Let’s dig into the relative performance of Mettler-Toledo (NYSE: MTD) and its peers as we unravel the now-completed Q4 research tools & consumables earnings season.

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

The 10 research tools & consumables stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 23.5% since the latest earnings results.

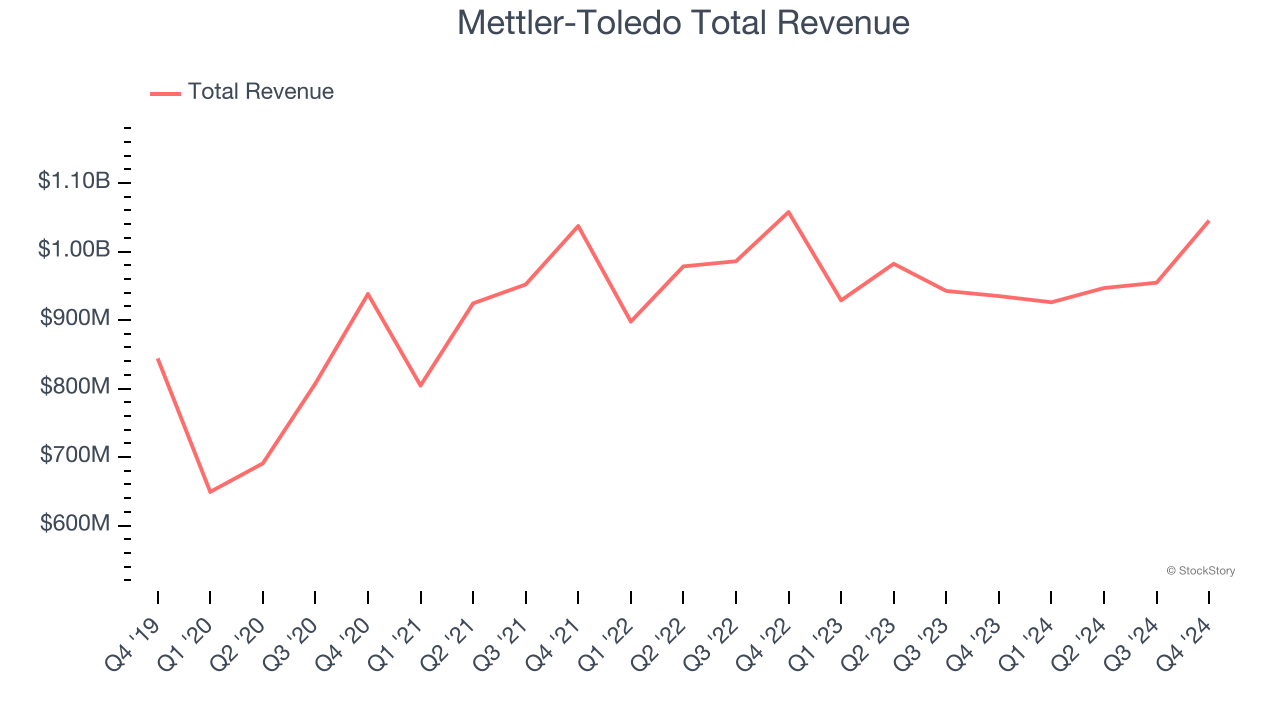

Mettler-Toledo (NYSE: MTD)

With roots dating back to the precision balance innovations of Swiss engineer Erhard Mettler, Mettler-Toledo (NYSE: MTD) manufactures precision weighing instruments, analytical equipment, and product inspection systems used in laboratories, industrial settings, and food retail.

Mettler-Toledo reported revenues of $1.05 billion, up 11.8% year on year. This print exceeded analysts’ expectations by 3.6%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ organic revenue estimates and a narrow beat of analysts’ full-year EPS guidance estimates.

Patrick Kaltenbach, President and Chief Executive Officer, stated, “We had a strong finish to the year as we capitalized on very good customer demand for Laboratory products, especially in Europe. Strong sales growth and solid execution of our margin improvement initiatives contributed to excellent Adjusted EPS and cash flow.”

The stock is down 22.2% since reporting and currently trades at $1,053.

Is now the time to buy Mettler-Toledo? Access our full analysis of the earnings results here, it’s free.

