Over the past six months, Fastenal has been a great trade. While the S&P 500 was flat, the stock price has climbed by 9.1% to $77.12 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Fastenal, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We’re glad investors have benefited from the price increase, but we're cautious about Fastenal. Here are three reasons why there are better opportunities than FAST and a stock we'd rather own.

Why Is Fastenal Not Exciting?

Founded in 1967, Fastenal (NASDAQ: FAST) provides industrial and construction supplies, including fasteners, tools, safety products, and many other product categories to businesses globally.

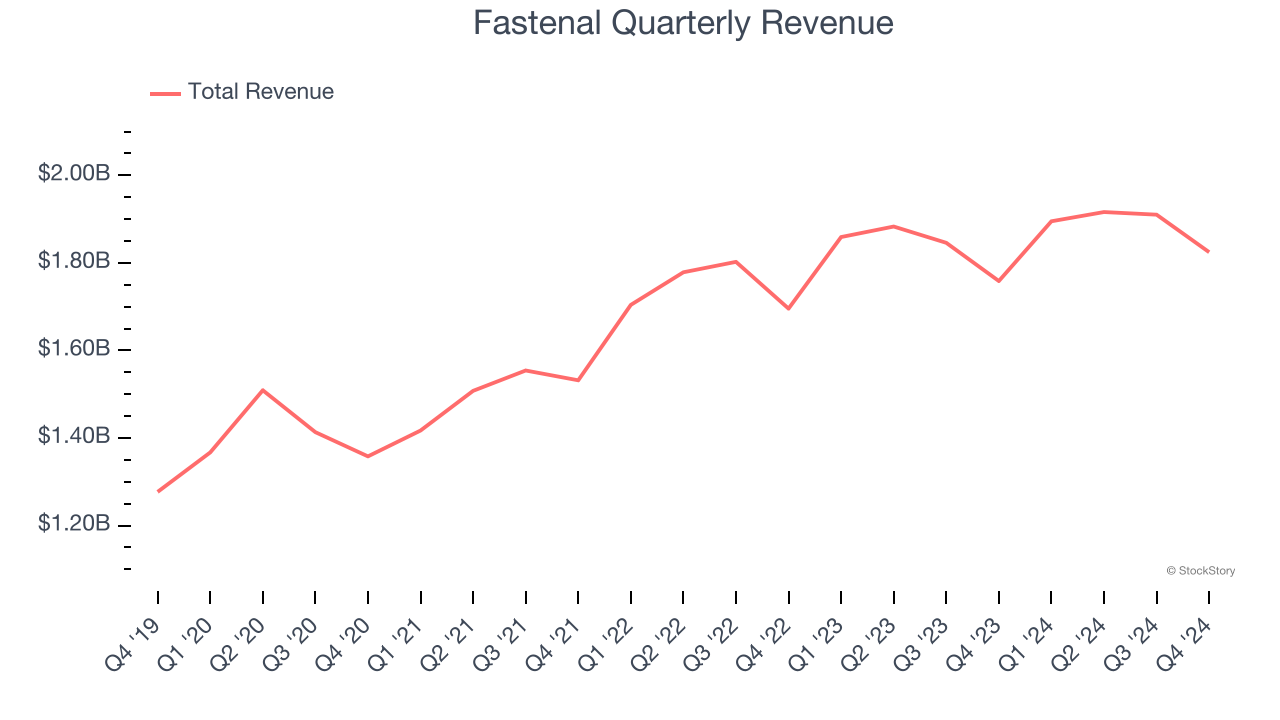

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Fastenal’s sales grew at a mediocre 7.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector.

