Shares of AeroVironment (AVAV) tumbled 17.4% after a report by SpaceNews indicated that the company’s roughly $1.4 billion contract related to the U.S. Space Force could be reopened for competitive bidding. The development introduces uncertainty around what had been considered a significant long-term revenue driver.

What’s Behind the Drop in AVAV Stock?

The primary issue is the Pentagon’s decision to revisit the Satellite Communications Augmentation Resource (SCAR) program. The initiative focuses on building mobile ground stations used to track and operate spacecraft. Originally, it was awarded to BlueHalo, a subsidiary of AeroVironment acquired last year.

The U.S. Department of Defense is now reviewing the program's procurement structure. According to the SpaceNews report, the Pentagon is seeking to move away from cost-plus contracts and transition SCAR to a firm-fixed-price model, while potentially broadening the supplier base. Such changes could trigger a recompetition process, modifications to technical requirements, and renegotiation of contract terms. Each of these factors increases execution risk and diminishes AeroVironment's revenue certainty.

Uncertainty around SCAR is not entirely new. In a January SEC filing, the company disclosed that, by mutual agreement, the government had issued a stop-work order under its Other Transaction Agreement covering the delivery of BADGER phased-array antenna systems tied to the program. The pause was designed to allow negotiations under updated requirements, likely incorporating a fixed-price framework. While management has said it expects to continue supporting SCAR, final terms have yet to be settled.

