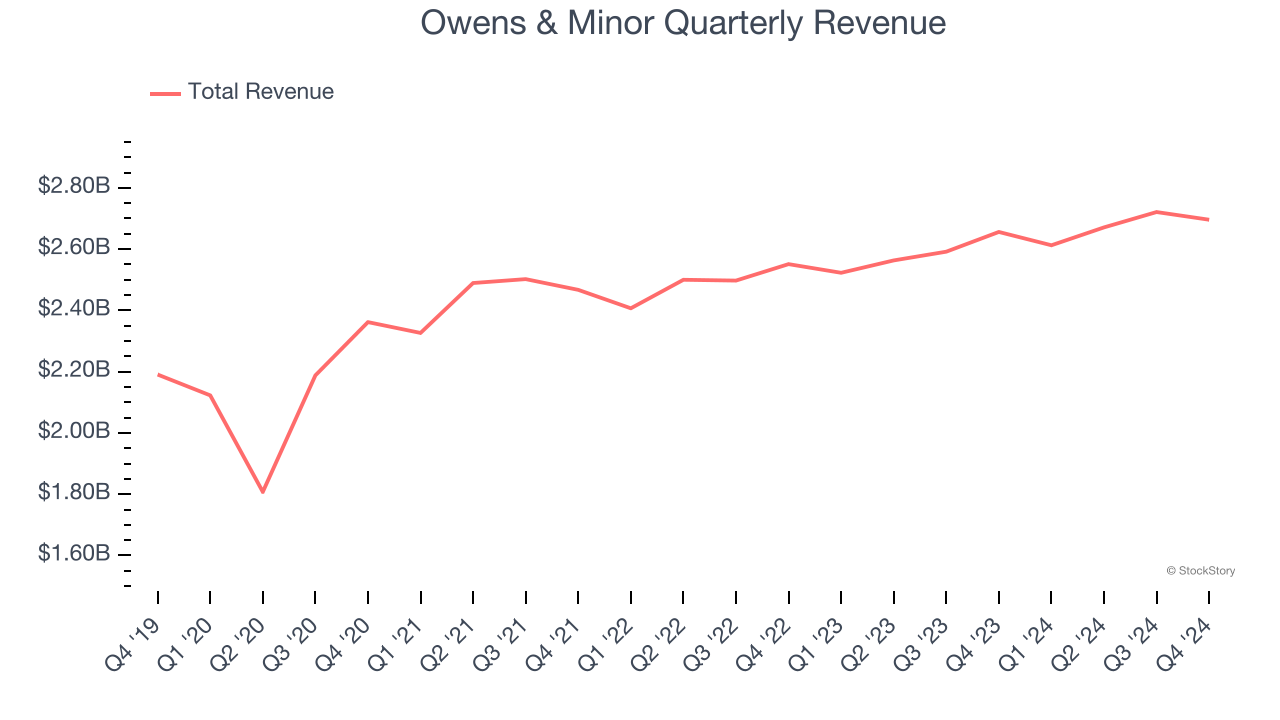

Medical supply and logistics company Owens & Minor (NYSE: OMI) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 1.5% year on year to $2.70 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $11 billion at the midpoint. Its non-GAAP profit of $0.55 per share was 5.7% above analysts’ consensus estimates.

Is now the time to buy Owens & Minor? Find out by accessing our full research report, it’s free.

Owens & Minor (OMI) Q4 CY2024 Highlights:

- Revenue: $2.70 billion vs analyst estimates of $2.69 billion (1.5% year-on-year growth, in line)

- Adjusted EPS: $0.55 vs analyst estimates of $0.52 (5.7% beat)

- Adjusted EBITDA: $138.2 million vs analyst estimates of $134.9 million (5.1% margin, 2.4% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $11 billion at the midpoint, in line with analyst expectations and implying 2.8% growth (vs 3.6% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $1.73 at the midpoint, missing analyst estimates by 3.6%

- EBITDA guidance for the upcoming financial year 2025 is $575 million at the midpoint, below analyst estimates of $595.6 million

- Operating Margin: -9.7%, down from 2.3% in the same quarter last year

- Free Cash Flow was -$435,000, down from $55.44 million in the same quarter last year

- Market Capitalization: $531.3 million

Company Overview

Founded in 1882, Owens & Minor (NYSE: OMI) offers healthcare logistics and medical supply solutions, specializing in product distribution, logistics management, and manufacturing of medical-grade PPE and surgical supplies.

Healthcare Distribution & Related Services

Healthcare distributors operate scale-driven business models that thrive on high volumes. Their recurring revenue streams from contracts with hospitals, pharmacies, and healthcare providers provide stability, but profitability can be squeezed by powerful stakeholders on both sides (suppliers and customers), pricing pressures, and regulatory changes. Looking ahead, the sector is positioned for growth due to increasing demand for healthcare services driven by an aging population and advancements in medical technology. However, rising operational costs, potential drug pricing reforms, and supply chain vulnerabilities present potential headwinds. Additionally, the push for digitalization and value-based care creates opportunities for innovation but requires significant investment to remain competitive.

