The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how maintenance and repair distributors stocks fared in Q4, starting with MSC Industrial (NYSE: MSM).

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

The 9 maintenance and repair distributors stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 2.1%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.2% since the latest earnings results.

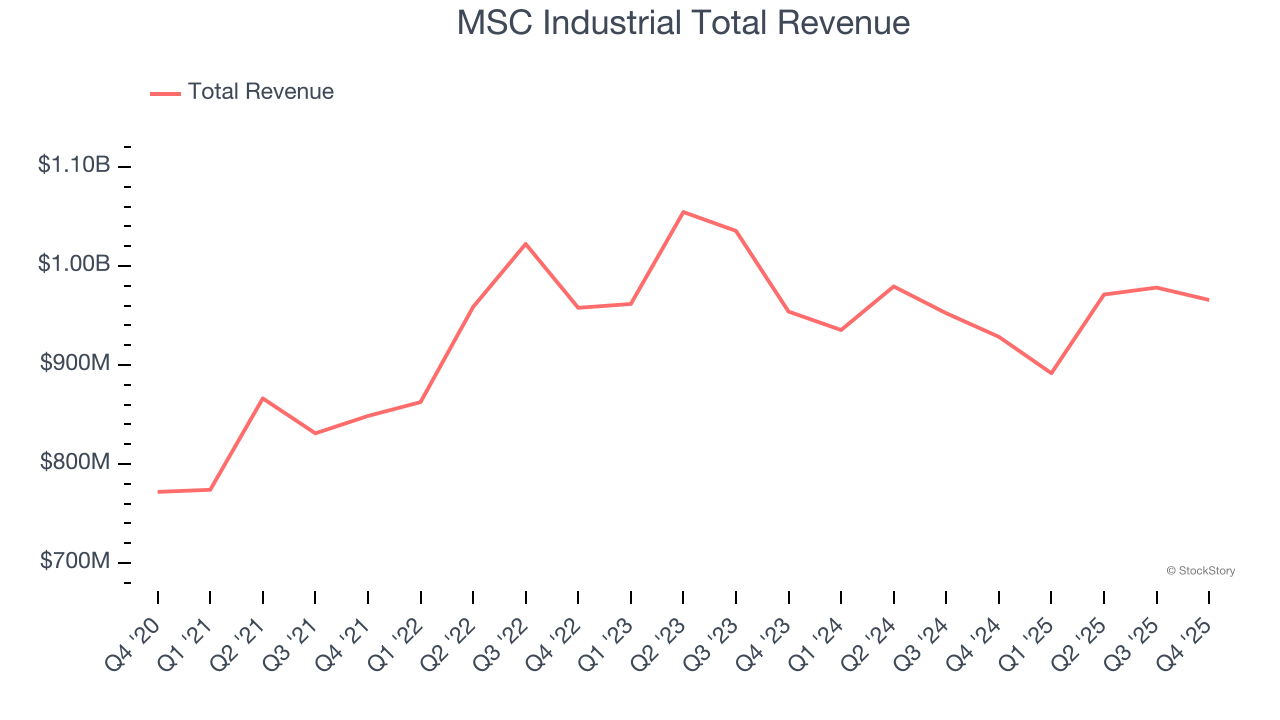

MSC Industrial (NYSE: MSM)

Founded in NYC’s Little Italy, MSC Industrial Direct (NYSE: MSM) provides industrial supplies and equipment, offering vast and reliable selection for customers such as contractors

MSC Industrial reported revenues of $965.7 million, up 4% year on year. This print was in line with analysts’ expectations, and overall, it was a strong quarter for the company with a solid beat of analysts’ EBITDA estimates and a decent beat of analysts’ adjusted operating income estimates.

Interestingly, the stock is up 7.4% since reporting and currently trades at $91.25.

Is now the time to buy MSC Industrial? Access our full analysis of the earnings results here, it’s free.

