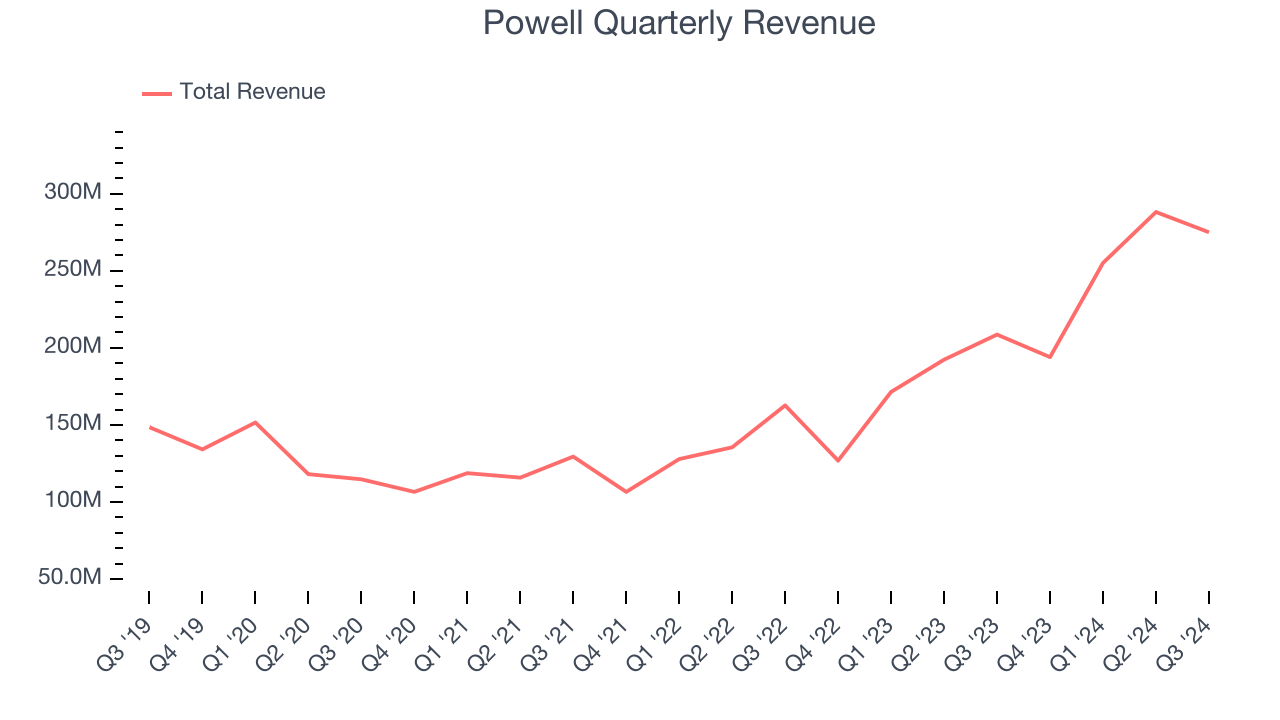

Electrical energy control systems manufacturer Powell (NYSE: POWL) missed Wall Street’s revenue expectations in Q3 CY2024, but sales rose 31.8% year on year to $275.1 million. Its GAAP profit of $3.77 per share was 6.2% above analysts’ consensus estimates.

Is now the time to buy Powell? Find out by accessing our full research report, it’s free.

Powell (POWL) Q3 CY2024 Highlights:

- Revenue: $275.1 million vs analyst estimates of $286.5 million (31.8% year-on-year growth, 4% miss)

- Adjusted EPS: $3.77 vs analyst estimates of $3.55 (6.2% beat)

- Adjusted EBITDA: $57.91 million vs analyst estimates of $54.87 million (21.1% margin, 5.5% beat)

- Operating Margin: 20.4%, up from 14.3% in the same quarter last year

- Backlog: $1.3 billion at quarter end

- Market Capitalization: $3.46 billion

Brett A. Cope, Powell’s Chairman and Chief Executive Officer, stated, “Powell delivered a strong fourth quarter performance that closed out another incredible year for the Company. We experienced tremendous growth in our largest markets, with our top line growing by 45% in fiscal 2024. We continue to execute at a high standard for both our customers and our shareholders as reflected by our gross margin, which improved 590 basis points compared to the prior year. Having recorded our second consecutive year of more than $1.0 billion in new orders, we continue to grow in our traditional markets of oil & gas, petrochemical and electrical utilities, while further diversifying in markets such as data centers, hydrogen, carbon capture and other alternative fuels. I’m incredibly proud of the Powell team for their performance in fiscal 2024 and their unwavering commitment to our customers and mission.”