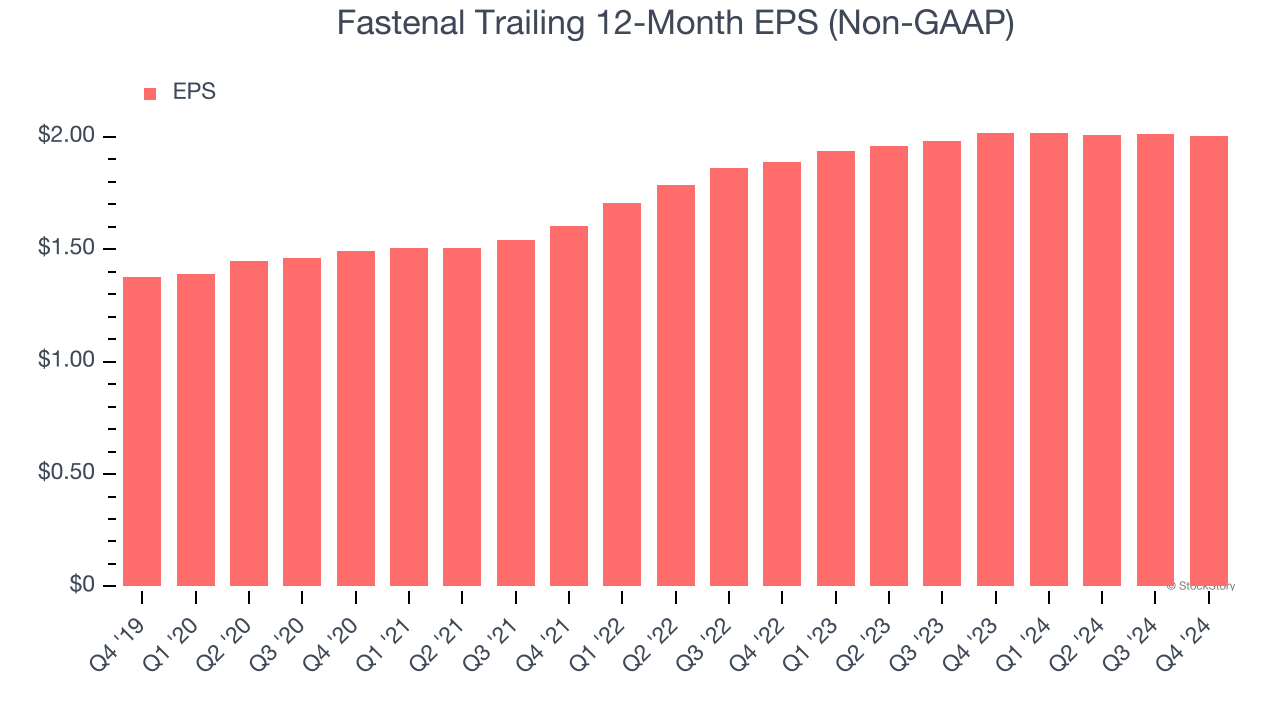

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Fastenal’s unimpressive 7.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

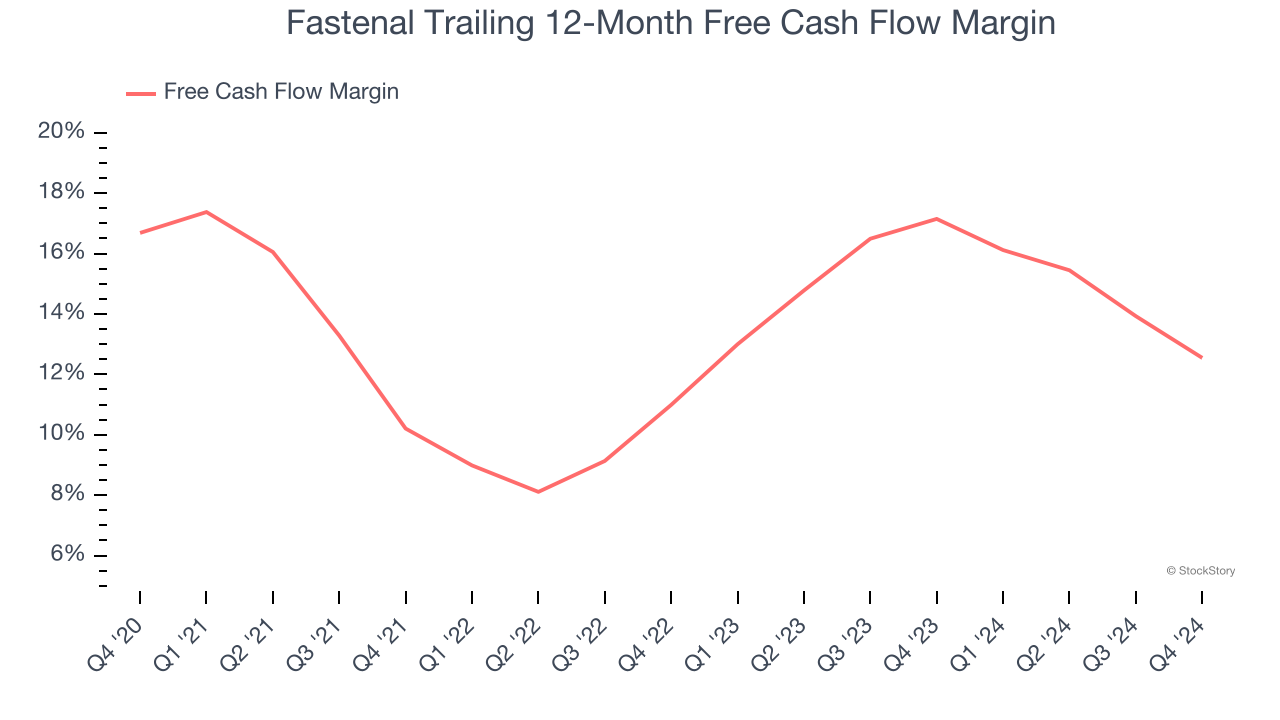

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Fastenal’s margin dropped by 4.1 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Fastenal’s free cash flow margin for the trailing 12 months was 12.5%.

Final Judgment

Fastenal isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 35.4× forward price-to-earnings (or $77.12 per share). This multiple tells us a lot of good news is priced in - we think there are better investment opportunities out there. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Fastenal

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.