Strongly Encourages Stockholders to Vote FOR Joe Kiani and Christopher Chavez on the GOLD Proxy Card

Warns Stockholders of Politan’s Value-Destructive Agenda Should It Gain Control

Highlights Masimo’s Track Record of Innovation, Longstanding Premium Valuation, Strong Long-Term Plan and Superior Director Nominees

Visit ProtectMasimosFuture.com for More Information

Members of the Masimo Corporation (“Masimo” or the “Company”) (NASDAQ: MASI) Board of Directors today issued a letter to stockholders in connection with its definitive proxy materials filed on June 17, 2024, and the Company’s Annual Meeting of Stockholders to be held on July 25, 2024. The letter highlights what in our view are the significant risks to the value of Masimo if control of the Board is ceded to Politan Capital Management (“Politan”), which we believe wants to eliminate some of the key people and practices that have fueled Masimo’s long-term innovation and growth and supported its premium valuation multiple. The letter also details the Company’s excellent positioning to continue to drive above-market organic growth and meaningful margin expansion, while highlighting the expertise and experience of Masimo’s highly qualified director nominees. To protect stockholders’ investment and the Company’s future, the Board strongly encourages stockholders to vote FOR Masimo’s exceptional director nominees, Joe Kiani and Christopher Chavez.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20240617740544/en/

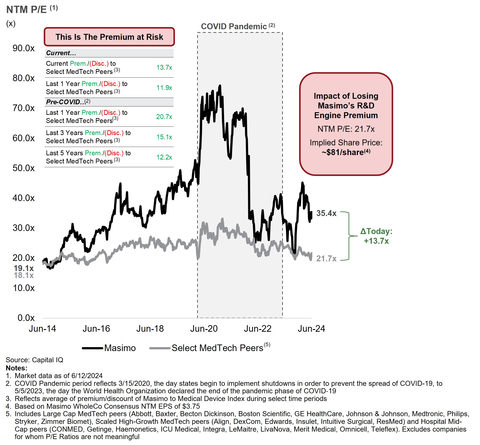

Fig. 1 – Masimo Has Historically Traded at a Premium to Select MedTech Peers (Graphic: Business Wire)

Find our definitive proxy materials and more information on why your vote is critical to the future of Masimo at www.ProtectMasimosFuture.com. The full text of the Board’s letter to our stockholders can be found here:

Dear Fellow Masimo Stockholders:

At the upcoming Annual Meeting of Stockholders, you face a choice: electing your Board’s nominees – Joe Kiani, the founder, Chairman and CEO of Masimo, and Christopher Chavez, a highly experienced and independent former CEO and director of public medical device companies – or adding two more nominees hand-picked and paid by Politan, thereby ceding control of Masimo to Politan.

This election is critical to the future of Masimo and the value of your investment in our stock. As independent directors who have served on Masimo’s Board alongside Politan directors Quentin Koffey and Michelle Brennan, it’s clear to us that they have no understanding of Masimo’s business. Innovation and revenue growth have supported Masimo’s longstanding valuation premium to medical technology peers, but we believe Politan wants to eliminate some of the key people and practices that drive Masimo’s innovation and growth. The risk of their agenda is immense.

Masimo has earned its valuation through innovation that has driven consistent organic growth, consistently taking share in existing markets with clinically superior products and creating new markets with new technologies and applications. Mr. Kiani leads this process with a team that drives and is driven by him. We are concerned that replacing this approach and team with Politan’s inexperience and what we believe is a misguided agenda will destroy Masimo’s innovation engine, slow organic growth, and dramatically depress Masimo’s valuation multiple.

A year ago, Politan rebuffed Masimo’s assertion that Politan was seeking control of the Company as “absurd.” Now, Politan is doing exactly that—refusing to settle its second consecutive proxy contest for anything less than a majority of Politan-nominated directors on the Company’s Board.

Your vote on the GOLD card FOR Masimo director nominees Joe Kiani and Christopher Chavez will help ensure that Masimo continues delivering on its business plan to create value for stockholders and improve the lives of patients and customers.

With your support at the upcoming Annual Meeting, we are confident that we can complete the separation of Masimo’s consumer business, continue to advance our strong innovation pipeline to support our valuation premium, consistently meet or exceed revenue and earnings expectations, and continue to seat highly qualified and independent directors to expand the Board.

