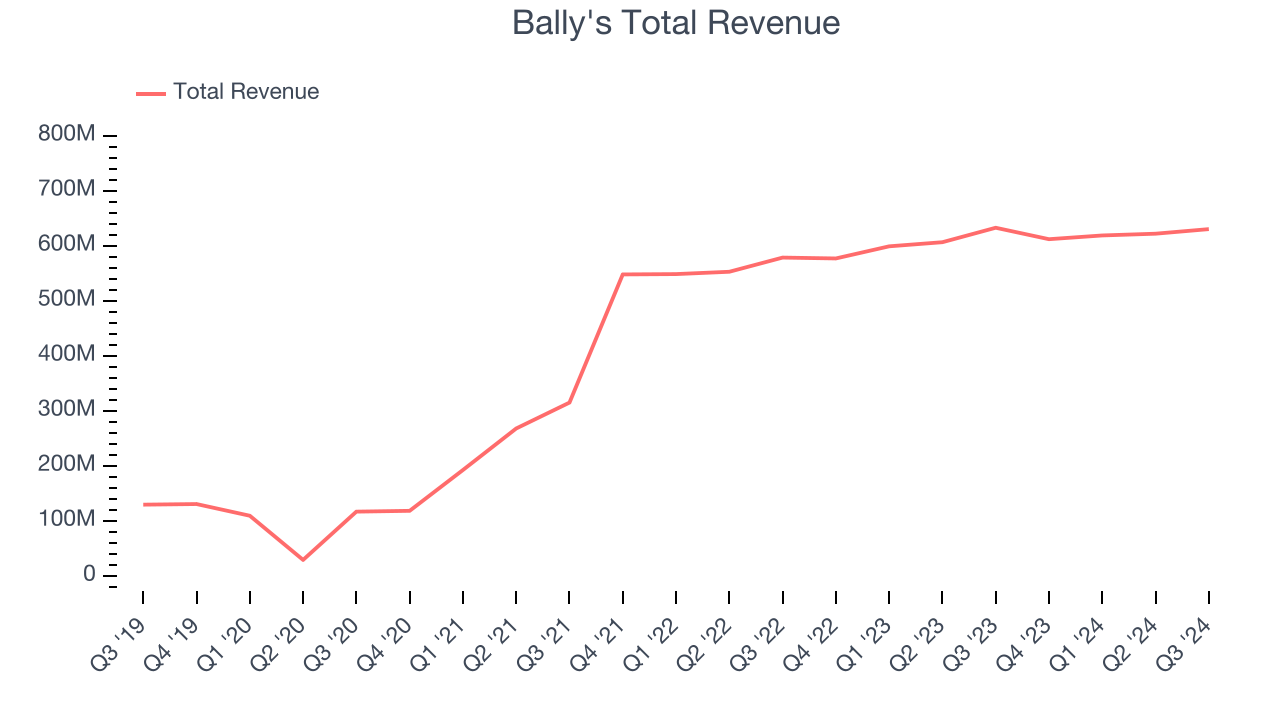

Gaming, betting and entertainment company Bally's Corporation (NYSE: BALY) fell short of the market’s revenue expectations in Q3 CY2024, with sales flat year on year at $630 million. Its GAAP loss of $5.10 per share was also 3,691% below analysts’ consensus estimates.

Is now the time to buy Bally's? Find out by accessing our full research report, it’s free.

Bally's (BALY) Q3 CY2024 Highlights:

- Revenue: $630 million vs analyst estimates of $655.1 million (3.8% miss)

- EPS: -$5.10 vs analyst estimates of -$0.13 (-$4.97 miss)

- EBITDA: $137.7 million vs analyst estimates of $149.4 million (7.8% miss)

- Gross Margin (GAAP): 54.6%, in line with the same quarter last year

- Operating Margin: -25%, down from 5.9% in the same quarter last year

- EBITDA Margin: 21.9%, in line with the same quarter last year

- Market Capitalization: $711.6 million

Company Overview

Headquartered in Providence, Rhode Island, Bally's Corporation (NYSE: BALY) is a diversified global casino-entertainment company that owns and manages casinos, resorts, and online gaming platforms.

