Since January 2020, the S&P 500 has delivered a total return of 82%. But one standout stock has more than doubled the market - over the past five years, Parker-Hannifin has surged 207% to $635 per share. Its momentum hasn’t stopped as it’s also gained 24.8% in the last six months, beating the S&P by 18.5%.

Is now still a good time to buy PH? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does PH Stock Spark Debate?

Founded in 1917, Parker Hannifin (NYSE: PH) is a manufacturer of motion and control systems for a wide variety of mobile, industrial and aerospace markets.

Two Positive Attributes:

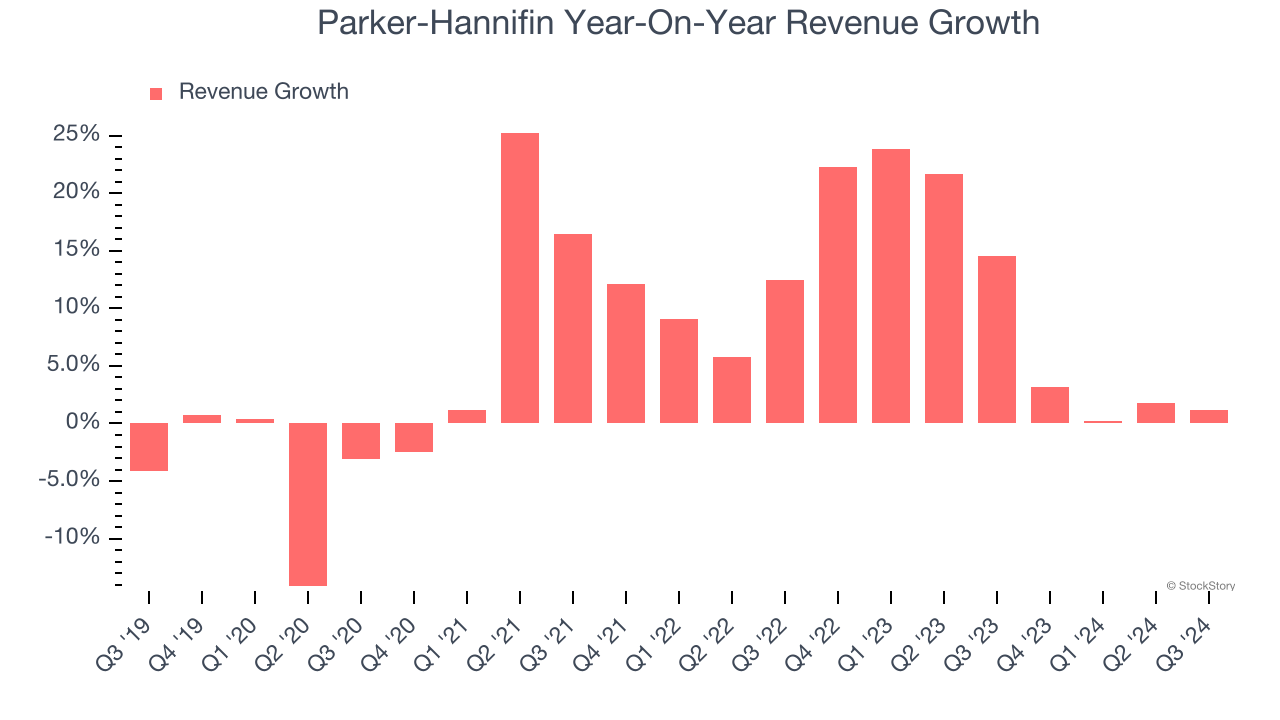

1. Skyrocketing Revenue Shows Strong Momentum

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Parker-Hannifin’s annualized revenue growth of 10.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