Since last year’s Annual Meeting, Masimo has weathered the post-Covid market environment and returned to growth in its healthcare business, gained significant market share, and successfully enforced our intellectual property against Apple at the U.S. International Trade Commission. Our Board and management team also undertook a thorough engagement program with our stockholders – we listened and we acted. As a result, we have undertaken a process to separate our consumer business in a manner that we believe will maximize value for our stockholders.

We accomplished all of this despite what we view as obstructive behavior by the Politan directors. During the past year, we believe the Politan directors:

- Imposed undue burdens on management and the rest of the Board, while making no constructive business proposals or suggestions;

- Obstructed the stockholder-directed expansion of the Board by creating an adversarial Board environment that helped drive away two qualified Board members and threatened litigation when the Board sought to replace them; and

- Obstructed the stockholder-requested process to separate the Consumer business.

In our opinion, this obstruction has not served stockholders’ interests; it has only served Politan’s bid for control of Masimo.

The choice in front of you is stark. Here’s why you should vote “FOR” Masimo’s nominees on the GOLD proxy card:

- Preserve Masimo’s innovation engine and valuation premium.

- Support Masimo’s push to achieve a 30% operating margin while maintaining its historical organic growth.

- Stop Politan from enacting its destructive agenda and impeding progress on value creation at Masimo, including successfully completing the separation of the Consumer business.

- Elect the most qualified nominees to Masimo’s Board, ensuring strong independent oversight and the resumption of a rigorous process to expand the Board.

We remain committed to listening to and delivering value for our stockholders. We believe handing control of the Company to Politan would risk the destruction of value in your investment in Masimo.

PRESERVE MASIMO’S INNOVATION PREMIUM

Historically, Masimo’s stockholders have benefited from the significant valuation premium ascribed to the Company for its ability to drive above-market organic growth through consistently innovating profitable, market-leading products (Fig. 1).

Since Masimo’s founding and to this day, Mr. Kiani’s vision, leadership and hands-on R&D direction have been critical to sustaining innovation, growth and shareholder value beyond its peers. In the medical technology industry broadly, stock valuation is strongly correlated to forward revenue growth expectations (Fig. 2). Masimo has achieved revenue growth by taking market share from competitors through innovating clinically superior products and by creating new markets with its new technologies. Notably, Masimo trades at a nearly 63% premium to select MedTech peers on a NTM P/E multiple basis, highlighting the risk to the Company’s valuation if the Company loses Mr. Kiani’s leadership and is unable to sustain the consistent innovation that has driven its growth for decades.

Unlike most other CEOs in the medical device industry, Mr. Kiani continues to play a direct role in Masimo’s R&D efforts. Mr. Kiani is named as an inventor on over 900 of Masimo’s patent filings, reflecting his unique contributions to Masimo’s core technologies and capabilities. This is not just a historical achievement – many of Masimo’s recently introduced products, such as Oxygen Reserve Index™ (ORi™), Stork™, Opioid Halo™, W1 and Radius VSM™, originated with Mr. Kiani.

Despite challenges from last year’s proxy contest, rapidly shifting market conditions and Politan’s disruptive presence in the boardroom, the Company achieved significant innovation milestones. These include:

-

Securing FDA clearances of:

- ORi™;

- Masimo SET®-based Opioid Halo™ wearable, the first-ever FDA-authorized opioid overdose prevention system;

- Radius VSM™, an incredibly versatile, wearable vital signs monitor;

- Masimo Stork™, a state-of-the-art baby monitor backed by clinically proven Masimo SET® pulse oximetry; and

- Masimo W1 medical watch for use in hospital-to-home and telehealth programs.

We expect these and future innovations will continue to be important drivers of growth. One of Masimo’s fastest-growing products, ORi™ accounted for more than 20% of worldwide sales of rainbow™ products in 2023 despite only launching in the U.S. late in the fourth quarter. ORi™ is the first noninvasive technology that provides insight into a patient’s oxygen status in the moderate hyperoxic range, and our research has clearly established its clinical benefits for use during surgery, in the ICU and in other places where oxygen is prescribed. We expect ORi™ will drive significant growth in rainbow™ revenues and have a positive effect on our broader hospital relationships and contracting efforts.