Casino Operator

Casino operators enjoy limited competition because gambling is a highly regulated industry. These companies can also enjoy healthy margins and profits. Have you ever heard the phrase ‘the house always wins’? Regulation cuts both ways, however, and casinos may face stroke-of-the-pen risk that suddenly limits what they can or can't do and where they can do it. Furthermore, digitization is changing the game, pun intended. Whether it’s online poker or sports betting on your smartphone, innovation is forcing these players to adapt to changing consumer preferences, such as being able to wager anywhere on demand.

Sales Growth

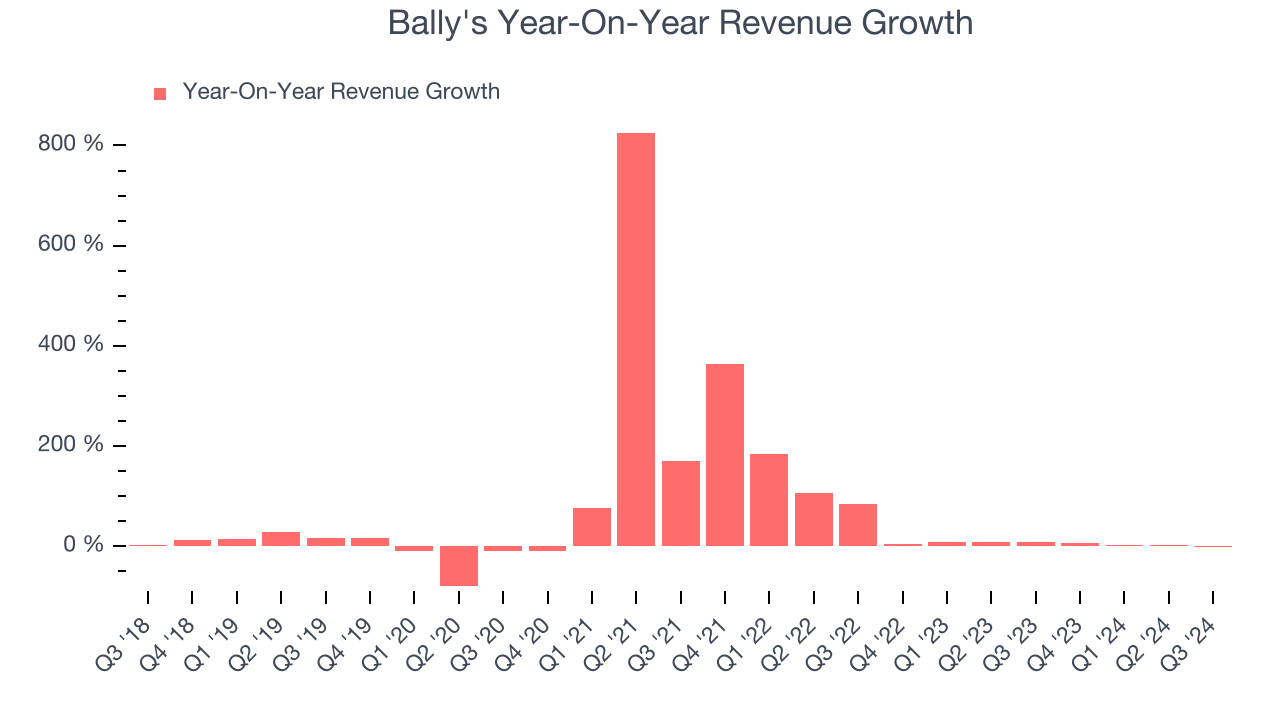

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Bally's grew its sales at an incredible 37.5% compounded annual growth rate. This is a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Bally’s recent history shows its demand slowed significantly as its annualized revenue growth of 5.6% over the last two years is well below its five-year trend. Note that COVID hurt Bally’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

