As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the surgical equipment & consumables - specialty industry, including Intuitive Surgical (NASDAQ: ISRG) and its peers.

The surgical equipment and consumables industry provides tools, devices, and disposable products essential for surgeries and medical procedures. These companies therefore benefit from relatively consistent demand, driven by the ongoing need for medical interventions, recurring revenue from consumables, and long-term contracts with hospitals and healthcare providers. However, the high costs of R&D and regulatory compliance, coupled with intense competition and pricing pressures from cost-conscious customers, can constrain profitability. Over the next few years, tailwinds include aging populations, which tend to need surgical interventions at higher rates. The increasing integration of AI and robotics into surgical procedures could also create opportunities for differentiation and innovation. However, the industry faces headwinds including potential supply chain vulnerabilities, evolving regulatory requirements, and more widespread efforts to make healthcare less costly.

The 4 surgical equipment & consumables - specialty stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.7% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 12.3% since the latest earnings results.

Best Q4: Intuitive Surgical (NASDAQ: ISRG)

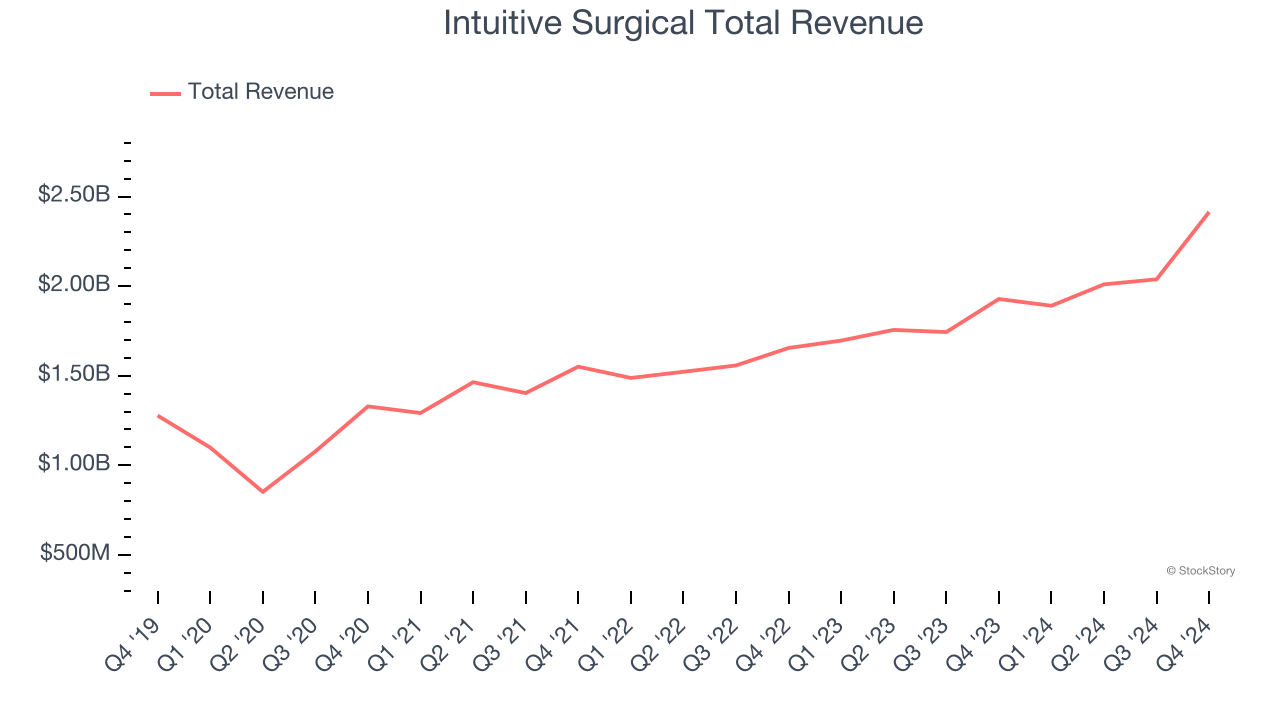

Pioneering minimally invasive surgery since its first da Vinci system was FDA-cleared in 2000, Intuitive Surgical (NASDAQ: ISRG) develops and manufactures robotic-assisted surgical systems that enable minimally invasive procedures across various medical specialties.

Intuitive Surgical reported revenues of $2.41 billion, up 25.2% year on year. This print exceeded analysts’ expectations by 6.5%. Overall, it was an incredible quarter for the company with an impressive beat of analysts’ sales volume and EPS estimates.

Intuitive Surgical achieved the biggest analyst estimates beat and fastest revenue growth of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 17.9% since reporting and currently trades at $499.06.

Is now the time to buy Intuitive Surgical? Access our full analysis of the earnings results here, it’s free.