Under Mr. Kiani’s leadership, Masimo has continued to build a pipeline of promising products to sustain the Company’s long-term growth trajectory. Innovative hospital technologies outside of Masimo’s core SET® pulse oximetry products achieved double-digit growth in 2022 and 2023. Additionally, Masimo’s pulse oximetry business has benefitted greatly from the fact that customers can upgrade to rainbow™ or tetherless pulse oximetry, which are two highly differentiated technologies that are unique to Masimo.

SUPPORT MASIMO’S PUSH TO ACHIEVE A 30% OPERATING MARGIN WHILE MAINTAINING ITS HISTORICAL ORGANIC GROWTH

Under our oversight, Mr. Kiani and the current management team have returned the professional healthcare business to its customary consistent meet or beat performance. Even as sensor sales temporarily declined during 2023, Mr. Kiani’s team successfully focused on expanding its footprint with existing customers and winning new customers to build a strong foundation for returning growth in healthcare to its historic trajectory. The value of incremental new contracts won in 2023 exceeded the previous record high set during the height of the Covid pandemic (Fig. 3), and worldwide unrecognized contract revenue reached levels that we believe support our effort to achieve high-single-digit organic revenue growth in 2024 (Fig. 4).

Masimo’s driver installed base has increased over 60% from 1.6 million drivers in 2017 to about 2.6 million as of the first quarter of 2024. At the same time, consumable revenue per driver has grown from pre-COVID levels, driven by continued strong utilization, increasing adoption of premium rainbow sensors and our ongoing development of new applications and use cases – all trends we anticipate continuing under our long-term plan (Fig. 5).

This strong foundation, along with significant contributions from faster-growing new products, underpins our growth expectations and ensures that we can generate substantial operating leverage to reach our long-term goal of 30% non-GAAP operating margins, as management shared in our Q1 2024 earnings presentation. Alongside the transition of high-volume sensor manufacturing to Malaysia and engineering initiatives to reduce product costs, we anticipate our steady innovation-led growth trajectory to drive leverage on our R&D, sales, and corporate and administrative expenses and account for a significant portion of that margin improvement.

Successful execution of these plans requires a focused, experienced Board and management team with a deep understanding of the business and the ability to balance innovation-driven growth and profitability. During their time on the Board, Mr. Koffey and Michelle Brennan have in our view distracted the Board and management team and made no strategic recommendations or suggested any ideas for improving Masimo’s revenue growth, operating margin and earnings. We believe cutting R&D investments and jettisoning Masimo’s time-tested approach to innovation would make it unlikely that Masimo achieves our targeted growth rates and generates the operating leverage needed to substantially expand margins. We believe handing control of the Board to Politan would threaten Masimo’s operational and financial stability and its ability to achieve its long-term goals.

STOP POLITAN FROM ENACTING WHAT WE BELIEVE IS A DESTRUCTIVE AGENDA AND OBSTRUCTING PROGRESS

While we have acted in accordance with the wishes of the majority stockholders of Masimo to separate the Consumer business, continue meeting or exceeding earnings expectations, expand the Board with independent directors, and try to avoid another proxy contest, we believe that Politan has obstructed progress and prioritized gaining control over serving stockholders’ interests. Notably, in our view:

- Mr. Koffey led the Special Committee to failure: After Mr. Koffey and Mr. Kiani discussed and agreed to potential terms for a separation of the Consumer Business, the Board formed a Special Committee of independent directors on February 13, 2024, chaired by Mr. Koffey, to progress the separation plans. In his capacity as chair, Mr. Koffey delivered a new term sheet that was radically different from the terms he had previously proposed and discussed with the full Board. In our view, the new term sheet would have created an unviable business without the cash reserves needed to operate on a solvent footing and without the rights necessary for the litigation with Apple. Two of the Special Committee members recommended dissolving the Special Committee because of its departure from what was discussed with the full Board and Mr. Koffey’s handling of it in his role as chairperson.

- Mr. Koffey has refused to settle despite stockholder support for a settlement: Following our initial settlement offer made on April 4, 2024, Mr. Koffey told Bob Chapek that his efforts to settle would be fruitless. Nonetheless, we tried and made two additional settlement proposals that would have given the Politan directors veto power. Politan’s only proposal would hand majority control of the Board to Politan and its unqualified Board members, which we believe would have been a dereliction of the Board’s fiduciary duties. Mr. Koffey never engaged with us to find a middle ground that would benefit stockholders.