Bally's also breaks out the revenue for its most important segment, Gaming. Over the last two years, Bally’s Gaming revenue (casino games, racing, sports betting) averaged 45.9% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Bally's missed Wall Street’s estimates and reported a rather uninspiring 0.4% year-on-year revenue decline, generating $630 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and illustrates the market thinks its newer products and services will not accelerate its top-line performance yet.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

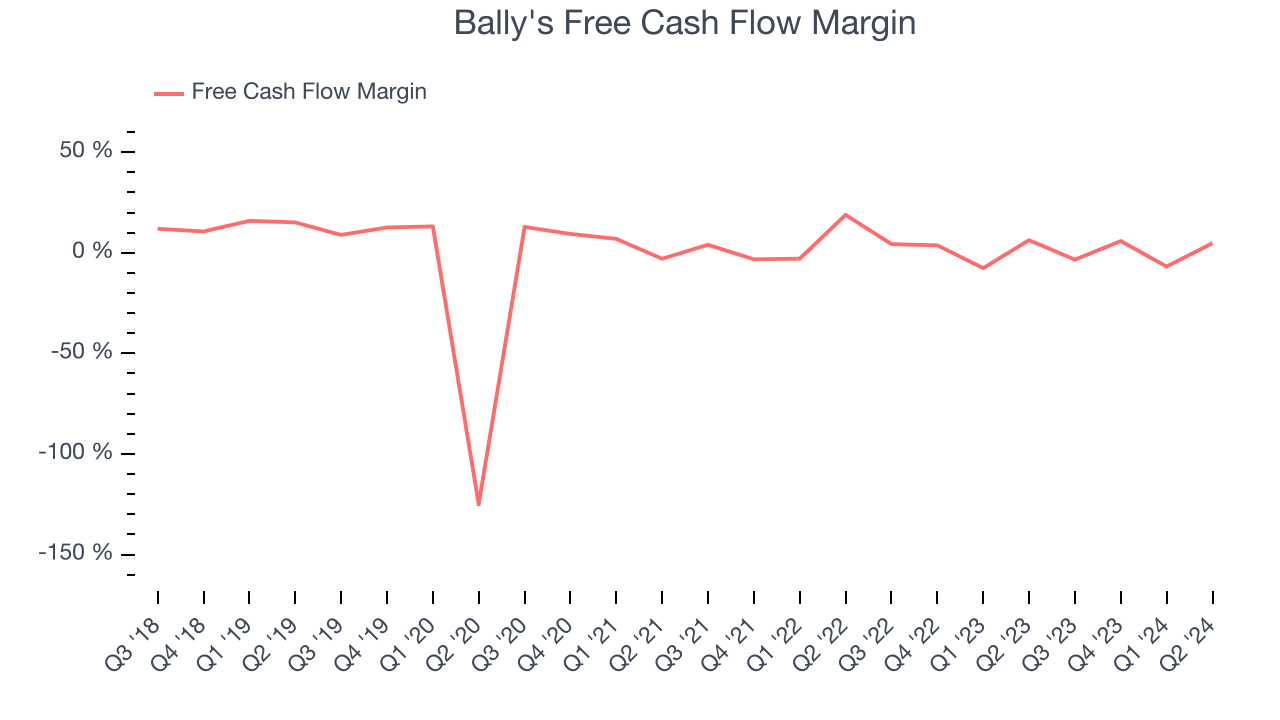

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Bally's broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

The company’s cash burn increased from $21.57 million of lost cash in the same quarter last year.

Key Takeaways from Bally’s Q3 Results

We struggled to find many strong positives in these results. Its EPS missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $17.62 immediately following the results.

Is Bally's an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.