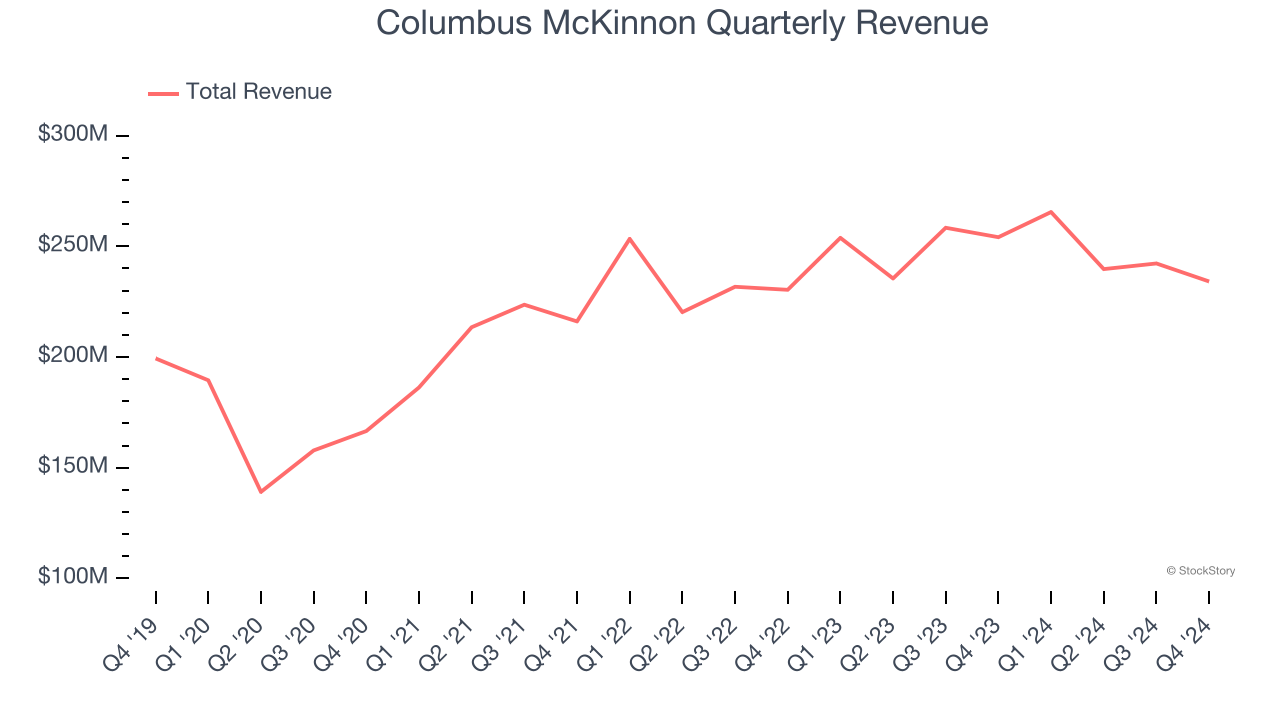

Material handling equipment manufacturer Columbus McKinnon (NASDAQ: CMCO) fell short of the market’s revenue expectations in Q4 CY2024, with sales falling 7.9% year on year to $234.1 million. Its non-GAAP profit of $0.56 per share was 23.3% below analysts’ consensus estimates.

Is now the time to buy Columbus McKinnon? Find out by accessing our full research report, it’s free.

Columbus McKinnon (CMCO) Q4 CY2024 Highlights:

- Revenue: $234.1 million vs analyst estimates of $253.9 million (7.9% year-on-year decline, 7.8% miss)

- Adjusted EPS: $0.56 vs analyst expectations of $0.73 (23.3% miss)

- Adjusted EBITDA: $37.78 million vs analyst estimates of $40.09 million (16.1% margin, 5.8% miss)