- Politan’s directors took actions that tried to delay and block the expansion of the Board with highly qualified independent directors: Despite being offered – and accepting – the opportunity to review resumes, interview candidates, submit additional candidates and amend the search criteria, Mr. Koffey and Ms. Brennan requested that the Company start an entirely new director search process, after Heidrick & Struggles had already identified and evaluated approximately 50 candidates. They then voted against the appointments of highly qualified independent directors Rolf Classon and Mr. Chapek. Further, after Mr. Mikkelson and Mr. Classon resigned from the Board citing personal and health reasons, respectively, Politan threatened litigation if we replaced them despite the fact that the Board now has only five members.

- Mr. Koffey proposed Mr. Kiani swap classes with another director so Politan would not face Mr. Kiani at this Annual Meeting, contrary to Delaware law: On April 25, 2024, Mr. Koffey proposed that Mr. Kiani and Mr. Reynolds switch director classes ahead of the Annual Meeting so that Mr. Reynolds would stand for election instead of Mr. Kiani. Ms. Brennan also supported this proposal, which is not permitted under Delaware law, as it undermines the stockholder franchise and flies in the face of good governance. We think this, and his plan to reappoint Mr. Kiani as Chairman of the Board if he is not reelected to the Board, demonstrates that Mr. Koffey does not truly care about good governance. Mr. Koffey also told us he would put Mr. Kiani on administrative leave following the election if Mr. Kiani were to accept reappointment to the Board, which Mr. Kiani has made clear he would not do.

Most recently, the Politan directors have taken actions that, in our view, have obstructed the separation of the Consumer business. We continue to pursue both a spinoff transaction and a potential JV transaction and are focused on executing whichever option creates more value for stockholders. Mr. Koffey’s legal threats and false accusations have unjustifiably alarmed some stockholders and delayed and made the pathway to a successful and value-accretive separation more challenging and costly.

More worrisome is the prospect of Politan enacting a potentially destructive agenda for Masimo. Politan’s eagerness to discard Masimo’s successful approach to running the Company as well as the leadership team that has created value for 35 years highlights what we view as Mr. Koffey’s reckless disregard for risk to stockholders. His failed leadership of the Special Committee foreshadows the future of the Company under his control. None of the Politan directors or nominees have public medical technology company director experience that would suggest they should be trusted with choosing a CEO for Masimo. By ousting Mr. Kiani, Politan would also destroy our succession plans, as we think other key employees may also leave.

We believe Politan’s approach to replacing a successful founder CEO, who many other companies would like to recruit, is dangerous to stockholders and other important stakeholders, including the hospitals and patients that rely on Masimo’s products and innovation.

ELECT THE MOST QUALIFIED NOMINEES TO MASIMO’S BOARD, ENSURING STRONG INDEPENDENT OVERSIGHT AND THE RESUMPTION OF A RIGOROUS PROCESS TO EXPAND THE BOARD

Mr. Kiani and Mr. Chavez bring Masimo’s Board significant insight and experience with 70-plus years of combined medical device industry leadership at the highest levels. By contrast, Politan’s nominees, William Jellison and Darlene Solomon, lack CEO experience, and neither have previously been directors at a medical device company – bringing the total medical company director experience of the Politan directors and nominees to zero.

As Masimo’s Founder and CEO since its inception 35 years ago, Mr. Kiani has a unique understanding of Masimo’s business and the innovation required to drive stockholder value. He has led Masimo through numerous strategic, engineering, market access, regulatory and legal challenges and built irreplaceable relationships with customers, partners, physicians, industry leaders and regulators. As previously discussed, Mr. Kiani remains deeply involved in Masimo’s R&D efforts. Mr. Kiani’s success in enforcing Masimo’s intellectual property resulted in multiple injunctions, damages and payments exceeding $1 billion, and related business agreements worth billions of dollars. In addition, Mr. Kiani is well known in the healthcare industry as a patient safety expert worldwide; founded the Patient Safety Movement Foundation and co-chaired the President’s Council of Advisors on Science and Technology’s Patient Safety Working Group and published recommendations to the President that have become a model for many organizations and countries to follow.