Sales Growth

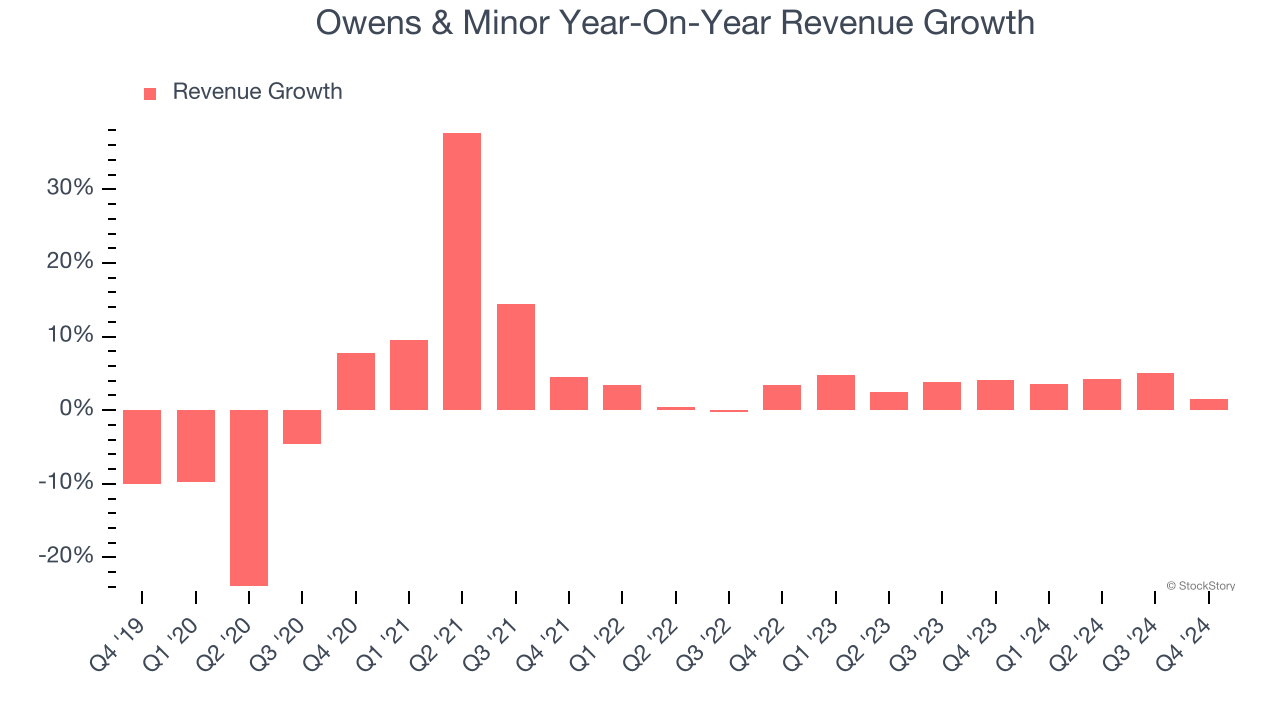

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Unfortunately, Owens & Minor’s 3% annualized revenue growth over the last five years was tepid. This was below our standard for the healthcare sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Owens & Minor’s annualized revenue growth of 3.7% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Owens & Minor grew its revenue by 1.5% year on year, and its $2.70 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.7% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