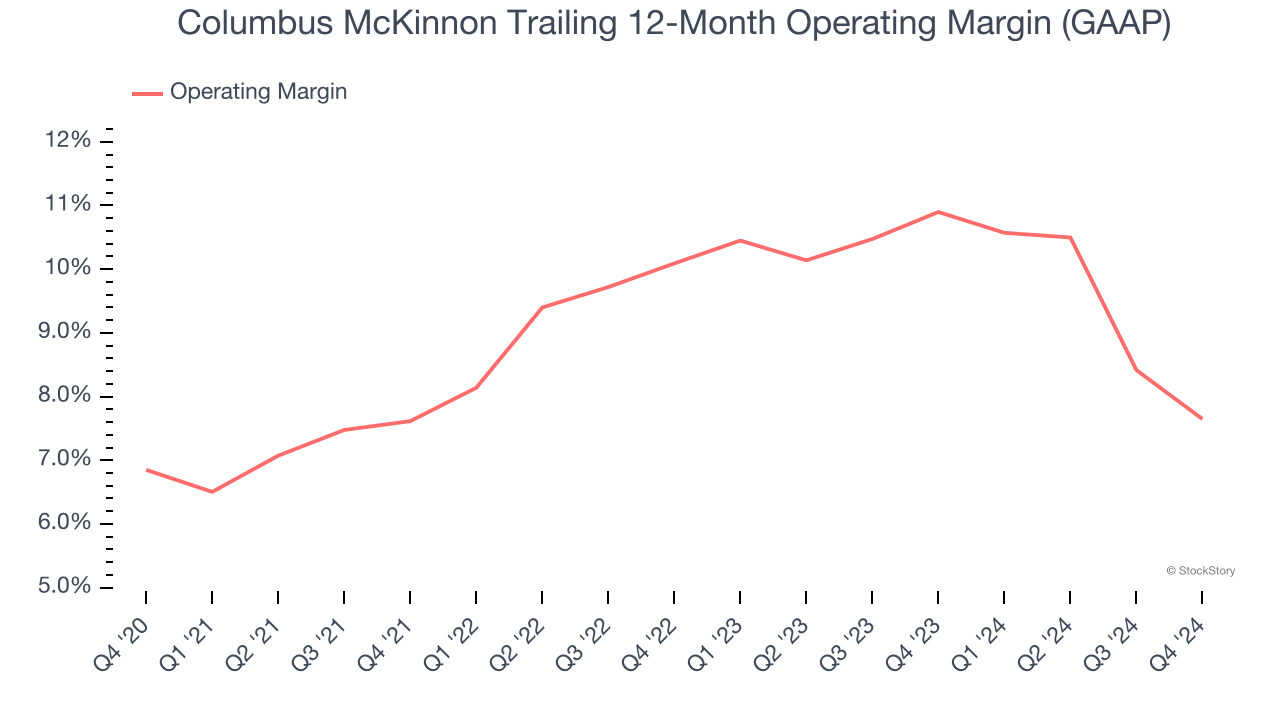

- Operating Margin: 7.6%, down from 10.6% in the same quarter last year

- Free Cash Flow Margin: 2.6%, down from 9.1% in the same quarter last year

- Backlog: $296.5 million at quarter end

- Market Capitalization: $982.6 million

"The second half of our third quarter saw a slowing of industry demand. This was driven by delayed customer decision-making related to U.S. policy uncertainty, including tariffs as well as continued weakening in the European economies," said David J. Wilson, President and Chief Executive Officer.

Company Overview

With 19 different brands across the globe, Columbus McKinnon (NASDAQ: CMCO) offers material handling equipment for the construction, manufacturing, and transportation industries.

