Since September 2025, FTI Consulting has been in a holding pattern, posting a small loss of 2.2% while floating around $165.02. The stock also fell short of the S&P 500’s 5.1% gain during that period.

Is there a buying opportunity in FTI Consulting, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is FTI Consulting Not Exciting?

We're sitting this one out for now. Here are three reasons why FCN doesn't excite us and a stock we'd rather own.

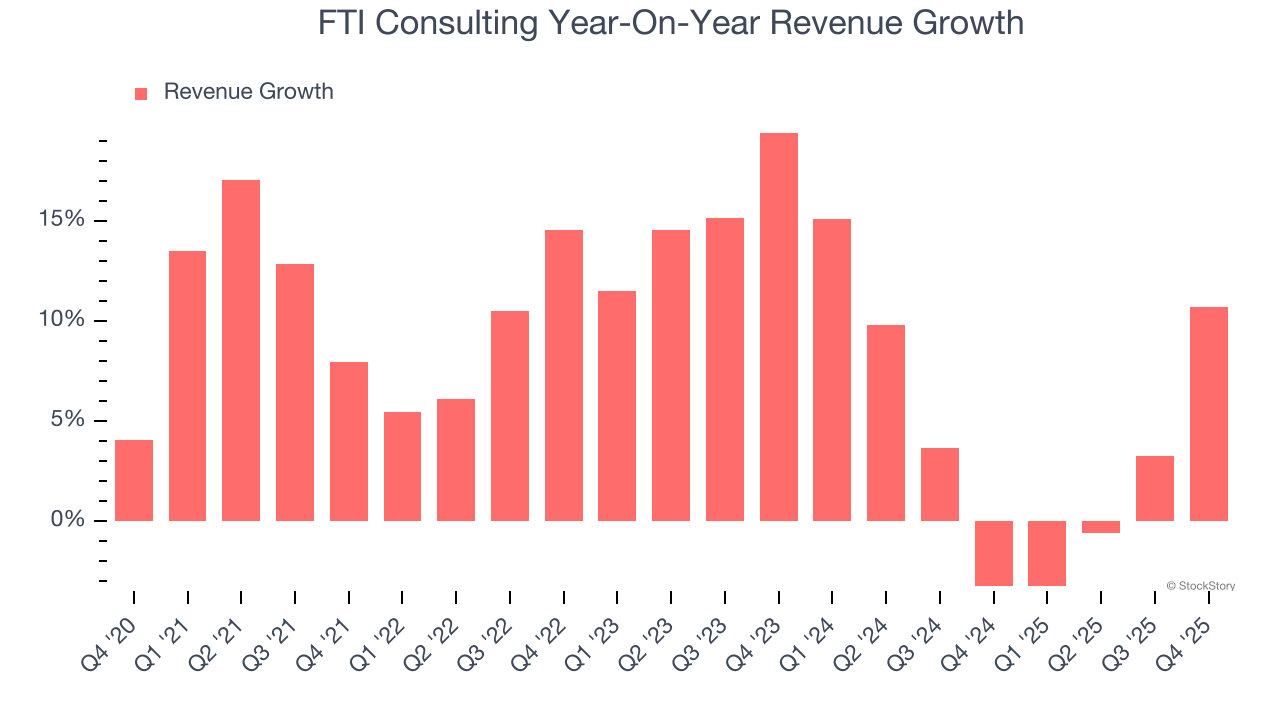

1. Lackluster Revenue Growth

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. FTI Consulting’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.2% over the last two years was well below its five-year trend.