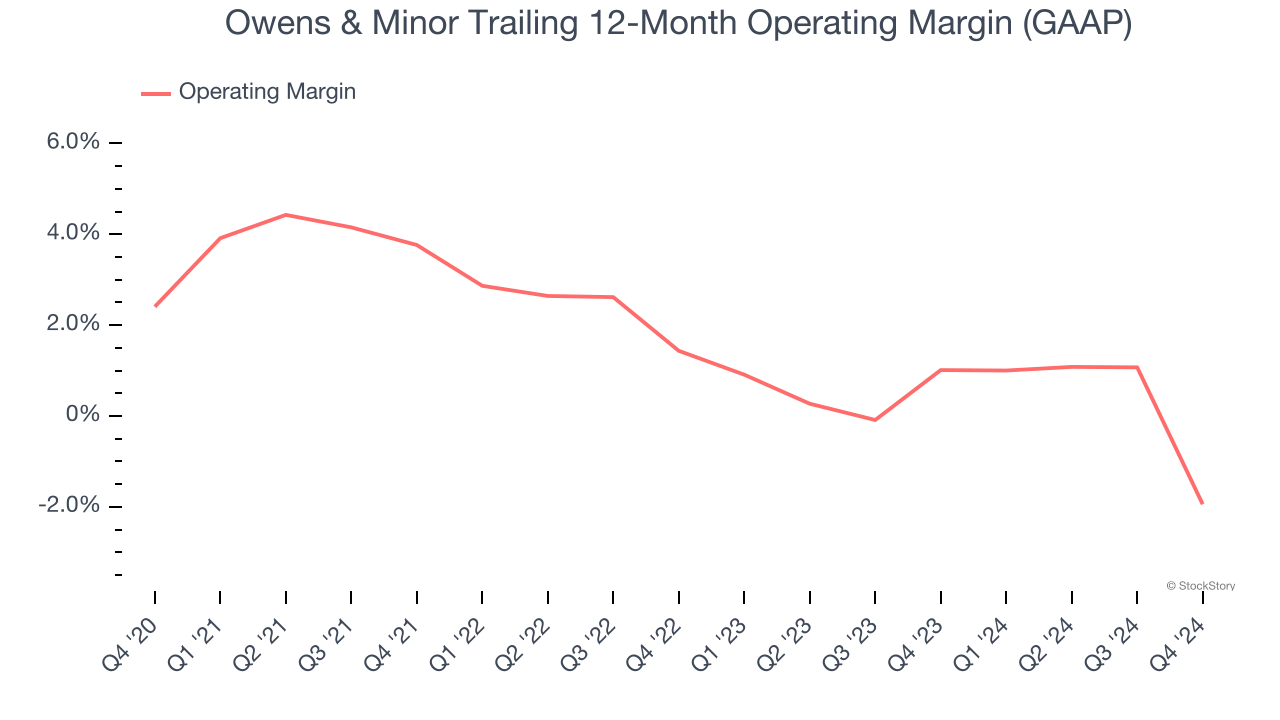

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Owens & Minor was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.2% was weak for a healthcare business.

Analyzing the trend in its profitability, Owens & Minor’s operating margin decreased by 4.3 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.4 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Owens & Minor generated an operating profit margin of negative 9.7%, down 12 percentage points year on year. This contraction shows it was recently less efficient because its expenses grew faster than its revenue.

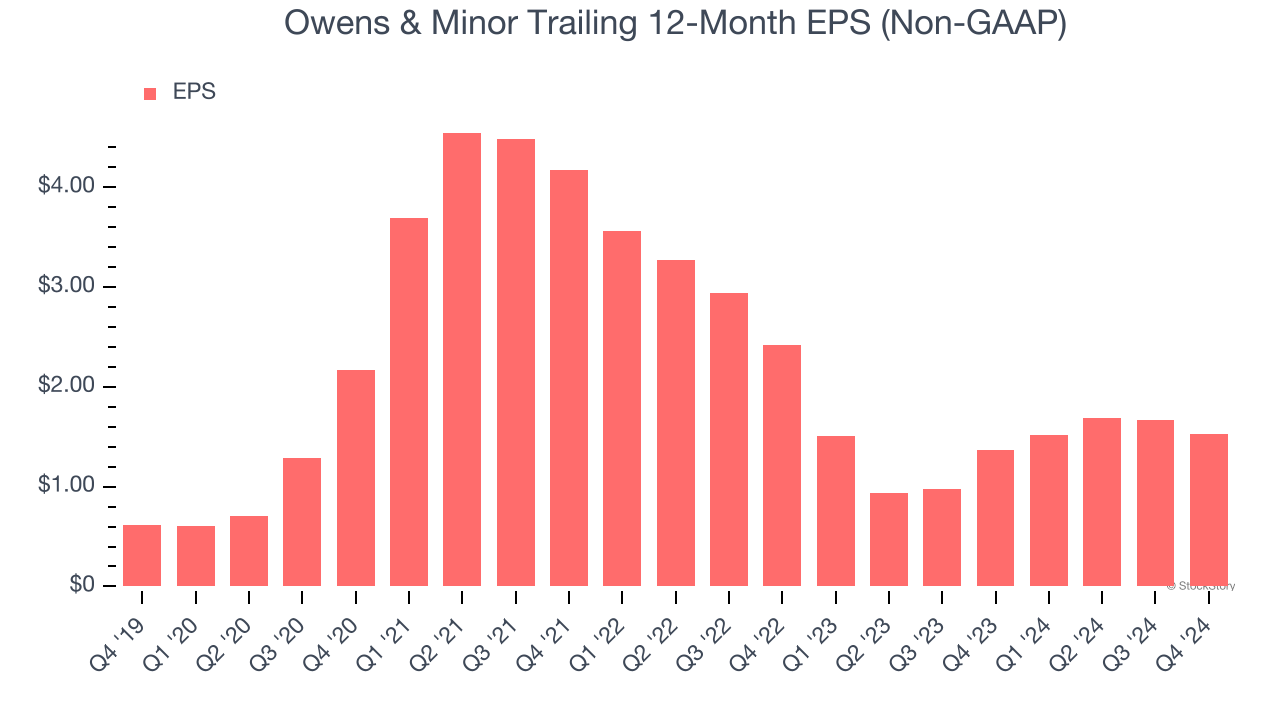

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Owens & Minor’s EPS grew at an astounding 20% compounded annual growth rate over the last five years, higher than its 3% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Owens & Minor reported EPS at $0.55, down from $0.69 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 5.7%. Over the next 12 months, Wall Street expects Owens & Minor’s full-year EPS of $1.52 to grow 16.1%.

Key Takeaways from Owens & Minor’s Q4 Results

It was encouraging to see Owens & Minor beat analysts’ EBITDA and EPS expectations this quarter despite in-line revenue. Full-year revenue guidance was also in line, which is comforting. On the other hand, its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock traded up 1.6% to $7.01 immediately following the results.

Is Owens & Minor an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.