General Industrial Machinery

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

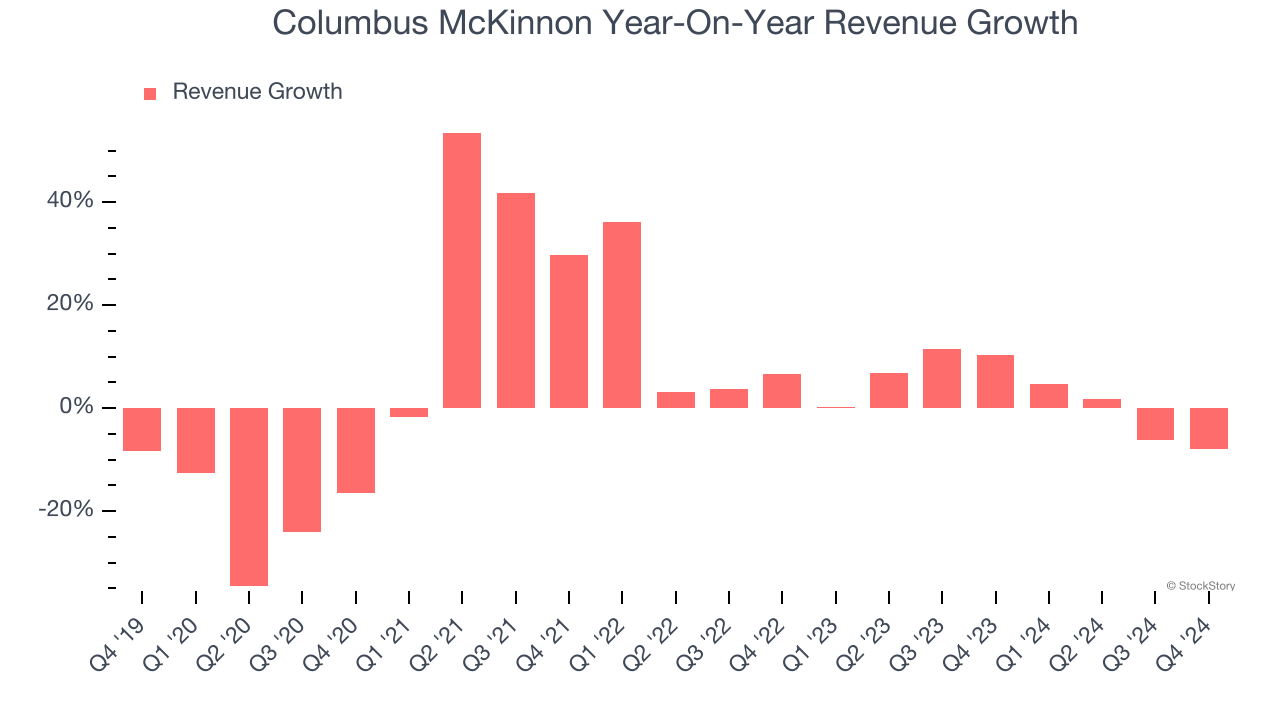

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Columbus McKinnon grew its sales at a sluggish 3.3% compounded annual growth rate. This was below our standard for the industrials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Columbus McKinnon’s annualized revenue growth of 2.4% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Columbus McKinnon missed Wall Street’s estimates and reported a rather uninspiring 7.9% year-on-year revenue decline, generating $234.1 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Columbus McKinnon has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.8%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Columbus McKinnon’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years . Shareholders will want to see Columbus McKinnon grow its margin in the future.

In Q4, Columbus McKinnon generated an operating profit margin of 7.6%, down 3 percentage points year on year. Since Columbus McKinnon’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

