Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Hilton (NYSE: HLT) and the best and worst performers in the travel and vacation providers industry.

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

The 17 travel and vacation providers stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 0.9% below.

Luckily, travel and vacation providers stocks have performed well with share prices up 11.7% on average since the latest earnings results.

Hilton (NYSE: HLT)

Founded in 1919, Hilton Worldwide (NYSE: HLT) is a global hospitality company with a portfolio of hotel brands.

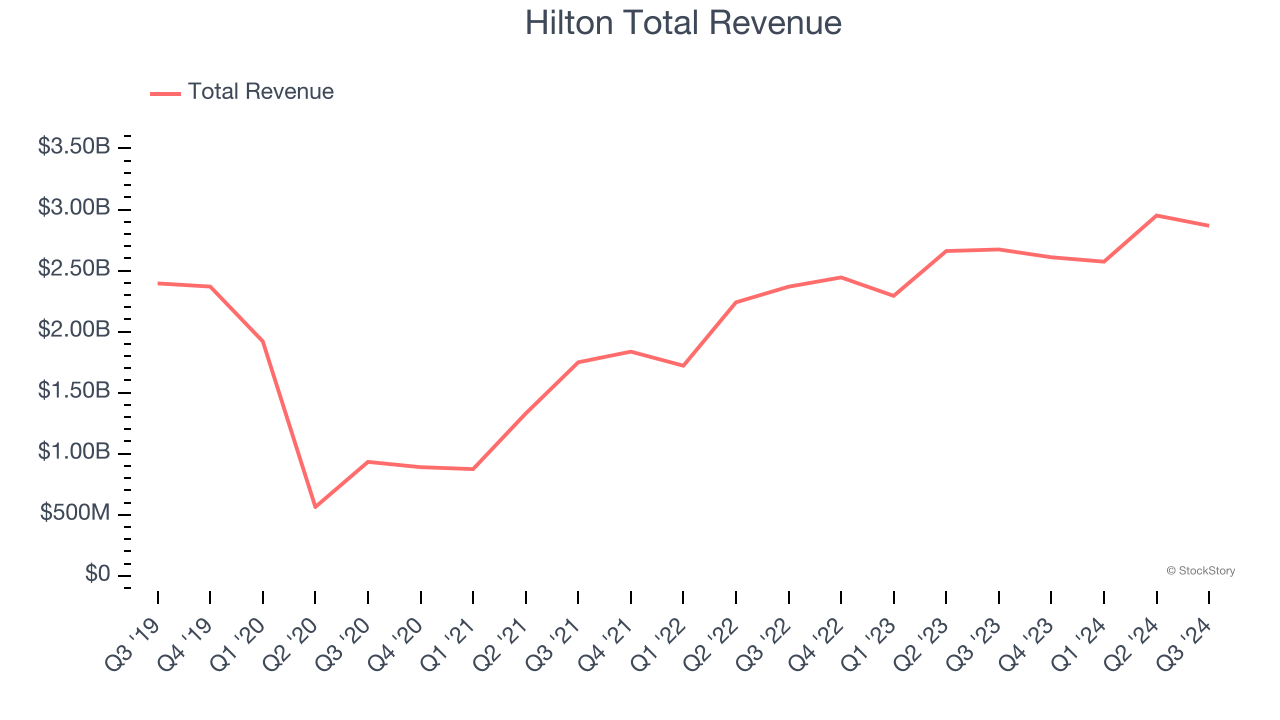

Hilton reported revenues of $2.87 billion, up 7.3% year on year. This print fell short of analysts’ expectations by 1.3%. Overall, it was a mixed quarter for the company with a decent beat of analysts’ adjusted operating income estimates.

Christopher J. Nassetta, President & Chief Executive Officer of Hilton, said, "We were pleased to deliver continued strong bottom line results that exceeded our guidance, despite slower top line growth which was driven by modestly slower macro trends, weather impacts and unfavorable calendar shifts. We continued to demonstrate the strength of our model, opening more rooms than any other quarter in our history, surpassing 8,000 hotels and achieving net unit growth of 7.8 percent. "

Interestingly, the stock is up 3.6% since reporting and currently trades at $246.52.

Read our full report on Hilton here, it’s free.

Best Q3: Target Hospitality (NASDAQ: TH)

Building mini-communities at places such as oil drilling sites, Target Hospitality (NASDAQ: TH) is a provider of specialty workforce lodging accommodations and services.

Target Hospitality reported revenues of $95.19 million, down 34.8% year on year, outperforming analysts’ expectations by 8.3%. The business had a very strong quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

Target Hospitality achieved the biggest analyst estimates beat and highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 5.4% since reporting. It currently trades at $9.70.

Is now the time to buy Target Hospitality? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Sabre (NASDAQ: SABR)

Originally a division of American Airlines, Sabre (NASDAQ: SABR) is a technology provider for the global travel and tourism industry.

Sabre reported revenues of $764.7 million, up 3.3% year on year, falling short of analysts’ expectations by 1.4%. It was a slower quarter as it posted a significant miss of analysts’ EPS estimates and a miss of analysts’ airline bookings estimates.

As expected, the stock is down 13.8% since the results and currently trades at $3.55.

Read our full analysis of Sabre’s results here.

Choice Hotels (NYSE: CHH)

With almost 100% of its properties under franchise agreements, Choice Hotels (NYSE: CHH) is a hotel franchisor known for its diverse brand portfolio including Comfort Inn, Quality Inn, and Clarion.

Choice Hotels reported revenues of $428 million, flat year on year. This number lagged analysts' expectations by 0.9%. Taking a step back, it was still a strong quarter as it logged an impressive beat of analysts’ EPS estimates and a decent beat of analysts’ adjusted operating income estimates.

The stock is up 3.3% since reporting and currently trades at $143.30.

Read our full, actionable report on Choice Hotels here, it’s free.

Playa Hotels & Resorts (NASDAQ: PLYA)

Sporting a roster of beachfront properties, Playa Hotels & Resorts (NASDAQ: PLYA) is an owner, operator, and developer of all-inclusive resorts in prime vacation destinations.

Playa Hotels & Resorts reported revenues of $183.5 million, down 13.9% year on year. This print topped analysts’ expectations by 4.1%. It was a strong quarter as it also recorded a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

The stock is up 37.1% since reporting and currently trades at $12.35.

Read our full, actionable report on Playa Hotels & Resorts here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.