, it was a softer quarter as it recorded a significant miss of analysts’ adjusted operating income estimates.

The stock is down 1.4% since reporting and currently trades at $60.49.

Read our full, actionable report on Ducommun here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.