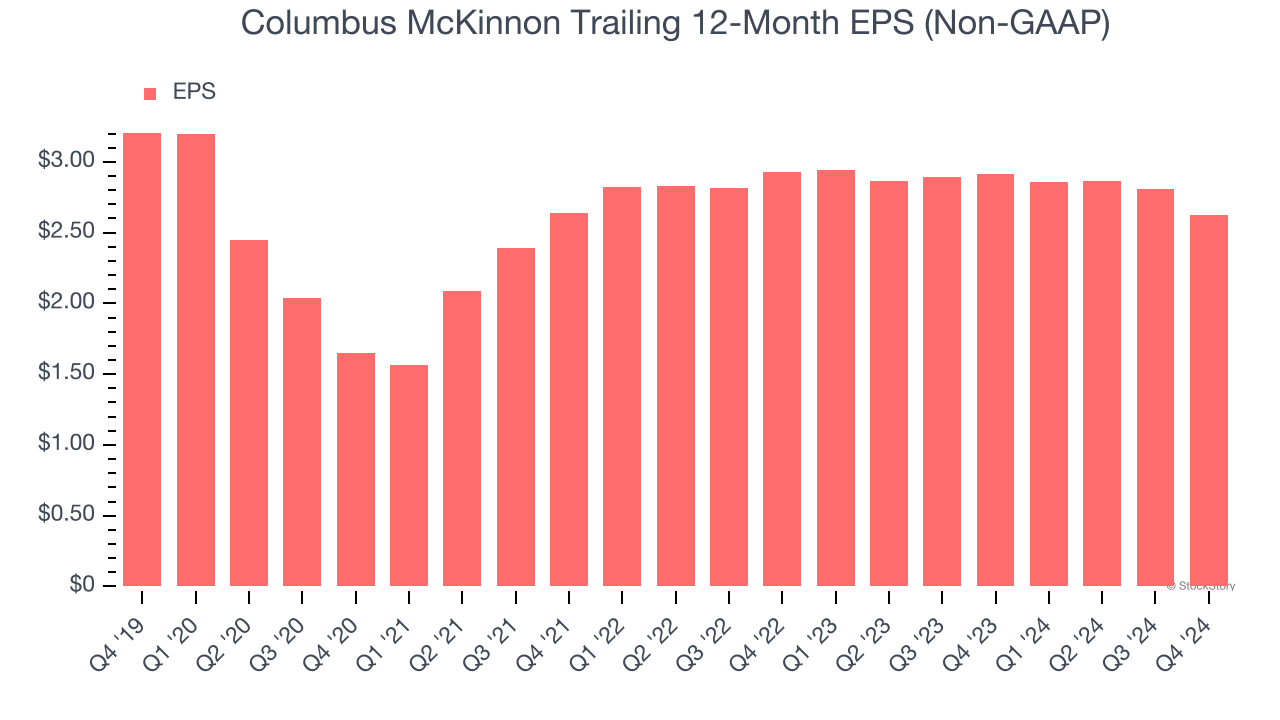

Sadly for Columbus McKinnon, its EPS declined by 3.9% annually over the last five years while its revenue grew by 3.3%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

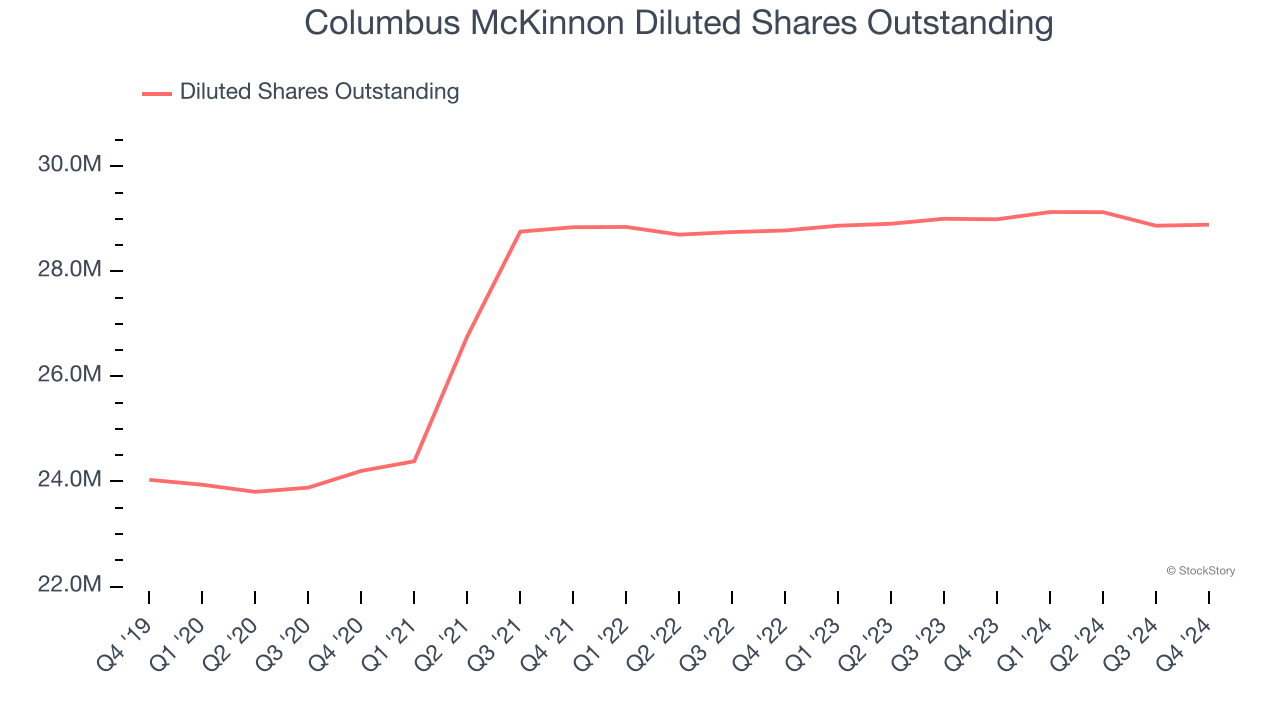

Diving into the nuances of Columbus McKinnon’s earnings can give us a better understanding of its performance. A five-year view shows Columbus McKinnon has diluted its shareholders, growing its share count by 20.2%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Columbus McKinnon, its two-year annual EPS declines of 5.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Columbus McKinnon reported EPS at $0.56, down from $0.74 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Columbus McKinnon’s full-year EPS of $2.63 to grow 23%.

Key Takeaways from Columbus McKinnon’s Q4 Results

We struggled to find many positives in these results. Its revenue missed significantly and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.1% to $34.36 immediately following the results.

Columbus McKinnon may have had a tough quarter, but does that actually create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.