Company Overview

Originally a metal-working shop supporting local petrochemical facilities, Powell (NYSE: POWL) has grown from a small Houston manufacturer to a global provider of electrical systems.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Luckily, Powell’s sales grew at an exceptional 14.4% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

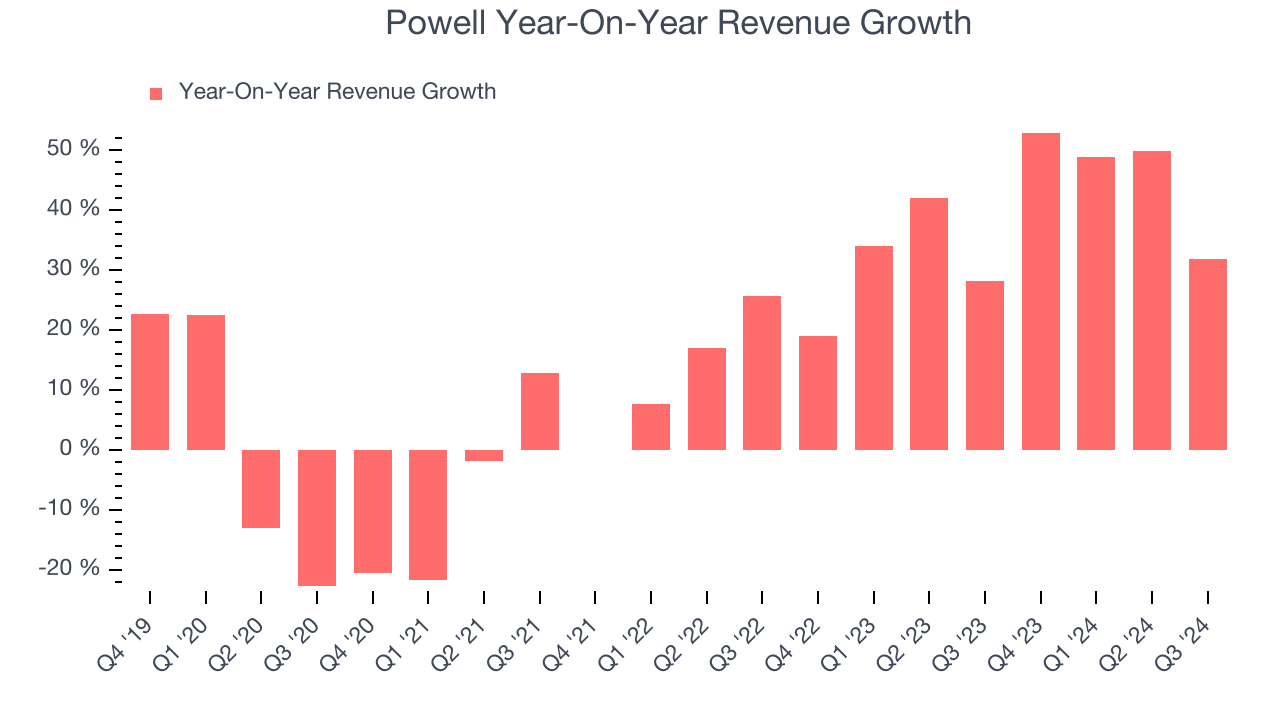

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Powell’s annualized revenue growth of 37.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Powell pulled off a wonderful 31.8% year-on-year revenue growth rate, but its $275.1 million of revenue fell short of Wall Street’s rosy estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.2% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

