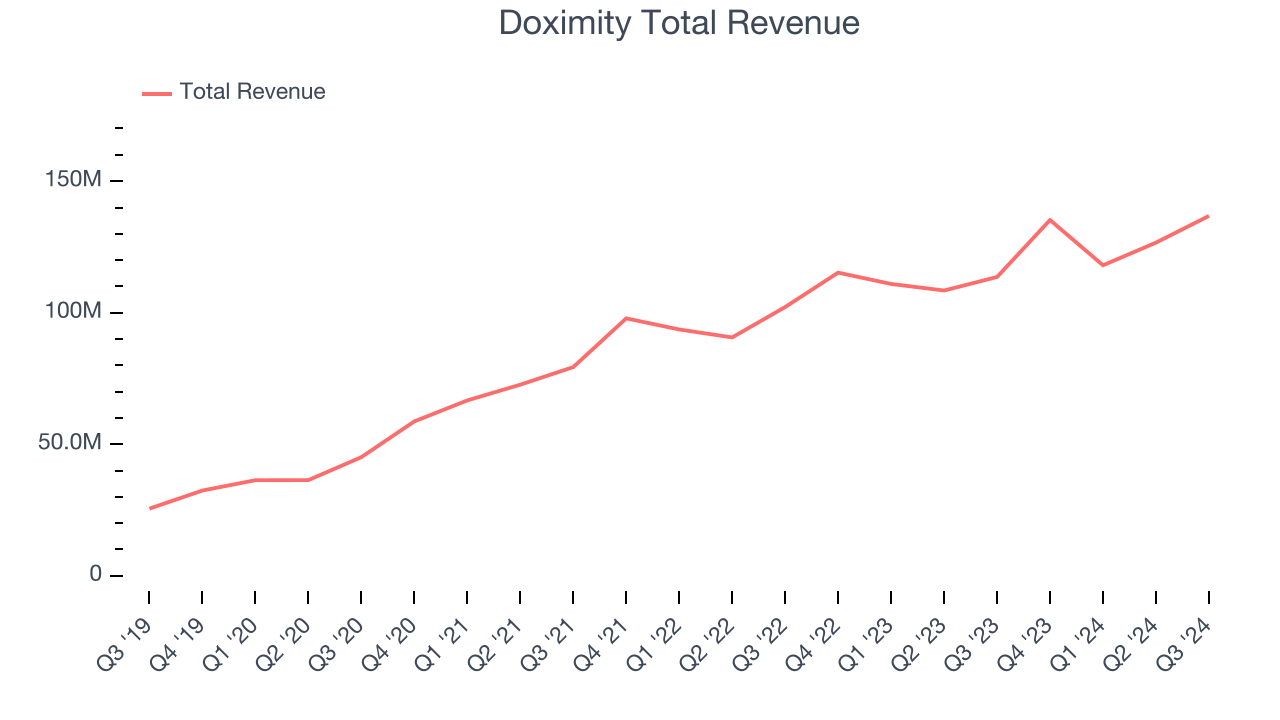

Healthcare professional network Doximity (NYSE: DOCS) reported revenue ahead of Wall Street’s expectations in Q3 CY2024, with sales up 20.4% year on year to $136.8 million. On top of that, next quarter’s revenue guidance ($152.5 million at the midpoint) was surprisingly good and 8.5% above what analysts were expecting. Its non-GAAP profit of $0.30 per share was also 17% above analysts’ consensus estimates.

Is now the time to buy Doximity? Find out by accessing our full research report, it’s free.

Doximity (DOCS) Q3 CY2024 Highlights:

- Revenue: $136.8 million vs analyst estimates of $127.2 million (7.6% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.26 (17% beat)

- EBITDA: $76.15 million vs analyst estimates of $63.04 million (20.8% beat)

- The company lifted its revenue guidance for the full year to $537.5 million at the midpoint from $518.5 million, a 3.7% increase

- EBITDA guidance for the full year is $276.5 million at the midpoint, above analyst estimates of $255.5 million

- Gross Margin (GAAP): 90%, up from 88.8% in the same quarter last year

- Operating Margin: 38.8%, up from 29.7% in the same quarter last year

- EBITDA Margin: 55.7%, up from 47.7% in the same quarter last year

- Free Cash Flow Margin: 48.8%, up from 31.2% in the previous quarter

- Market Capitalization: $7.86 billion

“Our clinical workflow tools saw record use in Q2 with over 600,000 unique active prescribers,” said Jeff Tangney, co-founder and CEO of Doximity.

Company Overview

Founded in 2010 and named for a combination of “docs” and “proximity”, Doximity (NYSE: DOCS) is the leading social network for U.S. medical professionals.

Healthcare And Life Sciences Software

The coronavirus pandemic has underscored the importance of high-quality health infrastructure in times of crisis. Coupled with intense competition between drugmakers and the growing volume of data in the health care sector, demand for data management solutions in the healthcare space is expected to remain strong in the years ahead.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Luckily, Doximity’s sales grew at a decent 23% compounded annual growth rate over the last three years. This is a useful starting point for our analysis.

This quarter, Doximity reported robust year-on-year revenue growth of 20.4%, and its $136.8 million of revenue topped Wall Street estimates by 7.6%. Management is currently guiding for a 12.7% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and illustrates the market believes its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Doximity is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.6 months this quarter. The company’s efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving it the freedom to invest resources into new growth initiatives while maintaining optionality.

Key Takeaways from Doximity’s Q3 Results

We were impressed by Doximity’s optimistic EBITDA forecast for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a solid quarter. The stock traded up 33.6% to $58 immediately after reporting.

Indeed, Doximity had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.