Wrapping up Q3 earnings, we look at the numbers and key takeaways for the aerospace stocks, including Woodward (NASDAQ: WWD) and its peers.

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

The 13 aerospace stocks we track reported a mixed Q3. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 2% above.

Thankfully, share prices of the companies have been resilient as they are up 9.5% on average since the latest earnings results.

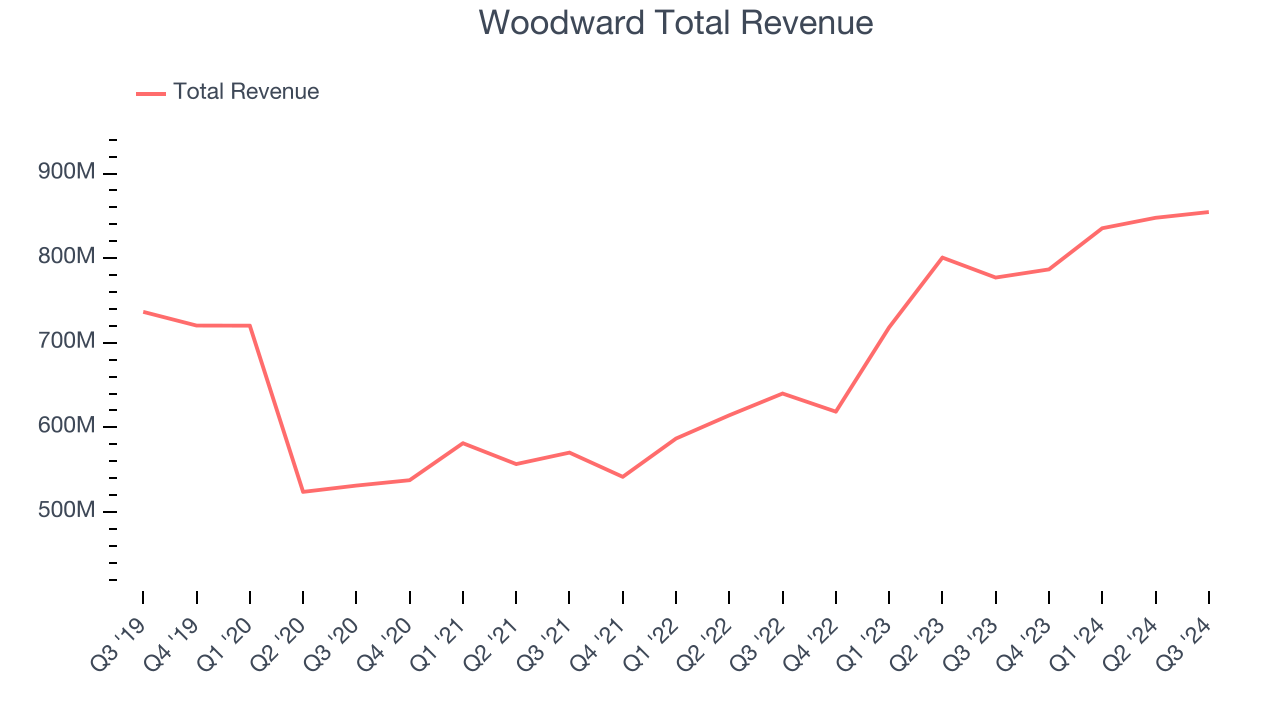

Woodward (NASDAQ: WWD)

Initially designing controls for water wheels in the early 1900s, Woodward (NASDAQ: WWD) designs, services, and manufactures energy control products and optimization solutions.

Woodward reported revenues of $854.5 million, up 10% year on year. This print exceeded analysts’ expectations by 5.3%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ organic revenue estimates and full-year EPS guidance exceeding analysts’ expectations.

"We delivered record sales in fiscal 2024 with Woodward revenue exceeding $3 billion for the first time. Robust end market demand along with contributions from operational excellence fueled significant sales growth and earnings expansion,” said Chip Blankenship, Chairman and Chief Executive Officer.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $179.97.

Is now the time to buy Woodward? Access our full analysis of the earnings results here, it’s free.