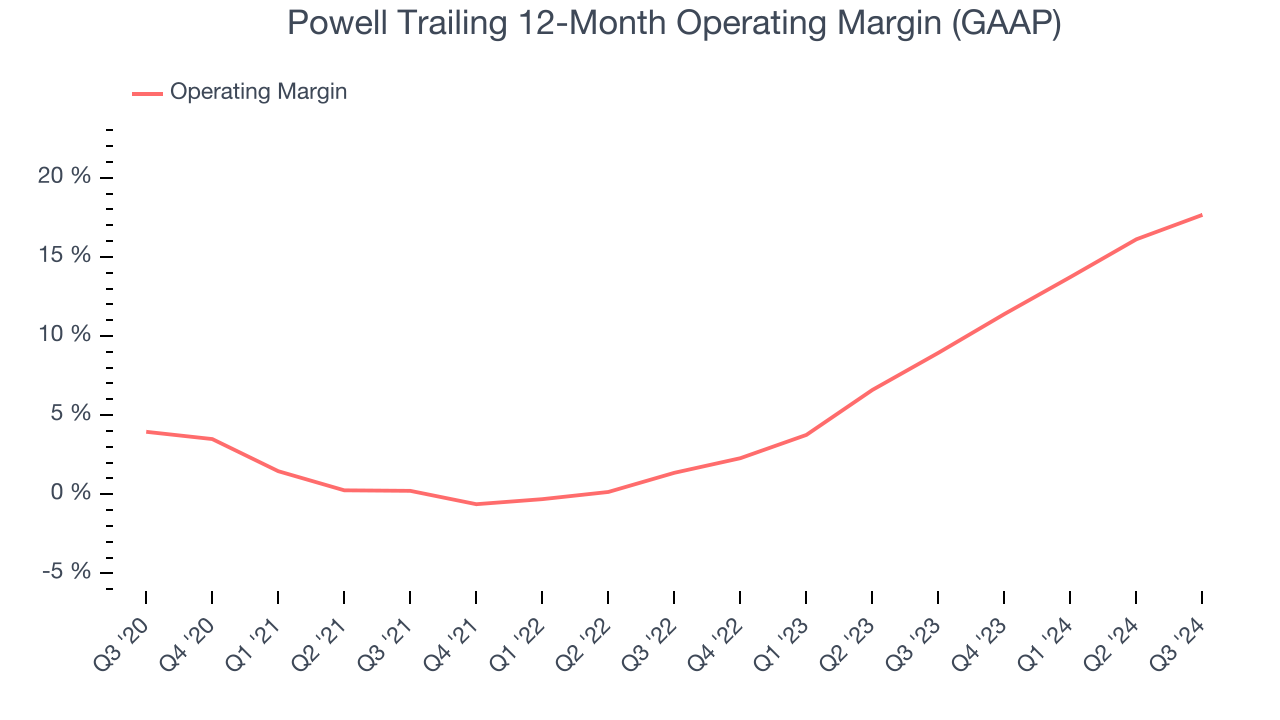

Powell has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.4%, higher than the broader industrials sector.

Looking at the trend in its profitability, Powell’s annual operating margin rose by 13.7 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q3, Powell generated an operating profit margin of 20.4%, up 6.1 percentage points year on year. The increase was solid, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

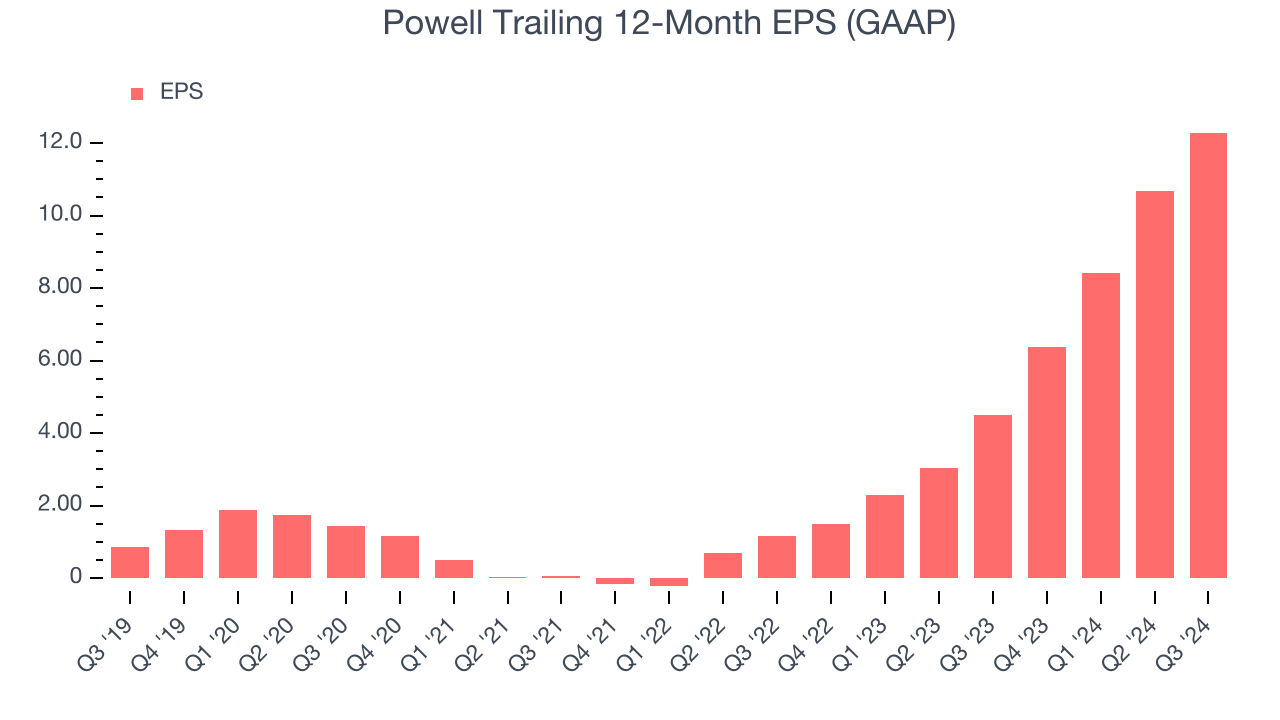

Powell’s EPS grew at an astounding 70.6% compounded annual growth rate over the last five years, higher than its 14.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into Powell’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Powell’s operating margin expanded by 13.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Powell, its two-year annual EPS growth of 227% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.In Q3, Powell reported EPS at $3.77, up from $2.17 in the same quarter last year. This print beat analysts’ estimates by 6.2%. Over the next 12 months, Wall Street expects Powell’s full-year EPS of $12.29 to grow by 1.3%.

Key Takeaways from Powell’s Q3 Results

We enjoyed seeing Powell exceed analysts’ EBITDA expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed significantly. Overall, this was a softer quarter. The stock traded down 7.5% to $289 immediately after reporting.

Is Powell an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.