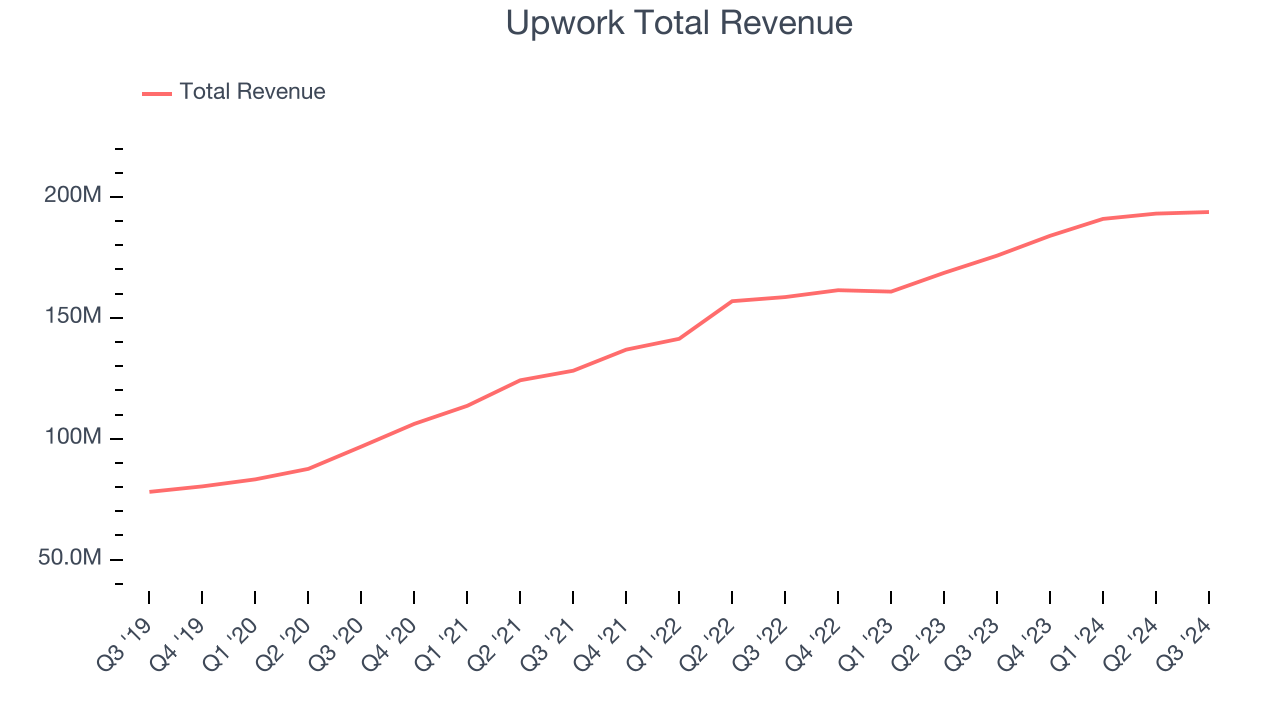

Online work marketplace Upwork (NASDAQ: UPWK) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 10.3% year on year to $193.8 million. Guidance for next quarter’s revenue was optimistic at $180.5 million at the midpoint, 2.7% above analysts’ estimates. Its non-GAAP profit of $0.29 per share was also 13.9% above analysts’ consensus estimates.

Is now the time to buy Upwork? Find out by accessing our full research report, it’s free.

Upwork (UPWK) Q3 CY2024 Highlights:

- Revenue: $193.8 million vs analyst estimates of $184 million (5.3% beat)

- Adjusted EPS: $0.29 vs analyst estimates of $0.25 (13.9% beat)

- EBITDA: $43.23 million vs analyst estimates of $38.53 million (12.2% beat)

- Revenue Guidance for Q4 CY2024 is $180.5 million at the midpoint, above analyst estimates of $175.8 million

- Management raised its full-year Adjusted EPS guidance to $1.01 at the midpoint, a 9.8% increase

- EBITDA guidance for the full year is $157 million at the midpoint, above analyst estimates of $146.3 million