Mr. Chavez would bring valuable strategic, operational and transactional expertise to Masimo’s Board through his deep leadership experience in the medical device industry as a CEO and independent public company director. He led FDA product approvals, commercialization processes, and significant revenue growth at two public medical device companies, TriVascular Inc. and Advanced Neuromodulation Systems Inc. (ANSI), that culminated in strategic acquisitions of both companies. Additionally, Mr. Chavez previously served as an independent director at Endologix, Nuvectra Corp. and Advanced Medical Optics Inc., which was acquired by Abbott Laboratories in 2009. Further, as former Chair of the Medical Device Manufacturers Association, a leading industry trade association, Mr. Chavez brings a wealth of business associations and contacts that will help drive value for stockholders.

Meanwhile, Politan nominee Dr. Solomon has never worked at or served on the board of a medical device company. She has never served as a CEO , and, though a successful scientist in an area unrelated to Masimo’s business, her R&D experience is primarily in industries that face very different regulatory and operational challenges than the medical device industry. This seems to us an odd choice that demonstrates Politan’s inability to recruit CEOs or other top candidates in our industry.

We are concerned that Politan’s other nominee, Mr. Jellison, is a serial activist nominee who may not act as a true independent director but may operate at Mr. Koffey’s direction, as we believe Ms. Brennan has. In addition to Masimo and Politan, Mr. Jellison was nominated by Caligan Partners LP, an activist investment firm, as a director candidate for Anika Therapeutics less than three weeks ago, and was previously nominated by Gilead Capital LP, another activist investment firm, as a director candidate at Landauer Inc. for its 2017 annual meeting. Once again, despite having a year to plan, Politan was only able to secure a nominee who last worked as a CFO in 2016 and has since served activists. We believe this demonstrates the type of poor planning and execution that will create risk for stockholders should Politan gain control.

We are also concerned that Mr. Koffey, rather than recruiting the most qualified candidates, has selected candidates who he believes will take his direction and vote as he wishes, as we believe Ms. Brennan has. If both Politan nominees are elected, not only would Politan control the Board, but the Board would be left with only the two of us who previously served as CEOs, with Mr. Reynolds the lone former CEO of a medical technology company. We question how stripping Masimo’s Board of its industry and leadership experience will serve to benefit Masimo and its stockholders.

By contrast, Masimo remains committed to expanding the Board through a comprehensive search process focused on nominating highly qualified independent candidates with experience directly relevant to Masimo and its strategy.

YOUR VOTE FOR JOE KIANI AND CHRIS CHAVEZ ON THE GOLD PROXY CARD IS CRITICAL

Your vote for our nominees will help to ensure that Masimo continues to execute on what you have asked for and expect from us: the Consumer business separation, continued innovation to support Masimo’s premium valuation, consistent financial and operating performance and a highly qualified and expanded independent Board.

We believe electing Politan’s nominees to the Board hands control of Masimo to Politan and jeopardizes the value of your investment in Masimo. Please do not vote using any WHITE proxy card you may receive from Politan. Any vote on the WHITE proxy card will revoke your prior vote on a GOLD proxy card, and only your latest-dated proxy counts.

We have been deeply committed to engaging with you and delivering the changes you have requested. We look forward to continuing to work together to create value for all stockholders.

Thank you for your continued support,

Craig Reynolds

Bob Chapek

YOUR VOTE IS IMPORTANT—PLEASE USE THE GOLD PROXY CARD TODAY!

Simply follow the easy instructions on the enclosed GOLD proxy card to vote by internet or by signing, dating, and returning the GOLD proxy card in the postage-paid envelope provided. If you received this letter by email, you may also vote by pressing the “VOTE NOW” button in the accompanying email.

If you have questions about how to vote your shares, please call the firm assisting us with the solicitation of proxies, Innisfree M&A Incorporated, at:

1 (877) 456-3463 (toll-free from the U.S. and Canada)

or

+1 (412) 232-3651 (from other locations)

If you hold your shares in more than one account, you will receive separate notifications. Please be sure to vote ALL your accounts using the GOLD proxy card relating to each account. |