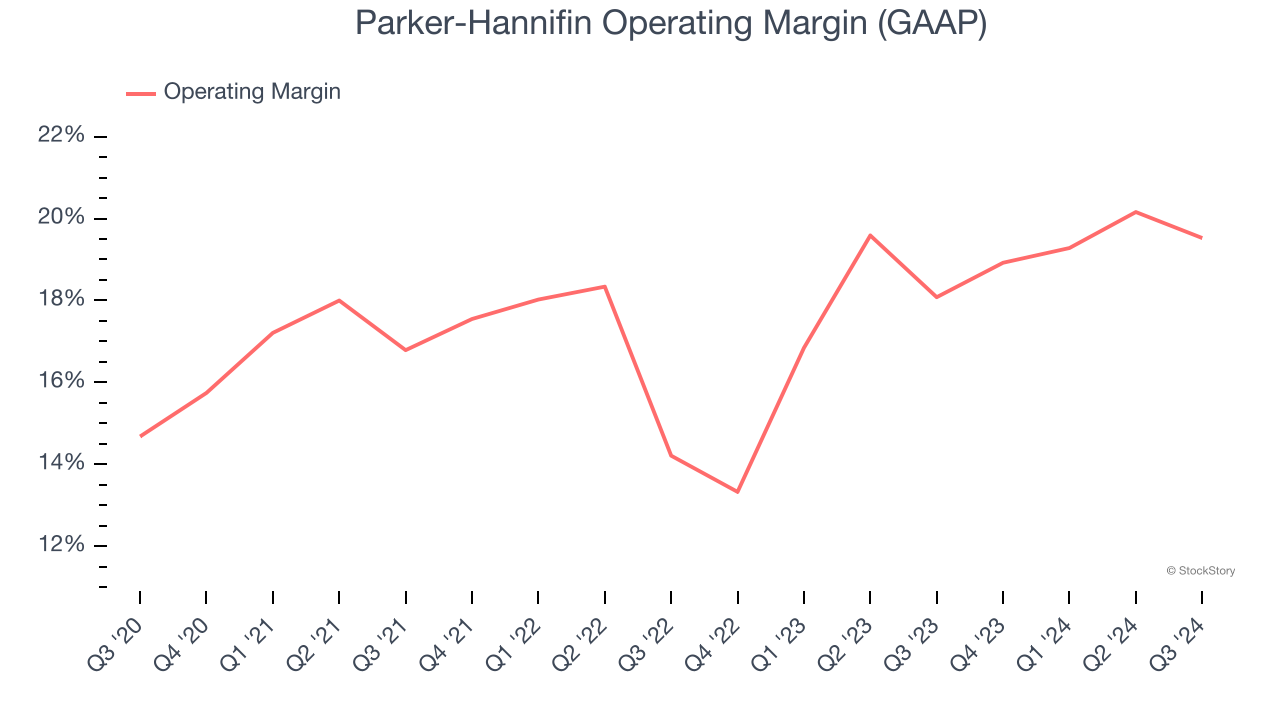

2. Operating Margin Rising, Profits Up

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Analyzing the trend in its profitability, Parker-Hannifin’s operating margin rose by 6.5 percentage points over the last five years, showing its efficiency has meaningfully improved. . Its operating margin for the trailing 12 months was 19.5%.

One Reason to be Careful:

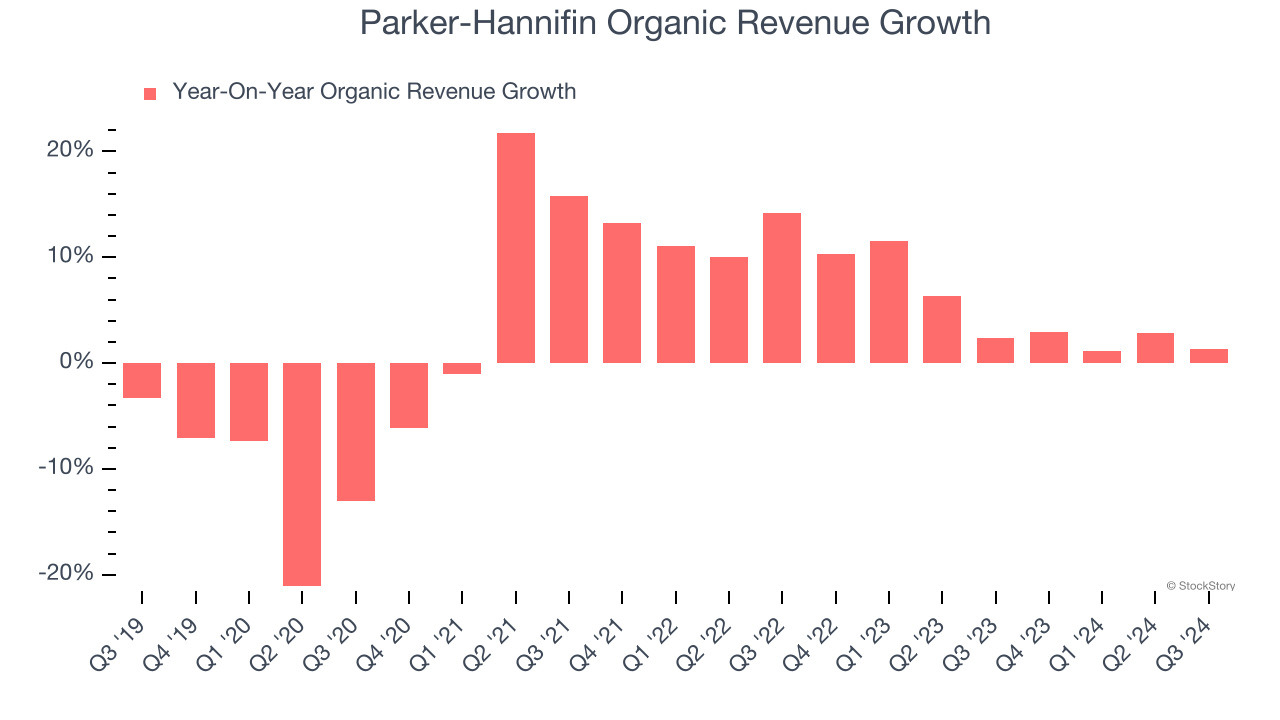

Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Gas and Liquid Handling companies should track organic revenue in addition to reported revenue. This metric gives visibility into Parker-Hannifin’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Parker-Hannifin’s organic revenue averaged 4.8% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

Parker-Hannifin’s merits more than compensate for its flaws, and with its shares outperforming the market lately, the stock trades at 23.1× forward price-to-earnings (or $635 per share). Is now the right time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Parker-Hannifin

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.