LeMaitre (NASDAQ: LMAT)

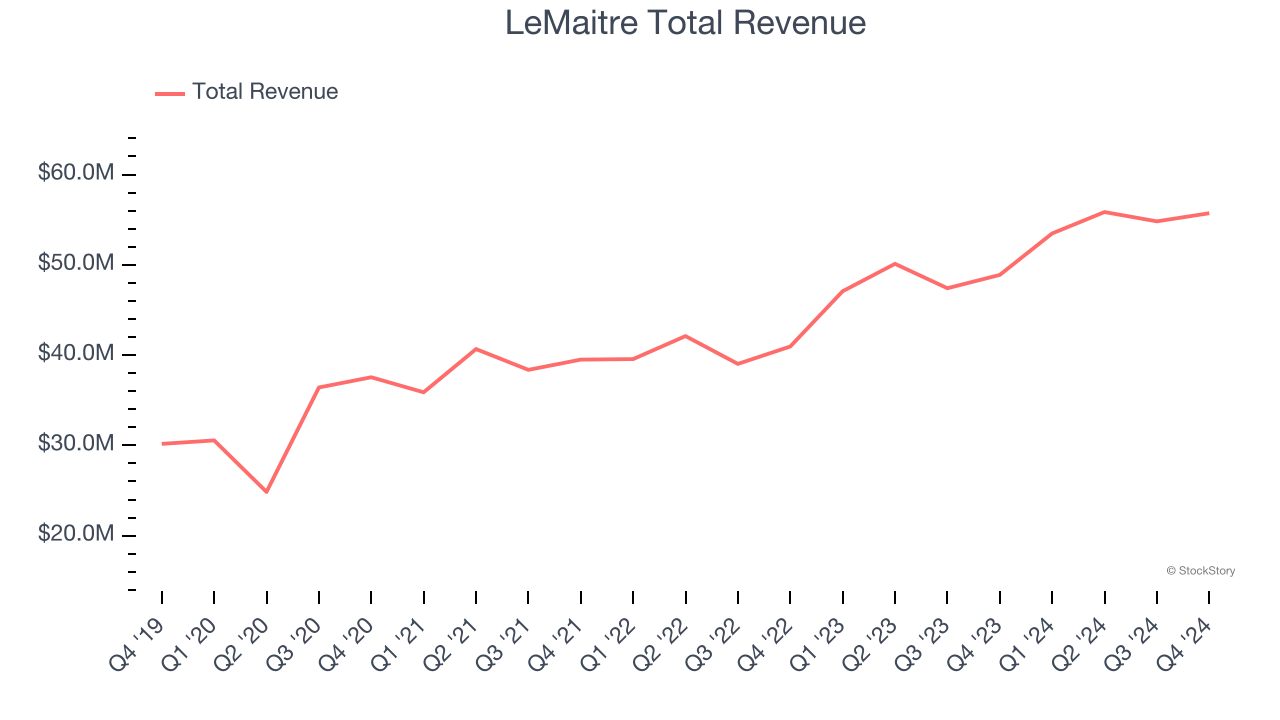

Founded in 1983 and named after a pioneering vascular surgeon, LeMaitre Vascular (NASDAQGM:LMAT) develops and manufactures specialized medical devices used by vascular surgeons to treat peripheral vascular disease and other circulatory conditions.

LeMaitre reported revenues of $55.72 million, up 14% year on year, falling short of analysts’ expectations by 0.7%. The business performed better than its peers, but it was unfortunately a mixed quarter with a solid beat of analysts’ full-year EPS guidance estimates.

LeMaitre scored the highest full-year guidance raise among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 16.5% since reporting. It currently trades at $83.49.

Is now the time to buy LeMaitre? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Teleflex (NYSE: TFX)

With a portfolio spanning from vascular access catheters to minimally invasive surgical tools, Teleflex (NYSE: TFX) designs, manufactures, and supplies single-use medical devices used in critical care and surgical procedures across hospitals worldwide.

Teleflex reported revenues of $795.4 million, up 2.8% year on year, falling short of analysts’ expectations by 2.3%. It was a softer quarter as it posted a miss of analysts’ constant currency revenue estimates.

Teleflex delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 19.9% since the results and currently trades at $142.23.

Read our full analysis of Teleflex’s results here.

Integra LifeSciences (NASDAQ: IART)

Founded in 1989 as a pioneer in regenerative medicine technology, Integra LifeSciences (NASDAQ: IART) develops and manufactures medical technologies for neurosurgery, wound care, and surgical reconstruction, including regenerative tissue products and surgical instruments.

Integra LifeSciences reported revenues of $442.6 million, up 11.5% year on year. This print came in 0.7% below analysts' expectations. It was a slower quarter as it also logged a miss of analysts’ full-year EPS guidance estimates.

Integra LifeSciences had the weakest full-year guidance update among its peers. The stock is up 4.3% since reporting and currently trades at $22.99.

Read our full, actionable report on Integra LifeSciences here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.