Artificial intelligence’s (AI) data appetite is insatiable, and that hunger is now lifting an unlikely hero: hard drives. As generative AI and cloud computing explode, data centers are scrambling for more high-capacity storage, breathing new life into Seagate Technology (STX). The once-steady storage maker is now riding the AI wave, with its drives becoming the silent backbone of the world’s data boom.

STX shares have been soaring this year and recently hit record highs after a blowout fiscal first quarter. Seagate's focus on high-capacity hard drives for cloud giants is paying off big time — most of its production is already locked under contract through 2026, giving the company clear visibility into 2027. Simply put, Seagate seems to have carved out a strong lane in the AI-fueled data boom.

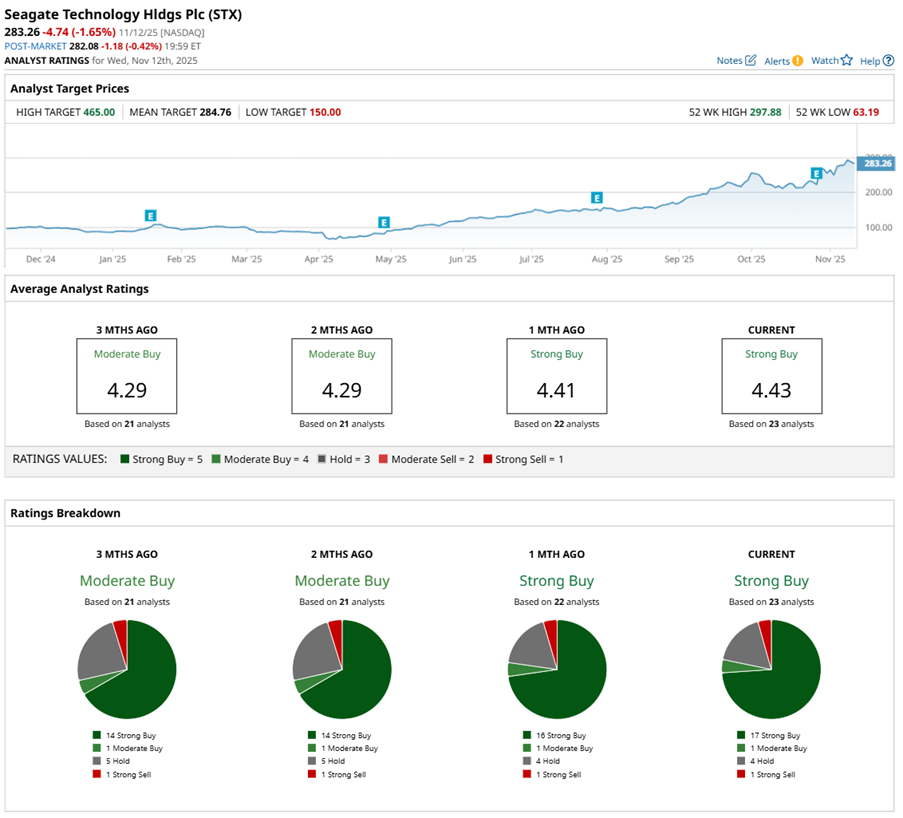

Wall Street’s confidence in Seagate is hitting new highs. Loop Capital just boosted its price target to a Street-high $465 from $350, calling the surge in demand “durable” and probably only getting started.

With AI and data centers driving a new storage boom, should you be grabbing STX stock right now?

About Seagate Technology Stock

Founded in 1978 and headquartered in Fremont, California, Seagate has spent decades shaping the backbone of the digital world. The company develops and delivers cutting-edge data storage technologies, from high-capacity hard disk drives (HDDs) and solid-state drives (SSDs) to its Lyve edge-to-cloud platform — powering everything from personal devices to massive data centers. Seagate’s products span the globe, serving OEMs, distributors, and retailers across multiple continents.

The pioneer behind the world’s first 5.25-inch hard drive, Seagate remains at the forefront of storage innovation. With over four zettabytes of capacity shipped, its Mozaic technology represents the next leap, packing more data into less space while reducing energy costs. By enabling sustainable, scalable, and high-performance storage, Seagate continues to fuel the world’s ever-growing demand for data and digital progress.