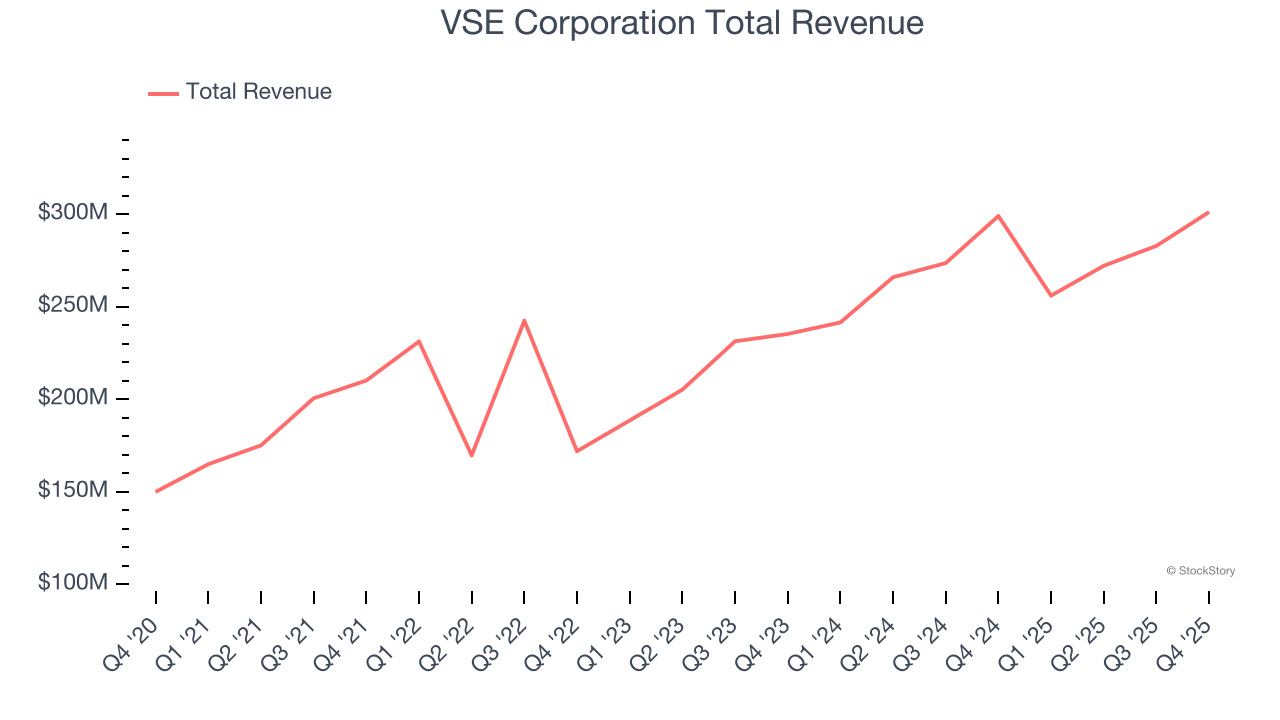

Best Q4: VSE Corporation (NASDAQ: VSEC)

With roots dating back to 1959 and a strategic focus on extending the life of transportation assets, VSE Corporation (NASDAQ: VSEC) provides aftermarket parts distribution and maintenance, repair, and overhaul services for aircraft and vehicle fleets in commercial and government markets.

VSE Corporation reported revenues of $301.2 million, flat year on year, outperforming analysts’ expectations by 4.6%. The business had an incredible quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 5% since reporting. It currently trades at $208.52.

Is now the time to buy VSE Corporation? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Distribution Solutions (NASDAQ: DSGR)

Founded in 1952, Distribution Solutions (NASDAQ: DSGR) provides supply chain solutions and distributes industrial, safety, and maintenance products to various industries.

Distribution Solutions reported revenues of $481.6 million, flat year on year, falling short of analysts’ expectations by 3%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Distribution Solutions delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 35% since the results and currently trades at $19.31.

Read our full analysis of Distribution Solutions’s results here.

Transcat (NASDAQ: TRNS)

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ: TRNS) provides measurement instruments and supplies.

Transcat reported revenues of $83.86 million, up 25.6% year on year. This print surpassed analysts’ expectations by 4.1%. More broadly, it was a slower quarter as it logged a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

Transcat pulled off the fastest revenue growth among its peers. The stock is up 16.6% since reporting and currently trades at $73.83.

Read our full, actionable report on Transcat here, it’s free.

W.W. Grainger (NYSE: GWW)

Founded as a supplier of motors, W.W. Grainger (NYSE: GWW) provides maintenance, repair, and operating (MRO) supplies and services to businesses and institutions.

W.W. Grainger reported revenues of $4.43 billion, up 4.5% year on year. This result topped analysts’ expectations by 0.7%. Zooming out, it was a slower quarter as it recorded a significant miss of analysts’ EPS estimates and full-year EPS guidance slightly missing analysts’ expectations.

The stock is down 2.5% since reporting and currently trades at $1,068.

Read our full, actionable report on W.W. Grainger here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.