Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at MillerKnoll (NASDAQ: MLKN) and its peers.

This is a sector that encompasses many types of business, and so it follows that a number of trends will impact the space. For industrial and environmental services companies, for example, trends around environmental compliance and increasing corporate ESG commitments matter while for safety and security services companies, the intersection of physical security, cybersecurity, and workplace safety regulations are the topics du jour. Broadly, AI and automation could be tailwinds for companies in the space that invest wisely. On the other hand, shifting regulatory frameworks could force continual changes in go-to-market and costly investments.

The 18 business services & supplies stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 3.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

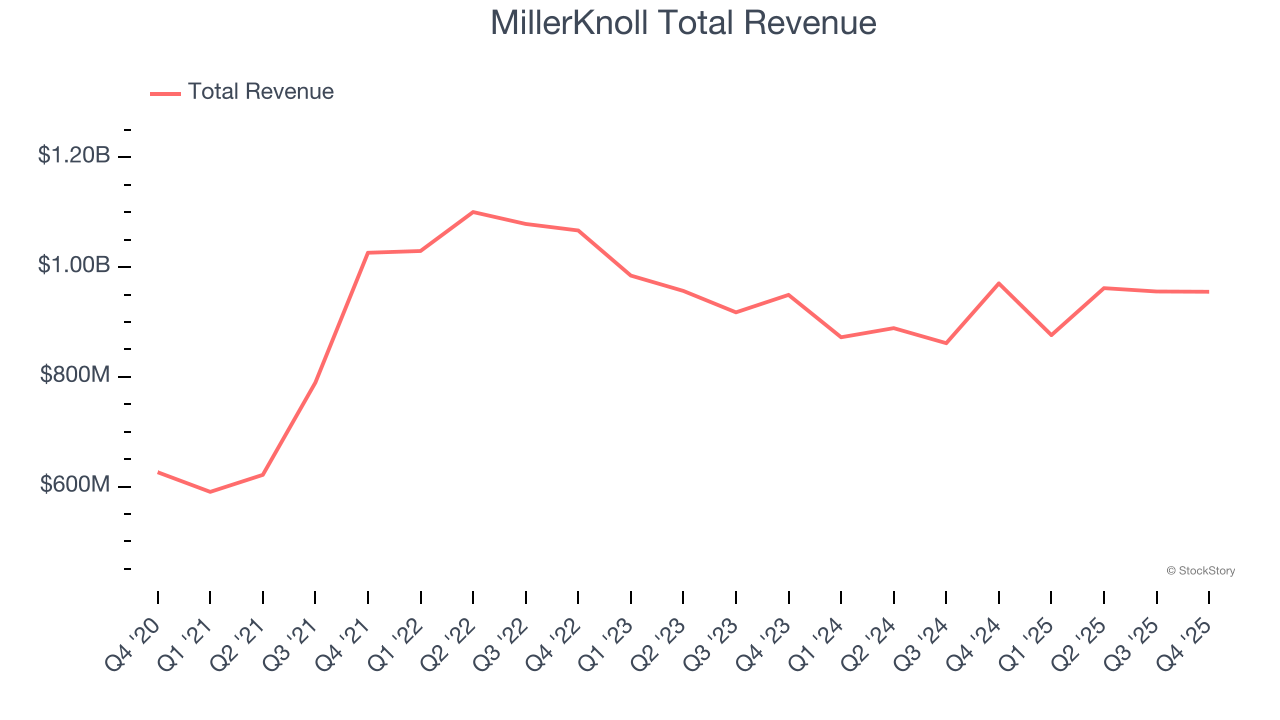

MillerKnoll (NASDAQ: MLKN)

Created through the 2021 merger of industry icons Herman Miller and Knoll, MillerKnoll (NASDAQ: MLKN) designs, manufactures, and distributes interior furnishings for offices, healthcare facilities, educational settings, and homes worldwide.

MillerKnoll reported revenues of $955.2 million, down 1.6% year on year. This print exceeded analysts’ expectations by 1.3%. Overall, it was an exceptional quarter for the company with an impressive beat of analysts’ EPS guidance for next quarter estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Interestingly, the stock is up 14.9% since reporting and currently trades at $20.14.

Is now the time to buy MillerKnoll? Access our full analysis of the earnings results here, it’s free.