- Gross Margin (GAAP): 77.6%, up from 75.4% in the same quarter last year

- Operating Margin: 10.7%, up from 6.5% in the same quarter last year

- EBITDA Margin: 22.3%, up from 17.8% in the same quarter last year

- Free Cash Flow Margin: 50.6%, up from 17.4% in the previous quarter

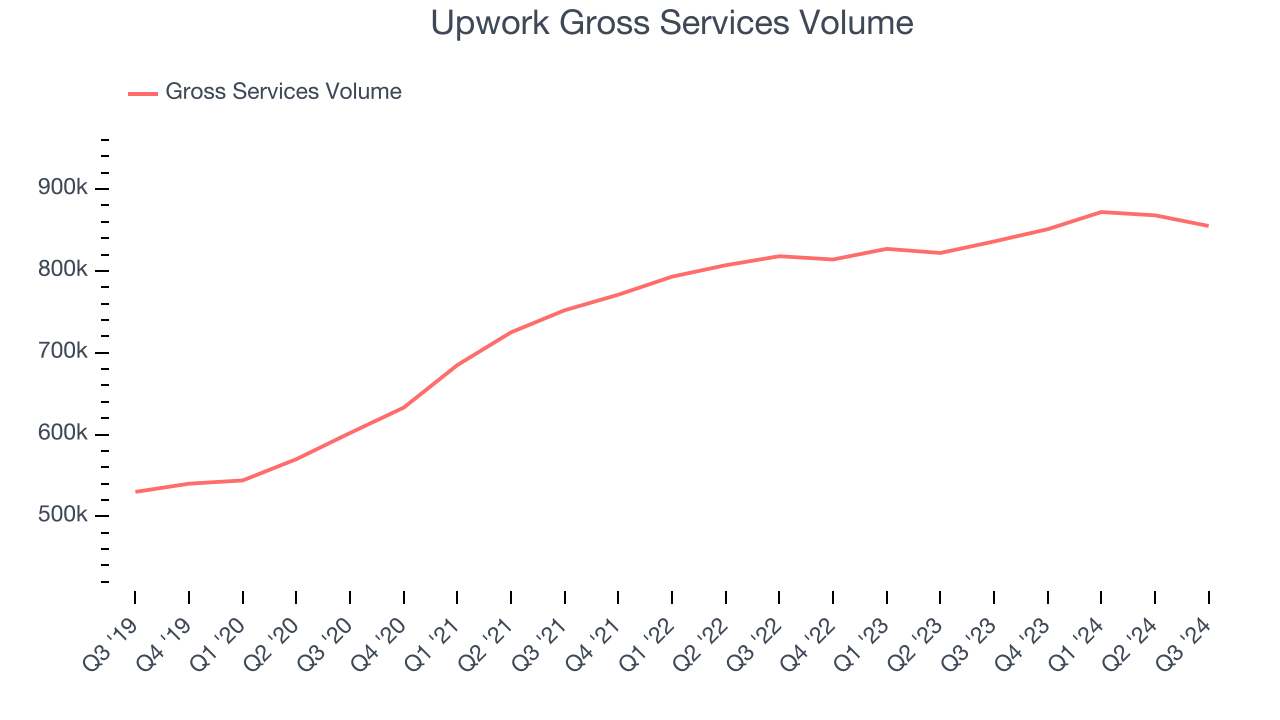

- Gross Services Volume: 855,000, up 19,000 year on year

- Market Capitalization: $1.9 billion

“Upwork continues to seize the tremendous market opportunity and execute our strategy to deliver durable, profitable growth, with 10% year-over-year revenue growth and our highest-ever net income in the third quarter,” said Hayden Brown, president and CEO, Upwork.

Company Overview

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ: UPWK) is an online platform where businesses and independent professionals connect to get work done.

Gig Economy

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech-enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Over the last three years, Upwork grew its sales at a solid 17.3% compounded annual growth rate. This is a good starting point for our analysis.

This quarter, Upwork reported year-on-year revenue growth of 10.3%, and its $193.8 million of revenue exceeded Wall Street’s estimates by 5.3%. Management is currently guiding for a 1.9% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and shows the market believes its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Gross Services Volume

Gmv Growth

As a gig economy marketplace, Upwork generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Upwork’s gross services volume, a key performance metric for the company, increased by 4% annually to 855,000 in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If Upwork wants to accelerate growth, it must engage users more effectively with its existing offerings or innovate with new products.