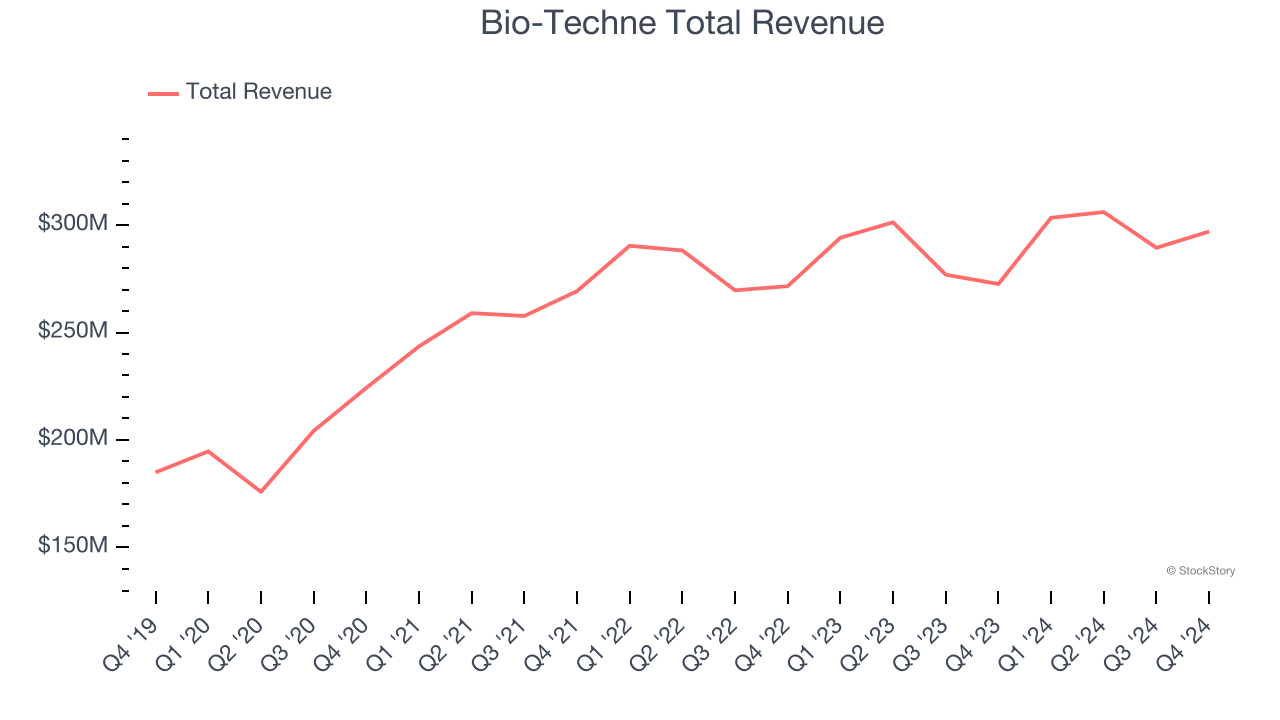

Best Q4: Bio-Techne (NASDAQ: TECH)

With a catalog of hundreds of thousands of specialized biological products used in laboratories worldwide, Bio-Techne (NASDAQ: TECH) develops and manufactures specialized reagents, instruments, and services that help researchers study biological processes and enable diagnostic testing and cell therapy development.

Bio-Techne reported revenues of $297 million, up 9% year on year, outperforming analysts’ expectations by 4.2%. The business had an exceptional quarter with a solid beat of analysts’ organic revenue estimates and a decent beat of analysts’ EPS estimates.

Bio-Techne scored the biggest analyst estimates beat among its peers. The stock is down 26.3% since reporting. It currently trades at $53.50.

Is now the time to buy Bio-Techne? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Avantor (NYSE: AVTR)

With roots dating back to 1904 and embedded in virtually every stage of scientific research and production, Avantor (NYSE: AVTR) provides mission-critical products, materials, and services to customers in biopharma, healthcare, education, and advanced technology industries.

Avantor reported revenues of $1.69 billion, down 2.1% year on year, falling short of analysts’ expectations by 1.6%. It was a softer quarter as it posted a miss of analysts’ organic revenue estimates.

Avantor delivered the weakest performance against analyst estimates in the group. The stock is down 29.7% since the results and currently trades at $15.23.

Read our full analysis of Avantor’s results here.

Thermo Fisher (NYSE: TMO)

With over 14,000 sales personnel and a portfolio spanning more than 2,500 technology manufacturers, Thermo Fisher Scientific (NYSE: TMO) provides scientific equipment, reagents, consumables, software, and laboratory services to pharmaceutical, biotech, academic, and healthcare customers worldwide.

Thermo Fisher reported revenues of $11.4 billion, up 4.7% year on year. This result topped analysts’ expectations by 1%. Aside from that, it was a mixed quarter as it also logged an impressive beat of analysts’ organic revenue estimates but a significant miss of analysts’ operating income estimates.

The stock is down 21.6% since reporting and currently trades at $445.49.

Read our full, actionable report on Thermo Fisher here, it’s free.

Bruker (NASDAQ: BRKR)

With roots dating back to the pioneering days of nuclear magnetic resonance technology, Bruker (NASDAQ: BRKR) develops and manufactures high-performance scientific instruments that enable researchers and industrial analysts to explore materials at microscopic, molecular, and cellular levels.

Bruker reported revenues of $979.6 million, up 14.6% year on year. This print beat analysts’ expectations by 1.4%. More broadly, it was a mixed quarter as it also produced a solid beat of analysts’ organic revenue estimates but full-year revenue guidance missing analysts’ expectations.

Bruker delivered the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is down 22.8% since reporting and currently trades at $39.89.

Read our full, actionable report on Bruker here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.