Valued at a market capitalization of $55 billion, the data storage company has been one of the brightest standouts in the S&P 500 Index ($SPX) this year, riding the wave of an AI-fueled storage boom.

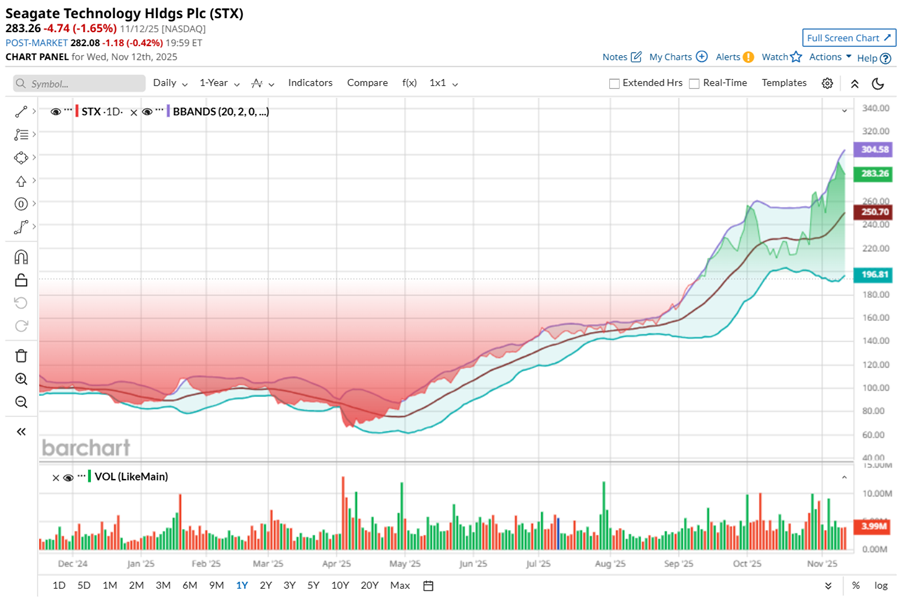

On Oct. 29, just a day after its stellar Q1 earnings, STX shares exploded over 19% in a single session, later touching a record $297.88 on Nov. 12. Over the past six months, the stock has skyrocketed 145%, and an astounding 199% on a year-to-date (YTD) basis, fueled by relentless demand for high-capacity drives from hyperscale data centers.

Technically, STX stock remains well above the midline of its Bollinger Bands, signaling sustained upward momentum even amid brief pullbacks. The widening of the bands suggests growing volatility, but also strong buying pressure behind the rally. This meteoric rise mirrors Seagate’s deepening role in the AI-driven data boom, as investments in mass-capacity storage and cloud infrastructure accelerate.

For a stock that has been on a tear, Seagate’s valuation still feels surprisingly grounded. Trading at 26 times earnings, it sits below the sector average — a rarity in today’s AI-fueled tech world. That’s what makes STX so compelling — it’s a pure play on the data and AI storage boom, yet still priced attractively for investors chasing both value and growth.

What seals the deal is Seagate’s quiet consistency. The company has paid quarterly dividends for 13 straight years, and recently sweetened the pot with a 3% hike. Its next payout of $0.74 per share, scheduled for Jan. 9, gives it a 1.04% yield — roughly double that of the S&P 500 Technology Sector SPDR’s (XLK) 0.53% yield.

In fiscal Q1 2026, Seagate returned $182 million to shareholders — $153 million via dividends and $29 million through buybacks. For investors seeking a balanced play between AI-driven upside and dependable shareholder returns, Seagate strikes that rare harmony between momentum and maturity.

A Snapshot of Seagate Technology’s Stellar Q3 Results

Seagate Technology turned heads on Oct. 28 when it dropped its fiscal Q1 2026 earnings report after the bell, and the next day, STX stock rocketed by the high teens. The data storage giant did not just beat expectations, but smashed them impressively, posting solid growth on both the top and bottom lines, powered by the unrelenting appetite for cloud data.

Non-GAAP revenue hit $2.63 billion, up 21% year-over-year (YOY), while non-GAAP EPS rose 65% annually to $2.61. The bottom line did not just top the Street’s projections but even exceeded the high end of management’s own guidance.