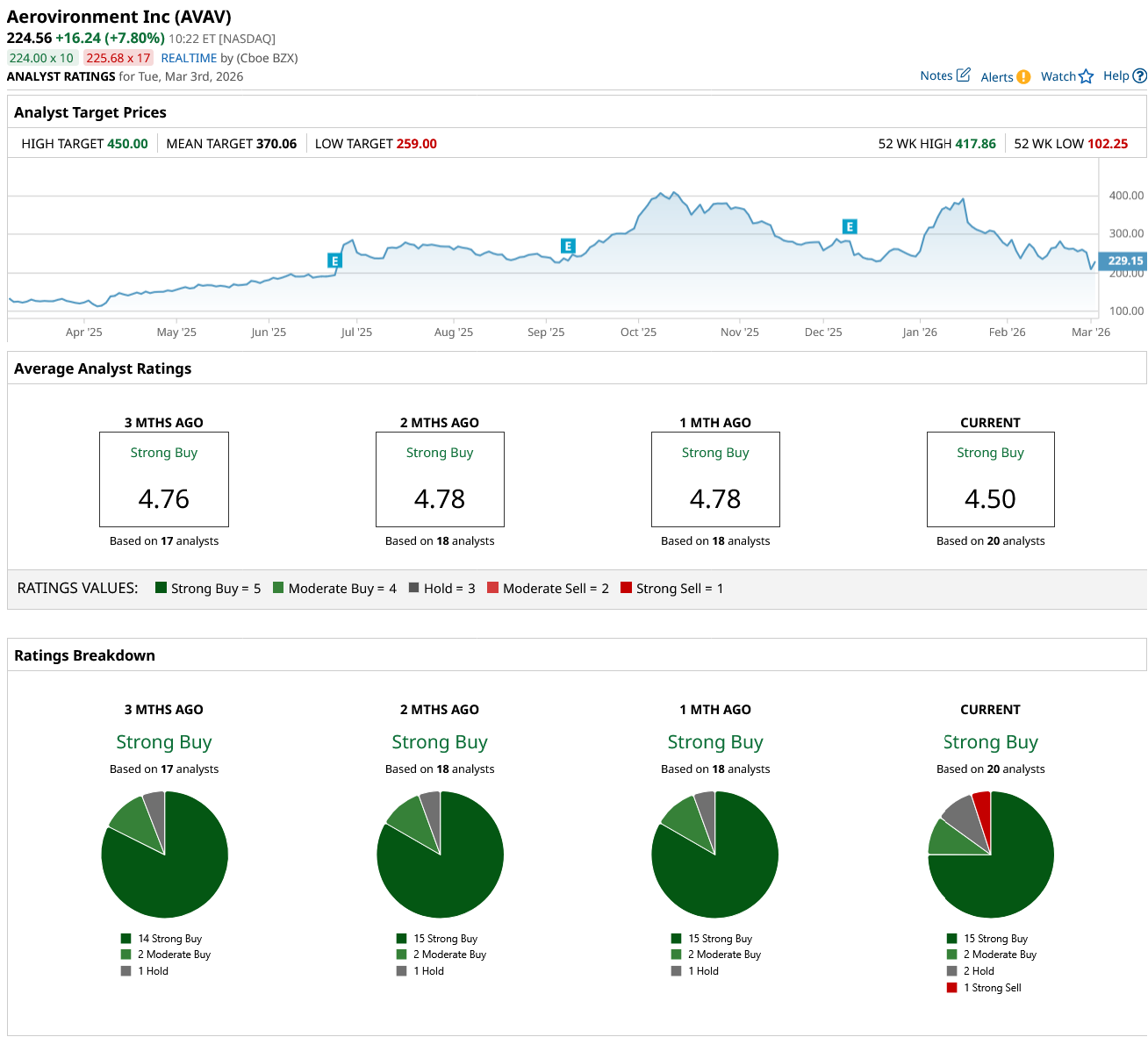

Investor sentiment was further pressured by a downgrade from Raymond James, which lowered its rating on the stock to “Underperform” from “Strong Buy.” The downgrade reflects potential contract risk, margin pressure, and increased competitive exposure. The analyst highlighted that if SCAR is significantly restructured or partially reassigned, a significant portion of the company’s backlog could be reduced. For a defense contractor valued in part on the predictability of government growth programs, backlog durability is critical.

More broadly, the situation reflects a shift in Pentagon procurement strategy toward cost control and supplier diversification. As for AeroVironment, it raises performance and pricing risks for contractors.

Is AVAV Stock a Buy Now?

While the latest development added uncertainty and pressured AeroVironment's share price, analysts maintain a “Strong Buy” consensus rating. For example, BTIG reiterated its “Buy” rating, noting that the contract in question was expected to represent only about 6% of annual revenue. In that context, the sharp intraday selloff appears disproportionate to the financial impact. While risk is elevated, the firm believes AeroVironment remains well positioned to benefit from future phased-array demand.

The broader geopolitical backdrop may also work in the company’s favor. Escalating tensions between the U.S., Israel, and Iran have rattled global markets, lifting oil prices and driving investors toward traditional safe havens. Historically, periods of geopolitical instability have led to increased defense spending, particularly on advanced systems aligned with modern warfare needs. That dynamic places AeroVironment in a strategic sweet spot.

AeroVironment focuses on unmanned systems and precision-strike technologies, with especially strong demand for its Switchblade loitering munitions. A recent $186 million delivery order from the U.S. Army for Switchblade 600 Block 2 and Switchblade 300 Block 20 highlights the platform’s expanding operational role. As military strategy shifts toward agile, technology-enabled engagements, these systems are increasingly integral.

The company’s operating performance has also been strong. Most recently, revenue surged 151% year-over-year (YoY) to $472.5 million, supported by organic growth and the integration of BlueHalo, which is expanding capabilities across cyber, space, and directed energy. AeroVironment has also reduced revenue concentration risk, with Ukraine-related sales expected to represent less than 5% of annual revenue.

Beyond Switchblade, additional platforms such as Titan, JUMP 20, JUMP20-X, and the emerging P550 expand the company’s addressable market. With global defense modernization entering a multi-year upcycle, AeroVironment’s long-term growth story remains intact.

While clarity on the SCAR program's structure is still needed, AVAV appears to be a compelling stock in the defense space.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart