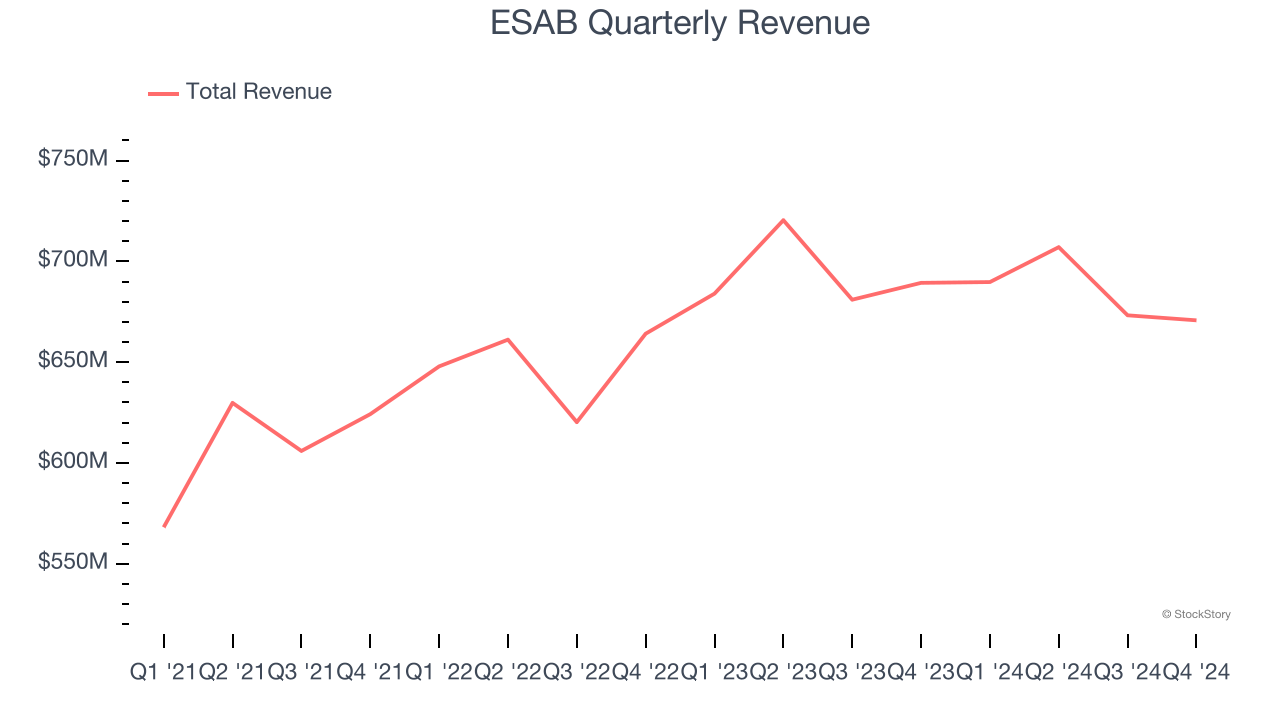

Welding and cutting equipment manufacturer ESAB (NYSE: ESAB) fell short of the market’s revenue expectations in Q4 CY2024, with sales falling 2.7% year on year to $670.8 million. Its non-GAAP profit of $1.28 per share was 9.9% above analysts’ consensus estimates.

Is now the time to buy ESAB? Find out by accessing our full research report, it’s free.

ESAB (ESAB) Q4 CY2024 Highlights:

- Revenue: $670.8 million vs analyst estimates of $676.2 million (2.7% year-on-year decline, 0.8% miss)

- Adjusted EPS: $1.28 vs analyst estimates of $1.16 (9.9% beat)

- Adjusted EBITDA: $128.6 million vs analyst estimates of $125.9 million (19.2% margin, 2.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $5.18 at the midpoint, missing analyst estimates by 3.9%

- EBITDA guidance for the upcoming financial year 2025 is $522.5 million at the midpoint, below analyst estimates of $546.4 million

- Operating Margin: 16.6%, up from 15% in the same quarter last year

- Free Cash Flow Margin: 0%, down from 15% in the same quarter last year

- Organic Revenue was flat year on year (4.2% in the same quarter last year)

- Market Capitalization: $7.56 billion

“Our teams delivered another strong quarter, closing another year of exceptional performance. ESAB continues to innovate, introducing products and solutions that fueled growth in welding equipment this quarter. Our relentless focus on efficiency is evident in our record-breaking margin performance," said Shyam P. Kambeyanda, President and CEO of ESAB.

Company Overview

Having played a significant role in the construction of the iconic Sydney Opera House, ESAB (NYSE: ESAB) manufactures and sells welding and cutting equipment for numerous industries.

Professional Tools and Equipment

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

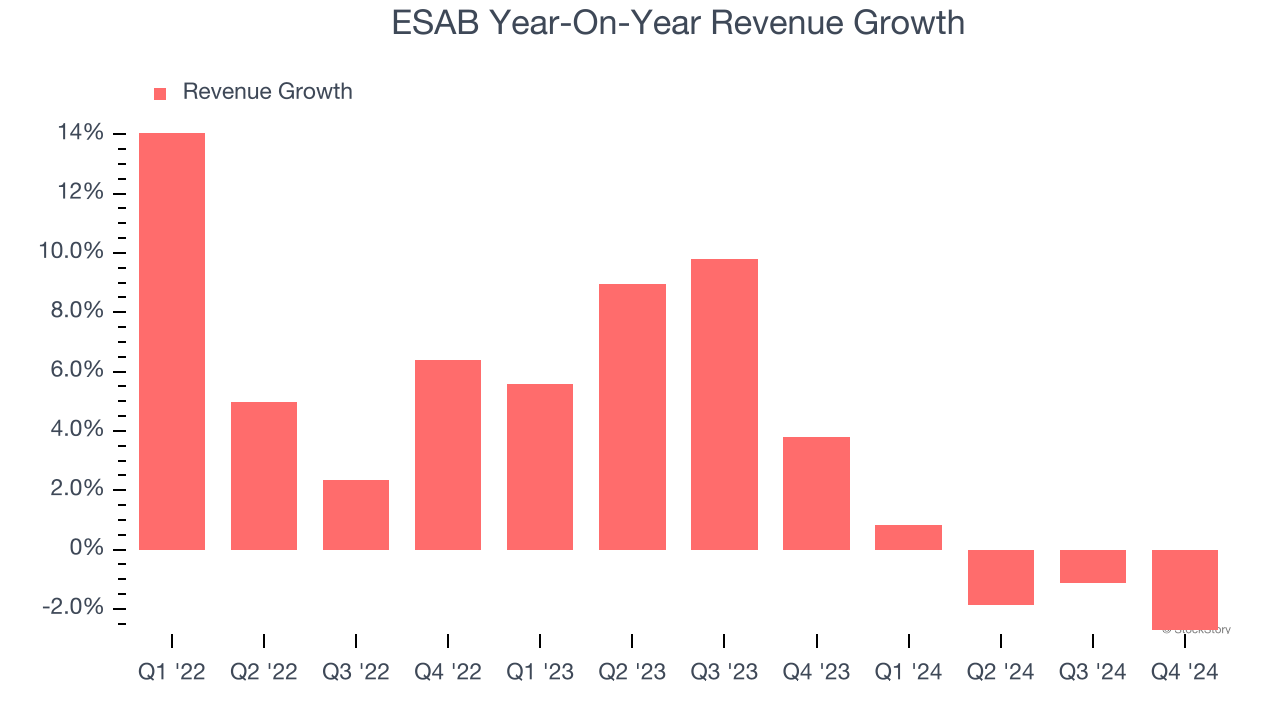

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, ESAB’s 4.1% annualized revenue growth over the last three years was sluggish. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. ESAB’s recent history shows its demand slowed as its annualized revenue growth of 2.8% over the last two years is below its three-year trend.

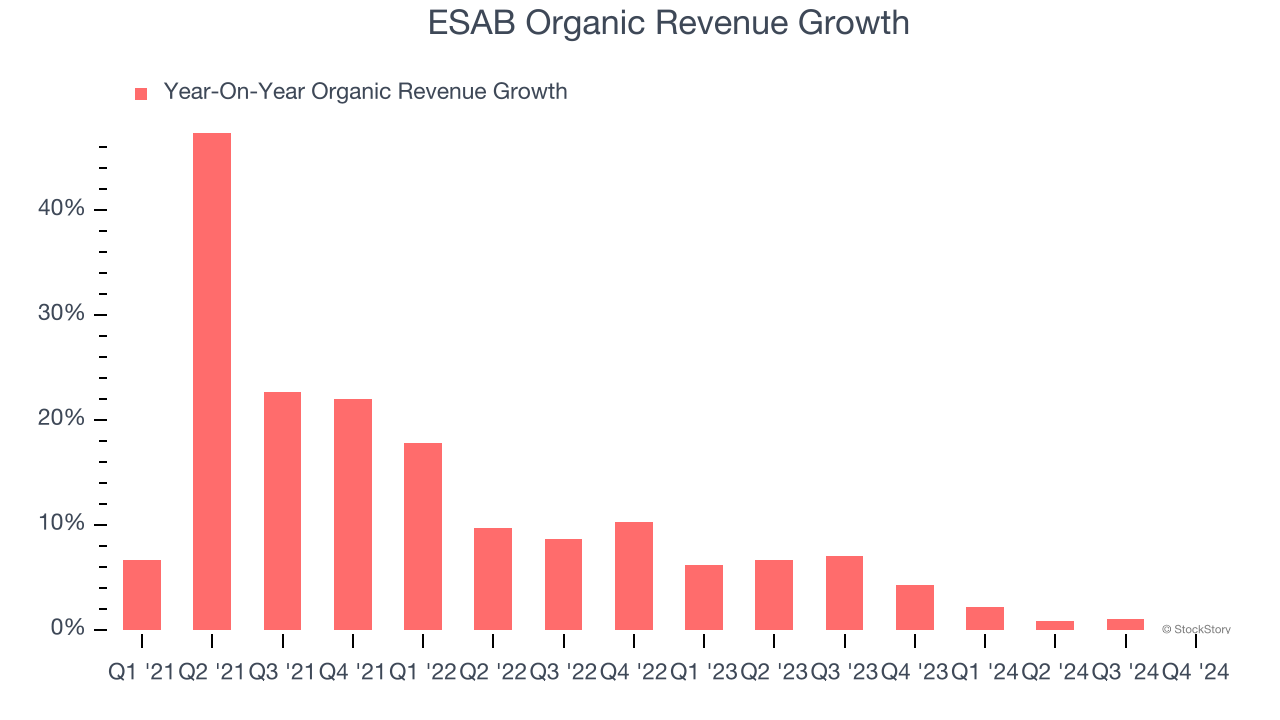

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, ESAB’s organic revenue averaged 3.5% year-on-year growth. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, ESAB missed Wall Street’s estimates and reported a rather uninspiring 2.7% year-on-year revenue decline, generating $670.8 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

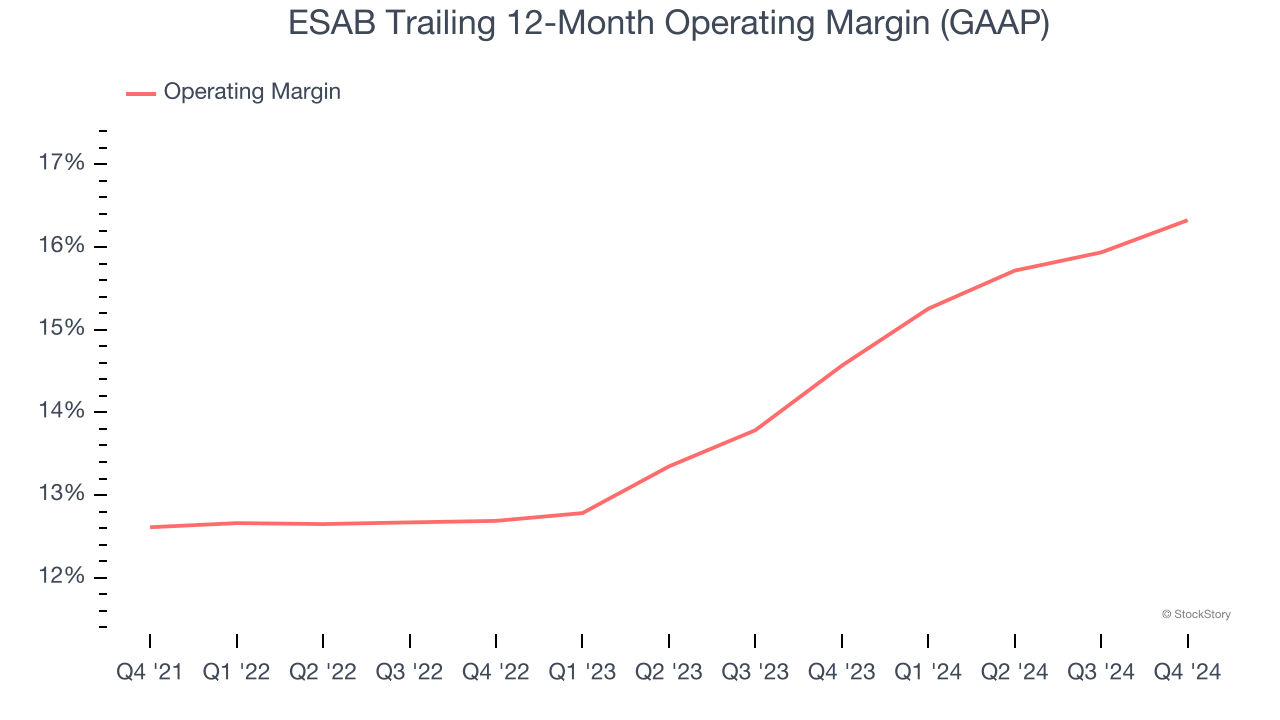

ESAB has been an efficient company over the last four years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.1%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, ESAB’s operating margin rose by 3.7 percentage points over the last four years, showing its efficiency has improved.

In Q4, ESAB generated an operating profit margin of 16.6%, up 1.6 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

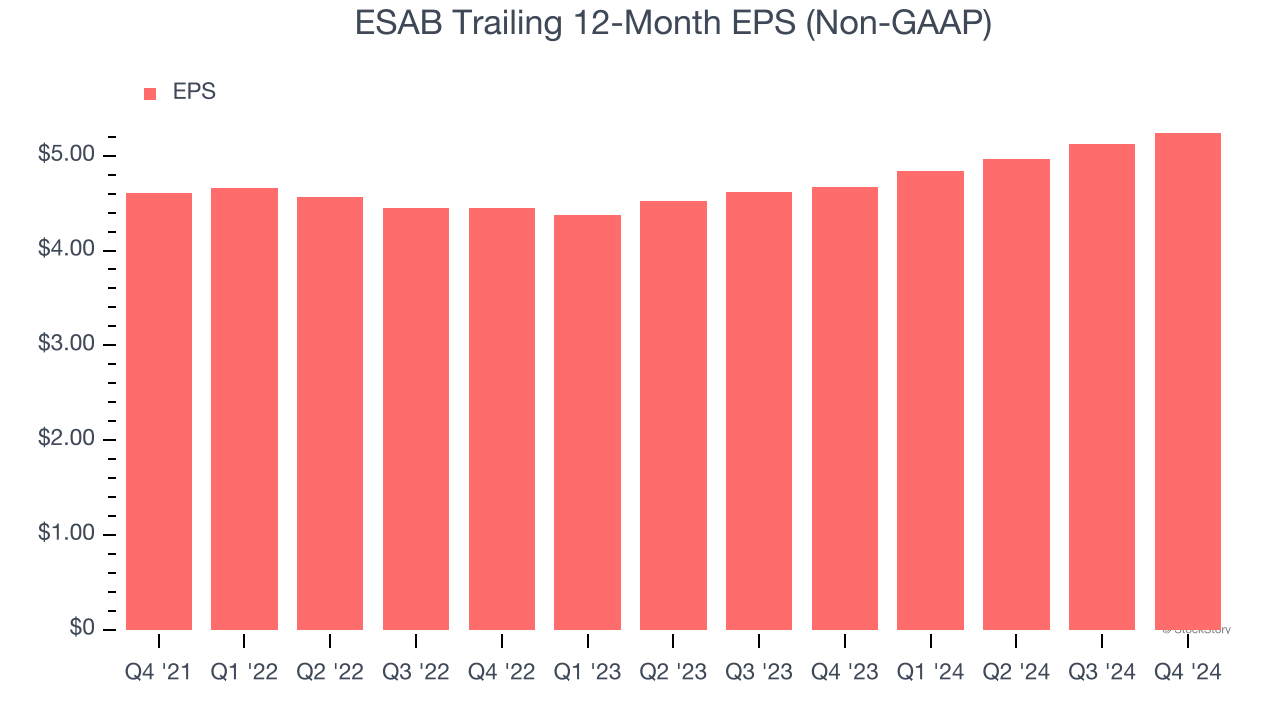

Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

ESAB’s EPS grew at a decent 8.5% compounded annual growth rate over the last two years, higher than its 2.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into ESAB’s earnings to better understand the drivers of its performance. ESAB’s operating margin has expanded by 4.8 percentage points over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, ESAB reported EPS at $1.28, up from $1.16 in the same quarter last year. This print beat analysts’ estimates by 9.9%. Over the next 12 months, Wall Street expects ESAB’s full-year EPS of $5.24 to grow 3.2%.

Key Takeaways from ESAB’s Q4 Results

It was encouraging to see ESAB beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed significantly and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.5% to $122 immediately after reporting.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.