The top-line surge came mainly from data centers — the true engine of Seagate’s recovery — where demand for high-capacity hard drives exploded. The data center segment accounted for 80% of total revenue, which jumped 34% annually and grew 13% sequentially to $2.1 billion. The trend was not a fluke. Cloud service providers kept the pipelines busy, and even enterprise OEM demand began to stir again.

Meanwhile, the Edge IoT segment — which caters to consumer and client markets — took a breather at $515 million, down 11% sequentially and 12% YOY. Still, Seagate expects this arm to bounce back in the December quarter with seasonal gains in VIA, edge, and consumer products.

Seagate shipped 182 exabytes of HDD storage this quarter — a 32% YOY rise and 12% sequential rise — with 159 exabytes delivered to data center customers. Nearly 80% of nearline volume now consists of 24 terabytes or higher drives, proving customers are embracing higher-capacity solutions at scale.

Then comes the ace in Seagate’s deck: Mozaic HAMR drives. Qualified by five major cloud providers and built for high-performance AI-driven workloads, these next-gen drives combine durability, density, and efficiency. Over 1 million Mozaic units shipped during the September quarter alone, setting the tone for what could be Seagate’s most important growth lever yet.

Financially, Seagate’s footing looks firm. Cash and equivalents stood at $1.1 billion, while long-term debt edged down to $4.9 billion. Net cash provided by operating activities rose impressively to $532 million, and free cash flow came in at $427 million, with management guiding for stronger cash generation in the next quarter.

Looking ahead, management’s tone is confident. Q2 revenue is anticipated to be $2.7 billion, plus or minus $100 million. Non-GAAP EPS is estimated to be around $2.75, plus or minus $0.20.

Meanwhile, analysts tracking Seagate anticipate fiscal Q2 2026 EPS to rise 41% YOY to $2.56. Looking ahead to fiscal 2026, profit is expected to surge to $10.09 per share, up 39% annually, then rise by another 33% annually to $13.39 per share in fiscal 2027.

What Do Analysts Think About Seagate Technology Stock?

Wall Street’s tone on Seagate has turned distinctly upbeat after its blowout quarter. Evercore ISI analyst Amit Daryanani stuck with an “Outperform” rating and a $330 target, saying Seagate is “well-positioned to capture growing demand.” Barclays analyst Tom O’Malley called the market “desperate for storage,” keeping an “Equal-Weight” stance but hiking his target to $240 from $200.

Wedbush analyst Matt Bryson also raised his price target to $290 from $260 and kept an “Outperform” rating on STX, citing Seagate’s solid fundamentals and resilient industry backdrop. Wedbush sees no reason to alter its bullish stance, expecting a significant margin expansion in late 2026 and 2027, which could unlock more favorable terms and extend Seagate’s growth runway.

The loudest cheer among analysts came from Loop Capital, which turned decisively bullish, hiking its target to a Street-high $465 from $350 while maintaining a “Buy” rating. The firm sees hard drive capacity demand rising sharply through 2026 and calls Seagate’s higher-capacity drive pricing “materially accretive” — fueling what it believes is a durable, early-stage re-rating for the stock.

Wall Street’s tone is becoming more bullish on STX stock. The shares have a consensus “Strong Buy” rating overall — an upgrade from a “Moderate Buy” rating two months ago. Of the 23 analysts rating the stock, 17 recommend a “Strong Buy” rating, one has a “Moderate Buy,” four are cautious with a “Hold” rating, and one analyst is outright skeptical with a “Strong Sell” rating.

With STX stock recently slipping, the consensus price target of $288.10 represents 12% potential upside from current levels. Loop Capital’s Street-high price target of $465 implies that STX could rise as much as 80% from here.

Conclusion

Seagate has been spinning heads this year, riding the heart of the AI revolution. With earnings soaring and analysts cheering, STX stock’s momentum looks far from over. Add in a steady dividend and generous buybacks, and investors have a stock that rewards patience. Along with storing data, Seagate is storing serious investor confidence.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Warren Buffett Says Investors Should Measure Their Investing Success On ‘Slugging Percentage, Not Batting Average’

- Oklo Is ‘Setting the Stage’ for a Revolution in Nuclear Energy. Should You Buy OKLO Stock Here?

- This Semiconductor Stock Just Got a New Street-High Price Target. Should You Buy It Now?

- Nasdaq Year-End Playbook Decode 5-Year Correlations and Seasonal Q4