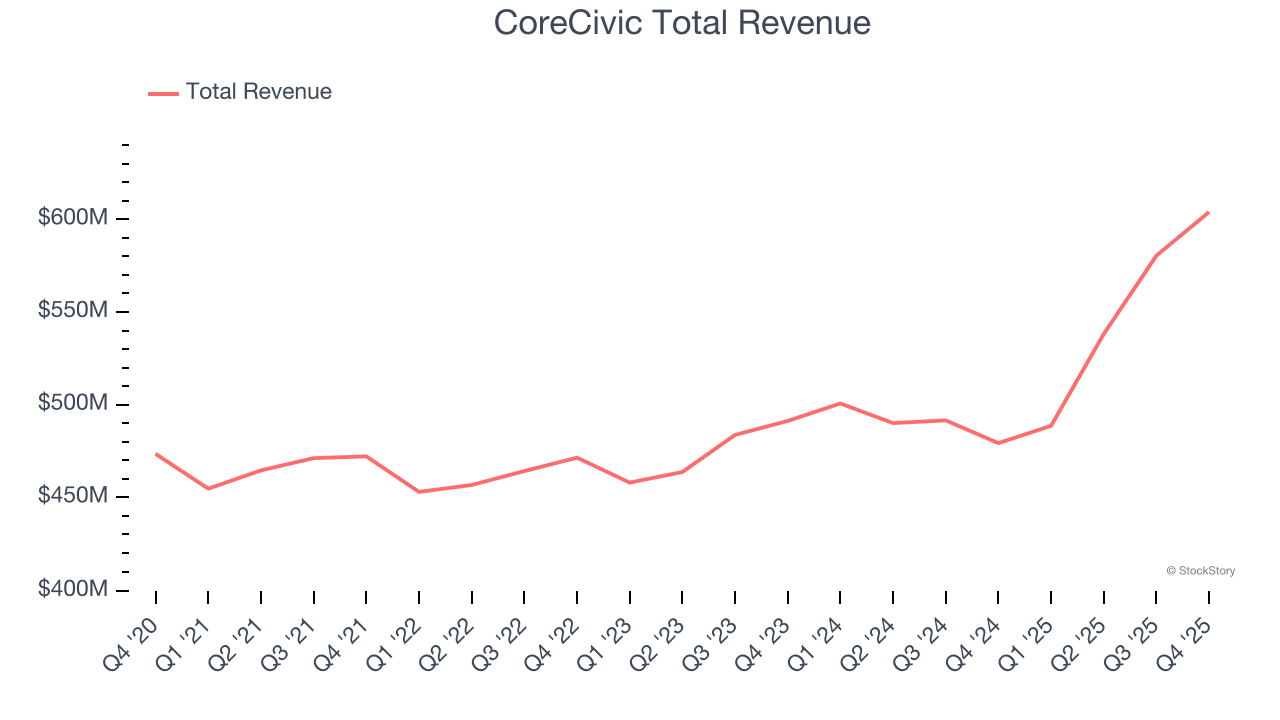

Best Q4: CoreCivic (NYSE: CXW)

Originally founded in 1983 as the first private prison company in the United States, CoreCivic (NYSE: CXW) operates correctional facilities, detention centers, and residential reentry programs for government agencies across the United States.

CoreCivic reported revenues of $604 million, up 26% year on year, outperforming analysts’ expectations by 6%. The business had an incredible quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.4% since reporting. It currently trades at $17.68.

Is now the time to buy CoreCivic? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Copart (NASDAQ: CPRT)

Starting as a single salvage yard in California in 1982, Copart (NASDAQ: CPRT) operates an online auction platform that connects sellers of damaged and salvage vehicles with buyers ranging from dismantlers and rebuilders to used car dealers and exporters.

Copart reported revenues of $1.12 billion, down 3.6% year on year, falling short of analysts’ expectations by 5%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EPS estimates.

Copart delivered the weakest performance against analyst estimates in the group. The stock is flat since the results and currently trades at $37.94.

Read our full analysis of Copart’s results here.

Pitney Bowes (NYSE: PBI)

With a century-long history dating back to 1920 and processing over 15 billion pieces of mail annually, Pitney Bowes (NYSE: PBI) provides shipping, mailing technology, logistics, and financial services to businesses of all sizes.

Pitney Bowes reported revenues of $477.6 million, down 7.5% year on year. This number came in 1.2% below analysts' expectations. Taking a step back, it was still a strong quarter as it produced a beat of analysts’ EPS estimates and a solid beat of analysts’ full-year EPS guidance estimates.

The stock is up 4.8% since reporting and currently trades at $10.74.

Read our full, actionable report on Pitney Bowes here, it’s free.

HNI (NYSE: HNI)

With roots dating back to 1944 and a significant acquisition of Kimball International in 2023, HNI (NYSE: HNI) manufactures and sells office furniture systems, seating, and storage solutions, as well as residential fireplaces and heating products.

HNI reported revenues of $888.4 million, up 38.3% year on year. This result beat analysts’ expectations by 24.8%. More broadly, it was a slower quarter as it logged a significant miss of analysts’ EPS estimates.

HNI achieved the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is down 7.7% since reporting and currently trades at $44.84.

Read our full, actionable report on HNI here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.