In Q3, Upwork added 19,000 gross services volume, leading to 2.3% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating gmv growth just yet.

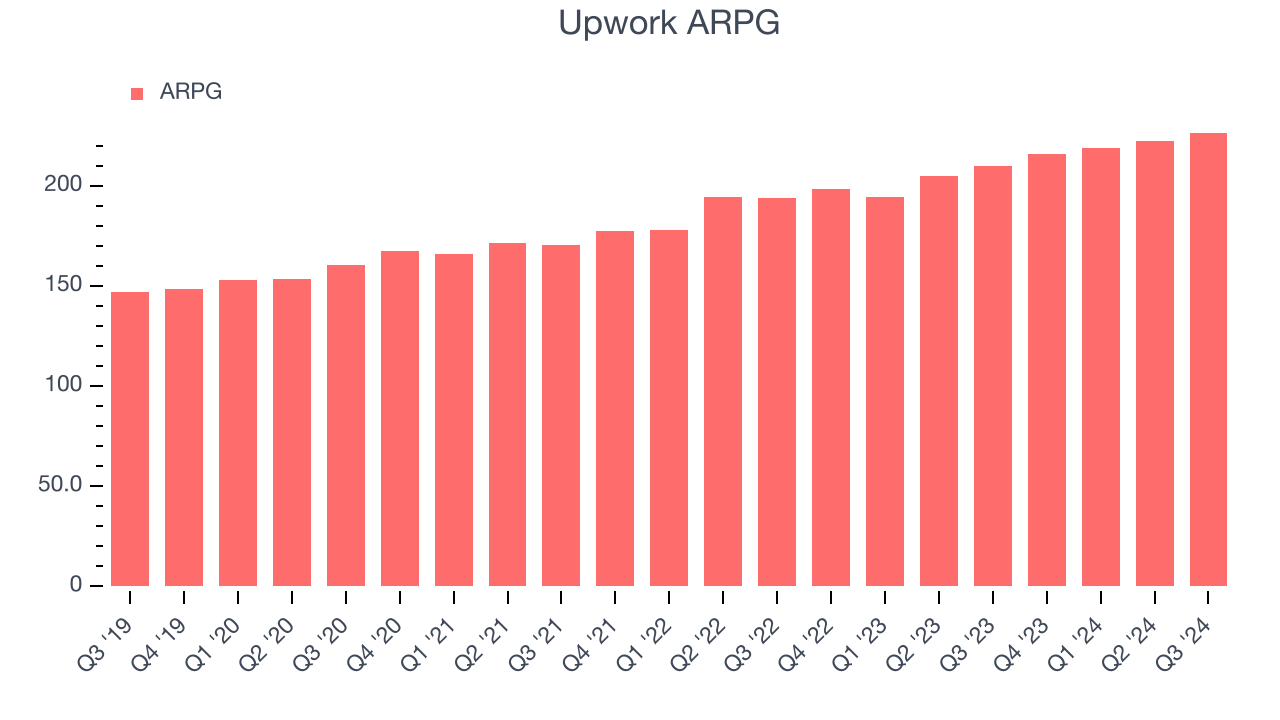

Revenue Per Gmv

Average revenue per gmv (ARPG) is a critical metric to track for consumer internet businesses like Upwork because it measures how much the company earns in transaction fees from each gmv. This number also informs us about Upwork’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Upwork’s ARPG growth has been excellent over the last two years, averaging 9.1%. Its ability to increase monetization while growing its gross services volume demonstrates its platform’s value, as its gmv are ing significantly more than last year.

This quarter, Upwork’s ARPG clocked in at $226.64. It grew 7.8% year on year, faster than its gross services volume.

Key Takeaways from Upwork’s Q3 Results

We were impressed by Upwork’s optimistic EBITDA forecast for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates. On the other hand, its gmv missed and its revenue growth stalled. Overall, we think this was still a decent quarter with some key metrics above expectations. The stock traded up 3.5% to $15.12 immediately following the results.

Upwork had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.