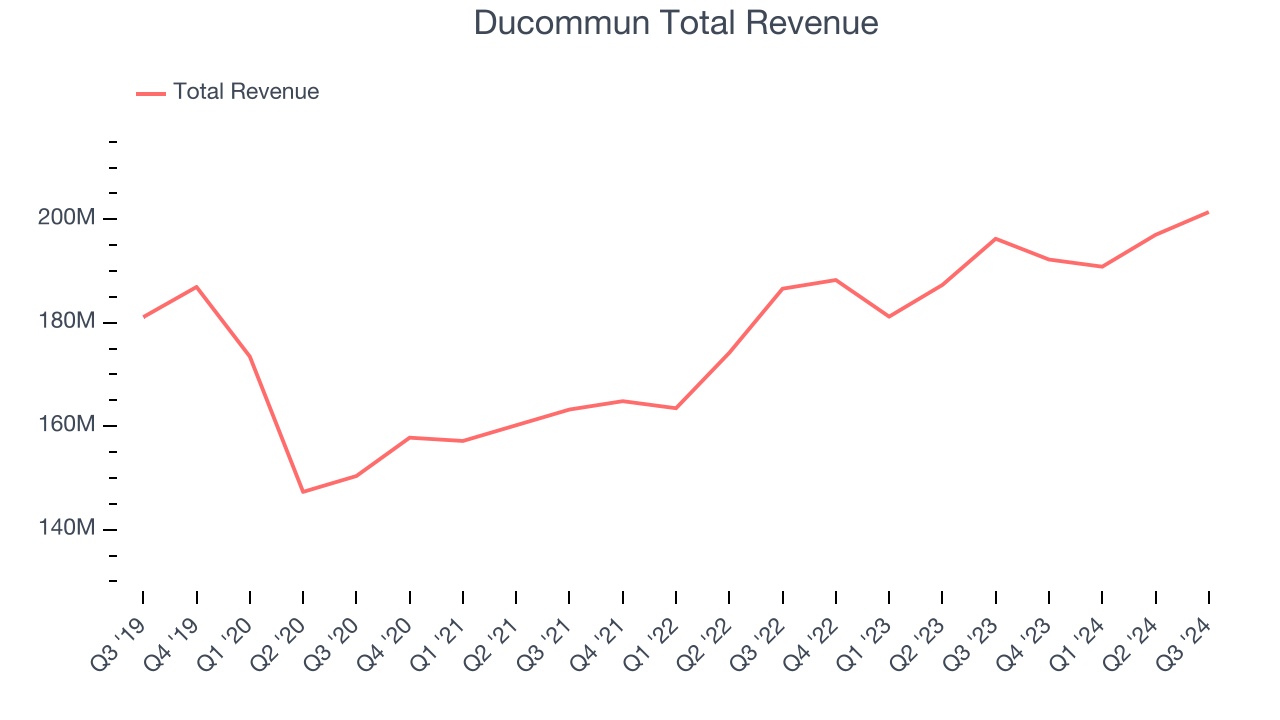

Best Q3: Ducommun (NYSE: DCO)

California’s oldest company, Ducommun (NYSE: DCO) is a provider of engineering and manufacturing services for high-performance products primarily within the aerospace and defense industries.

Ducommun reported revenues of $201.4 million, up 2.6% year on year, outperforming analysts’ expectations by 3.8%. The business had an incredible quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems content with the results as the stock is up 1% since reporting. It currently trades at $66.03.

Is now the time to buy Ducommun? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Textron (NYSE: TXT)

Listed on the NYSE in 1947, Textron (NYSE: TXT) provides products and services in the aerospace, defense, industrial, and finance sectors.

Textron reported revenues of $3.43 billion, up 2.5% year on year, falling short of analysts’ expectations by 2.7%. It was a disappointing quarter as it posted full-year EPS guidance missing analysts’ expectations.

As expected, the stock is down 2.6% since the results and currently trades at $84.61.

Read our full analysis of Textron’s results here.

Rocket Lab (NASDAQ: RKLB)

Becoming the first private company in the Southern Hemisphere to reach space, Rocket Lab (NASDAQ: RKLB) offers rockets designed for launching small satellites.

Rocket Lab reported revenues of $104.8 million, up 54.9% year on year. This print beat analysts’ expectations by 2.4%. It was a stunning quarter as it also recorded EBITDA guidance for next quarter exceeding analysts’ expectations.

Rocket Lab achieved the fastest revenue growth among its peers. The stock is up 77.3% since reporting and currently trades at $25.99.

Read our full, actionable report on Rocket Lab here, it’s free.

AerSale (NASDAQ: ASLE)

Providing a one-stop shop that integrates multiple services and product offerings, AerSale (NASDAQ: ASLE) delivers full-service support to mid-life commercial aircraft.

AerSale reported revenues of $82.68 million, down 10.6% year on year. This print lagged analysts' expectations by 11.1%. It was a softer quarter as it also recorded a significant miss of analysts’ adjusted operating income and EPS estimates.

AerSale had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is up 5.9% since reporting and currently trades at $6.25.

Read our full, actionable report on AerSale here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September, a quarter in November) have kept 2024 stock markets frothy, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there's still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.