About Masimo

Masimo (NASDAQ: MASI) is a global medical technology company that develops and produces a wide array of industry-leading monitoring technologies, including innovative measurements, sensors, patient monitors, and automation and connectivity solutions. In addition, Masimo Consumer Audio is home to eight legendary audio brands, including Bowers & Wilkins, Denon, Marantz, and Polk Audio. Our mission is to improve life, improve patient outcomes, and reduce the cost of care. Masimo SET® Measure-through Motion and Low Perfusion™ pulse oximetry, introduced in 1995, has been shown in over 100 independent and objective studies to outperform other pulse oximetry technologies.1 Masimo SET® has also been shown to help clinicians reduce severe retinopathy of prematurity in neonates,2 improve CCHD screening in newborns3 and, when used for continuous monitoring with Masimo Patient SafetyNet™ in post-surgical wards, reduce rapid response team activations, ICU transfers, and costs.4-7 Masimo SET® is estimated to be used on more than 200 million patients in leading hospitals and other healthcare settings around the world,8 and is the primary pulse oximetry at 9 of the top 10 hospitals as ranked in the 2022-23 U.S. News and World Report Best Hospitals Honor Roll.9 In 2005, Masimo introduced rainbow® Pulse CO-Oximetry technology, allowing noninvasive and continuous monitoring of blood constituents that previously could only be measured invasively, including total hemoglobin (SpHb®), oxygen content (SpOC™), carboxyhemoglobin (SpCO®), methemoglobin (SpMet®), Pleth Variability Index (PVi®), RPVi™ (rainbow® PVi), and Oxygen Reserve Index (ORi™). In 2013, Masimo introduced the Root® Patient Monitoring and Connectivity Platform, built from the ground up to be as flexible and expandable as possible to facilitate the addition of other Masimo and third-party monitoring technologies; key Masimo additions include Next Generation SedLine® Brain Function Monitoring, O3® Regional Oximetry, and ISA™ Capnography with NomoLine® sampling lines. Masimo’s family of continuous and spot-check monitoring Pulse CO-Oximeters® includes devices designed for use in a variety of clinical and non-clinical scenarios, including tetherless, wearable technology, such as Radius-7®, Radius PPG®, and Radius VSM™, portable devices like Rad-67®, fingertip pulse oximeters like MightySat® Rx, and devices available for use both in the hospital and at home, such as Rad-97® and the Masimo W1® medical watch. Masimo hospital and home automation and connectivity solutions are centered around the Masimo Hospital Automation™ platform, and include Iris® Gateway, iSirona™, Patient SafetyNet, Replica®, Halo ION®, UniView®, UniView :60™, and Masimo SafetyNet®. Its growing portfolio of health and wellness solutions includes Radius Tº®, Masimo W1 Sport, and Masimo Stork™. Additional information about Masimo and its products may be found at www.masimo.com. Published clinical studies on Masimo products can be found at www.masimo.com/evidence/featured-studies/feature/.

RPVi has not received FDA 510(k) clearance and is not available for sale in the United States. The use of the trademark Patient SafetyNet is under license from University HealthSystem Consortium.

References

- Published clinical studies on pulse oximetry and the benefits of Masimo SET® can be found on our website at http://www.masimo.com. Comparative studies include independent and objective studies which are comprised of abstracts presented at scientific meetings and peer-reviewed journal articles.

- Castillo A et al. Prevention of Retinopathy of Prematurity in Preterm Infants through Changes in Clinical Practice and SpO2 Technology. Acta Paediatr. 2011 Feb;100(2):188-92.

- de-Wahl Granelli A et al. Impact of pulse oximetry screening on the detection of duct dependent congenital heart disease: a Swedish prospective screening study in 39,821 newborns. BMJ. 2009;Jan 8;338.

- Taenzer A et al. Impact of pulse oximetry surveillance on rescue events and intensive care unit transfers: a before-and-after concurrence study. Anesthesiology. 2010:112(2):282-287.

- Taenzer A et al. Postoperative Monitoring – The Dartmouth Experience. Anesthesia Patient Safety Foundation Newsletter. Spring-Summer 2012.

- McGrath S et al. Surveillance Monitoring Management for General Care Units: Strategy, Design, and Implementation. The Joint Commission Journal on Quality and Patient Safety. 2016 Jul;42(7):293-302.

- McGrath S et al. Inpatient Respiratory Arrest Associated With Sedative and Analgesic Medications: Impact of Continuous Monitoring on Patient Mortality and Severe Morbidity. J Patient Saf. 2020 14 Mar. DOI: 10.1097/PTS.0000000000000696.

- Estimate: Masimo data on file.

