Over the last six months, BancFirst’s shares have sunk to $112.95, producing a disappointing 15.9% loss - a stark contrast to the S&P 500’s 5.1% gain. This might have investors contemplating their next move.

Is now the time to buy BancFirst, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is BancFirst Not Exciting?

Even with the cheaper entry price, we don't have much confidence in BancFirst. Here are three reasons we avoid BANF and a stock we'd rather own.

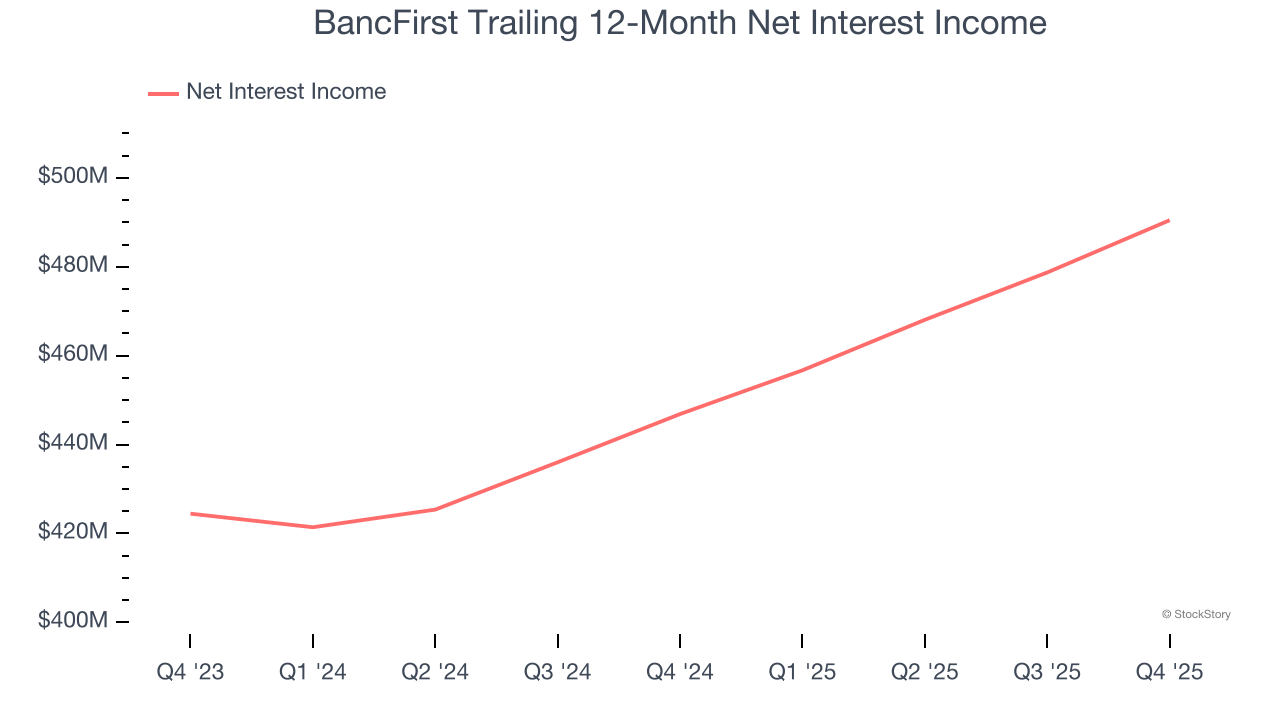

1. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

BancFirst’s net interest income has grown at a 9.8% annualized rate over the last five years, slightly worse than the broader banking industry and in line with its total revenue. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect BancFirst’s net interest income to rise by 4.3%, a deceleration versus its 7.5% annualized growth for the past two years. This projection is below its 7.5% annualized growth rate for the past two years.

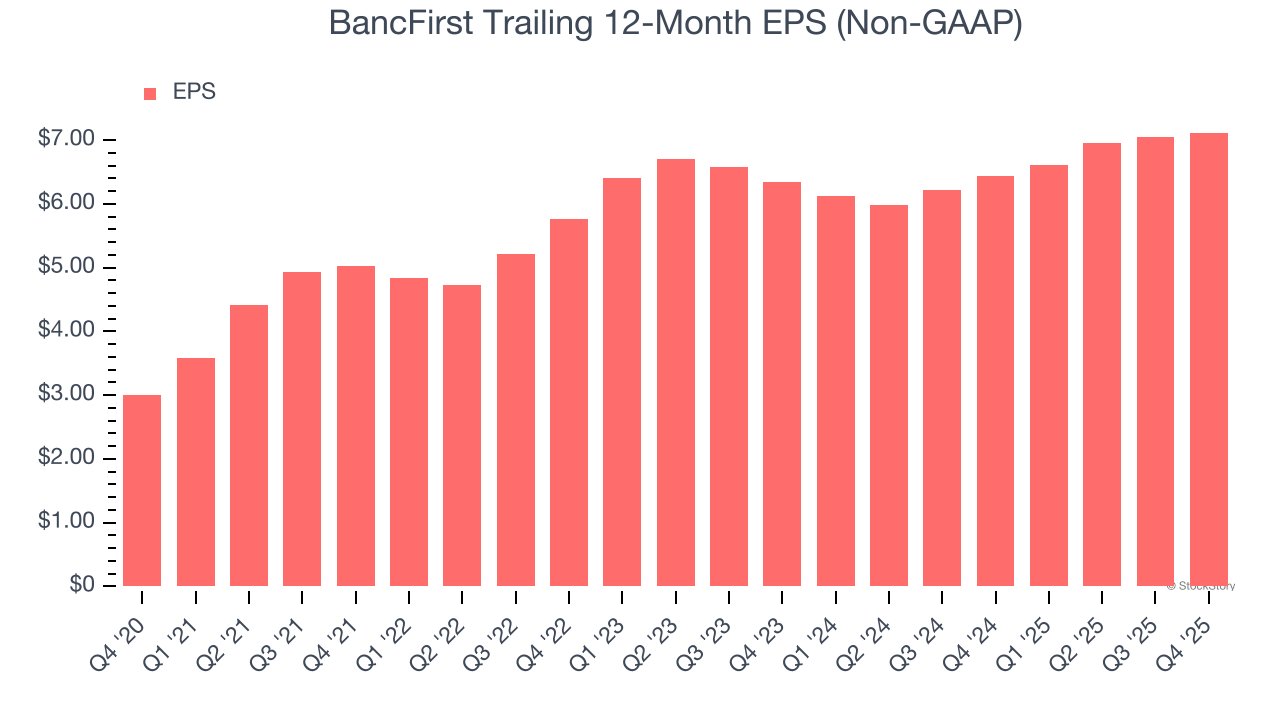

3. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

BancFirst’s weak 6% annual EPS growth over the last two years aligns with its revenue trend. This tells us it maintained its per-share profitability as it expanded.

Final Judgment

BancFirst’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 1.9× forward P/B (or $112.95 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of BancFirst

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.