Looking back on electrical systems stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Powell (NASDAQ: POWL) and its peers.

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

The 14 electrical systems stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 1.8% while next quarter’s revenue guidance was 1.3% below.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

Powell (NASDAQ: POWL)

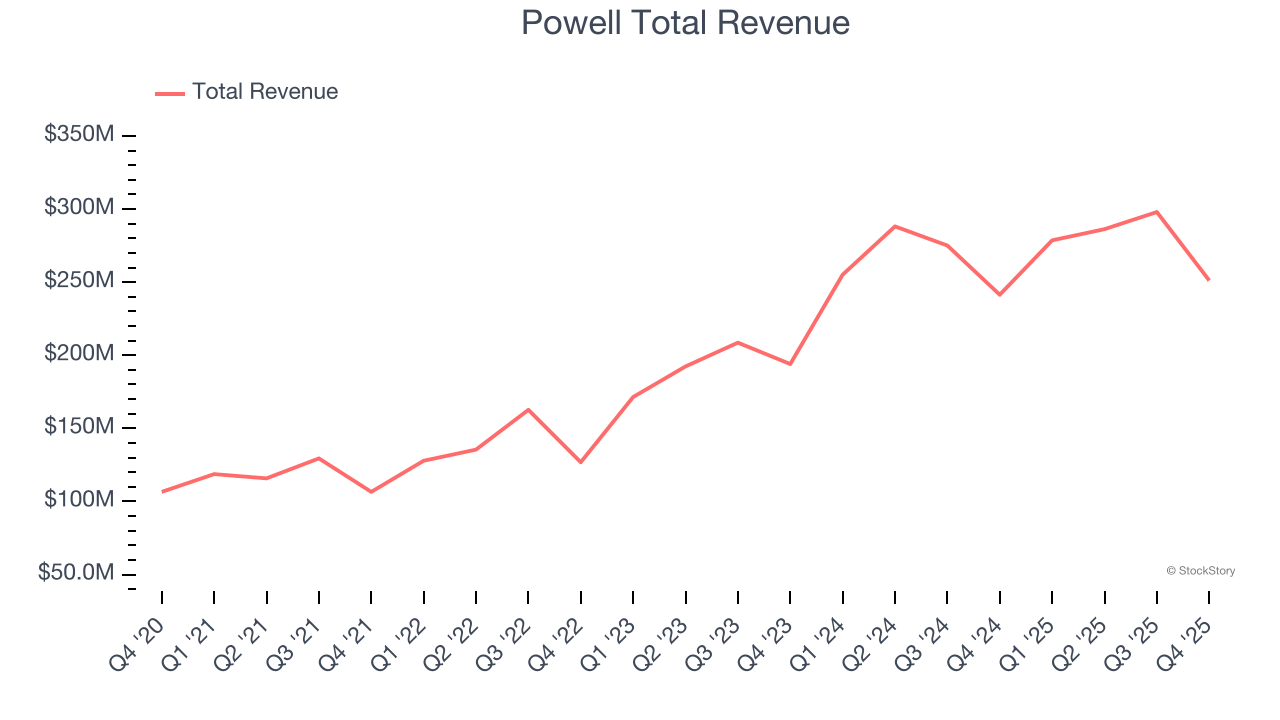

Originally a metal-working shop supporting local petrochemical facilities, Powell (NYSE: POWL) has grown from a small Houston manufacturer to a global provider of electrical systems.

Powell reported revenues of $251.2 million, up 4% year on year. This print fell short of analysts’ expectations by 2.1%, but it was still a satisfactory quarter for the company with an impressive beat of analysts’ EBITDA estimates but a significant miss of analysts’ revenue estimates.

Brett A. Cope, Powell’s Chairman and Chief Executive Officer, stated, “Ongoing levels of solid project execution drove a strong start to our fiscal year, as we delivered a gross margin of 28.4% despite the typical seasonality and lower volumes that define our first quarter. We also experienced high levels of order activity across most of the markets we serve, as the $439 million of awards booked was the highest quarterly total in over two years and led to a book-to-bill ratio of 1.7. Activity in our Commercial & Other Industrial market has accelerated considerably, as this market accounted for almost one-half of our awards in the quarter, and the average project size that we are pursuing and winning has grown substantially, highlighted by our first megaproject(3) order in the data center end market. Also, we won a very large LNG award to support a project along the U.S. Gulf Coast, as this market continues to exhibit favorable dynamics. Overall, our fiscal year is off to a great start, and our results continue to demonstrate both the breadth of investment in electrical infrastructure, as well as Powell’s unique ability to deliver engineered-to-order solutions.”

Interestingly, the stock is up 14.9% since reporting and currently trades at $520.93.

Is now the time to buy Powell? Access our full analysis of the earnings results here, it’s free.

Best Q4: LSI (NASDAQ: LYTS)

Enhancing commercial environments, LSI (NASDAQ: LYTS) provides lighting and display solutions for businesses and retailers.

LSI reported revenues of $147 million, flat year on year, outperforming analysts’ expectations by 4.9%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ revenue estimates.

The market seems content with the results as the stock is up 1.1% since reporting. It currently trades at $20.61.

Is now the time to buy LSI? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Whirlpool (NYSE: WHR)

Credited with introducing the first automatic washing machine, Whirlpool (NYSE: WHR) is a manufacturer of a variety of home appliances.

Whirlpool reported revenues of $4.10 billion, flat year on year, falling short of analysts’ expectations by 3.7%. It was a softer quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Whirlpool delivered the highest full-year guidance raise but had the weakest performance against analyst estimates in the group. As expected, the stock is down 14.6% since the results and currently trades at $69.08.

Read our full analysis of Whirlpool’s results here.

Verra Mobility (NASDAQ: VRRM)

Aiming to wrap technology and data around a historically manual and paper-based industry, Verra Mobility (NYSE: VRRM) is a leading provider of smart mobility technology to address tolls and violations, title and registration services, as well as safety and traffic enforcement.

Verra Mobility reported revenues of $257.9 million, up 16.4% year on year. This result beat analysts’ expectations by 6.7%. However, it was a slower quarter as it logged a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EPS estimates.

Verra Mobility delivered the biggest analyst estimates beat among its peers. The stock is down 9.3% since reporting and currently trades at $16.97.

Read our full, actionable report on Verra Mobility here, it’s free.

GE Vernova (NYSE: GEV)

Born from the energy business of industrial giant General Electric in a 2023 spin-off, GE Vernova (NYSE: GEV) designs, manufactures, and services power generation equipment and grid technologies to help customers build more reliable and sustainable electric systems.

GE Vernova reported revenues of $10.96 billion, up 3.8% year on year. This print topped analysts’ expectations by 6.5%. It was a strong quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

The stock is up 26% since reporting and currently trades at $873.

Read our full, actionable report on GE Vernova here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.