- http://health.usnews.com/health-care/best-hospitals/articles/best-hospitals-honor-roll-and-overview.

Forward-Looking Statements

This communication includes forward-looking statements as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, in connection with the Private Securities Litigation Reform Act of 1995. These forward-looking statements include, among others, statements regarding Masimo’s expectations for full-year 2024 financial guidance; the 2024 Annual Meeting of Stockholders (the “2024 Annual Meeting”) of Masimo and the potential stockholder approval of the Board’s nominees; the proposed separation of Masimo’s consumer business, including the potential timing and structure thereof and the expectation that the proposed separation will maximize shareholder value or be the best path for success; any potential joint venture involving Masimo’s consumer business and any proposed new terms thereof; Masimo’s expectation that OriTM will drive significant growth in rainbowTM revenues and margins and have a positive effect on Masimo’s broader hospital relationships and contracting efforts; Masimo’s expectation that its innovation-led growth trajectory will drive leverage on its R&D, sales, and corporate and administrative expenses and account for a significant portion of that margin improvement; Masimo’s long-term outlook; demand for Masimo’s products; anticipated revenue and earnings growth; Masimo’s financial condition, results of operations and business generally; expectations regarding Masimo’s ability to design and deliver innovative new noninvasive technologies and reduce the cost of care; and demand for Masimo’s products and technologies; Masimo’s long-term outlook; Masimo’s ability to continue in its leadership in delivering innovative solutions to clinicians and patients worldwide; and anticipated revenue, operating margins and earnings growth. These forward-looking statements are based on current expectations about future events affecting Masimo and are subject to risks and uncertainties, all of which are difficult to predict and many of which are beyond Masimo’s control and could cause its actual results to differ materially and adversely from those expressed in its forward-looking statements as a result of various risk factors, including, but not limited to (i) uncertainties regarding a potential separation of Masimo’s consumer business, (ii) uncertainties regarding future actions that may be taken by Politan in furtherance of its nomination of director candidates for election at the 2024 Annual Meeting, (iii) the potential cost and management distraction attendant to Politan’s nomination of director nominees at the 2024 Annual Meeting and (iv) factors discussed in the “Risk Factors” section of Masimo’s most recent periodic reports filed with the Securities and Exchange Commission (“SEC”), which may be obtained for free at the SEC’s website at www.sec.gov. Although Masimo believes that the expectations reflected in its forward-looking statements are reasonable, the Company does not know whether its expectations will prove correct. All forward-looking statements included in this communication are expressly qualified in their entirety by the foregoing cautionary statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of today’s date. Masimo does not undertake any obligation to update, amend or clarify these statements or the “Risk Factors” contained in the Company’s most recent reports filed with the SEC, whether as a result of new information, future events or otherwise, except as may be required under the applicable securities laws.

Additional Information Regarding the 2024 Annual Meeting of Stockholders and Where to Find It

The Company has filed a definitive proxy statement containing a form of GOLD proxy card with the SEC in connection with its solicitation of proxies for its 2024 Annual Meeting. THE COMPANY’S STOCKHOLDERS ARE STRONGLY ENCOURAGED TO READ THE DEFINITIVE PROXY STATEMENT (AND ANY AMENDMENTS AND SUPPLEMENTS THERETO) AND ACCOMPANYING GOLD PROXY CARD AS THEY WILL CONTAIN IMPORTANT INFORMATION. Stockholders may obtain the proxy statement, any amendments or supplements to the proxy statement and other documents as and when filed by the Company with the SEC without charge from the SEC’s website at www.sec.gov.

Certain Information Regarding Participants

The Company, its directors and certain of its executive officers and employees may be deemed to be participants in connection with the solicitation of proxies from the Company’s stockholders in connection with the matters to be considered at the 2024 Annual Meeting. Information regarding the direct and indirect interests, by security holdings or otherwise, of the Company’s directors and executive officers in the Company is included in the Company’s definitive proxy statement for the 2024 Annual Meeting, and any changes thereto may be found in any amendments or supplements to the proxy statement and other documents as and when filed by the Company with the SEC, which can be found through the SEC’s website at www.sec.gov.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240617740544/en/

Contacts

Investor Contact: Eli Kammerman

(949) 297-7077

ekammerman@masimo.com

Media Contact: Evan Lamb

(949) 396-3376

elamb@masimo.com