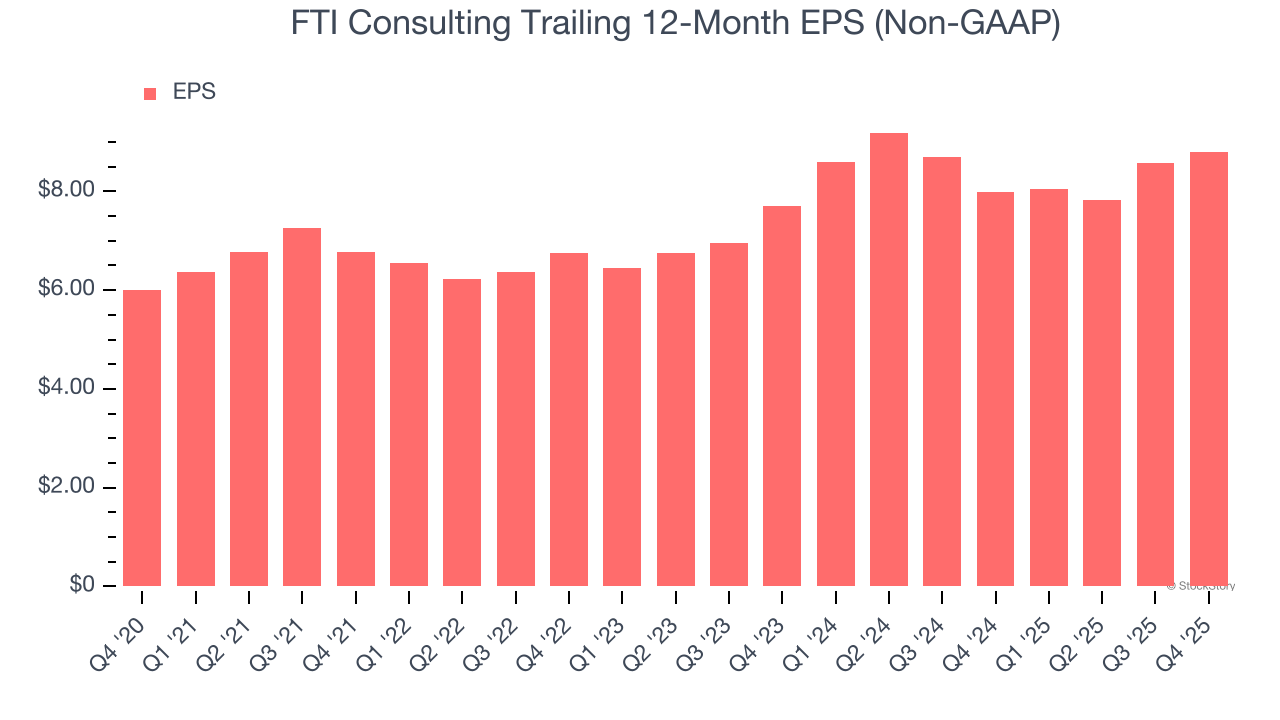

2. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

FTI Consulting’s EPS grew at an unimpressive 6.8% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 4.2% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

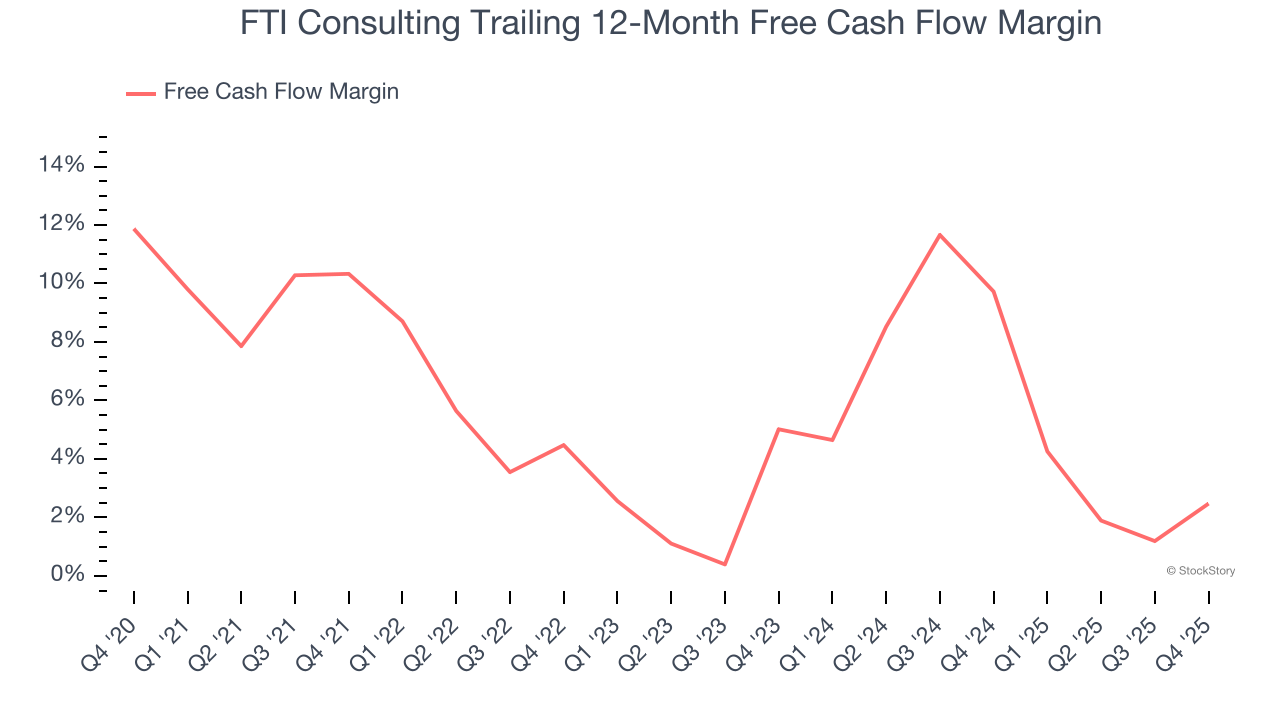

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, FTI Consulting’s margin dropped by 7.9 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. FTI Consulting’s free cash flow margin for the trailing 12 months was 2.5%.

Final Judgment

FTI Consulting isn’t a terrible business, but it isn’t one of our picks. With its shares lagging the market recently, the stock trades at 17.9× forward P/E (or $165.02 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than FTI Consulting

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.