It's reality now and science fiction no more. Joby Aviation (JOBY), the urban air mobility company with a focus on electric vertical takeoff and landing (eVTOL) vehicles, is partnering with Uber (UBER) to launch air taxi services in Dubai later this year. Users will be able to call the service from the Uber app if their trip qualifies, with the added benefit of Uber Black pick-up and drop-off.

“Our focus has always been on creating a flight experience that operates quietly and integrates naturally into the rhythm of city life," said Joby Chief Product Officer Eric Allison. "By partnering with Uber, we’re making this new mode of transportation familiar and accessible, connecting the ground and the sky through a system designed to save people time and fit seamlessly into how they already move.”

The electric air taxi will be flown by a certified commercial pilot with panoramic views from every seat. With top speeds of up to 200 mph, Joby's air taxi will have a range of 100 miles on one charge. Although pricing has not been revealed, industry estimates suggest that the per-seat fare could be between $50 to $100 for short-haul trips. Notably, Joby has long-stated that the initial target price for its air taxi service will be similar to high-end ground transportation, specifically Uber Black.

JOBY stock popped more than 4% on Feb. 26. Yet, the stock remains down by 25% on a year-to-date (YTD) basis. Can the realization of Joby's commercialization dream finally halt the rut in the JOBY stock and propel shares to new heights? Let's find out.

What Is Jolly With Joby (And What Is Not)?

In the realm of eVTOL, Joby is often seen as a frontrunner, having been founded way back in 2009 and also being one of the first among its peers to become publicly listed in August 2021. Moreover, what works in favor of Joby is that it is vertically integrated, meaning it plans to both manufacture its aircraft and operate the ride-sharing service. While this reduces dependence on others, it also requires significant control over costs.

Overall, the eVTOL sector holds considerable promise, and Joby Aviation stands out with several meaningful near- and medium-term catalysts. Key milestones include its advancement through Federal Aviation Administration (FAA) certification stages, with Stage 4 completion targeted for mid-2026 (potentially unlocking backlog from partners such as Delta (DAL)), scaling manufacturing to four aircraft per month by 2027 (supported by Toyota’s (TM) $1 billion investment and deployment of 200 engineers), and active participation in the FAA’s eVTOL Pilot Program, which is testing nationwide operations and anticipates around 25 vertiports in the coming years.

Going into specifics, what gives Joby a genuine technical edge is its proprietary low-noise profile and advanced propulsion setup. Instead of conventional helicopter-style rotors, the aircraft uses a distributed electric propulsion system with six custom tilting propellers. In joint testing with NASA, the vehicle recorded just 45.2 A-weighted decibels at 500 meters, which is quieter than competing quadrotor designs and barely noticeable against typical urban background noise. That quiet operation is a major advantage when securing permits to land in dense city environments. Moreover, the company’s custom high-nickel battery chemistry supports top speeds of 200 mph and a 150-mile range, clearly ahead of what many newer players can achieve.

That said, the biggest risk for Joby remains its pre-revenue status and the tight regulatory timeline. Cash burn is running high, with recent guidance pointing to annual usage above $500 million just to cover testing and factory ramp-up. JOBY stock’s valuation is almost entirely tied to the FAA certification schedule. Any significant hardware issues during final flight tests or further delays pushing certification into 2027 could burn through cash quickly, likely forcing highly dilutive equity raises. Recent U.S. Securities and Exchange Commission (SEC) filings also showed notable insider sales — more than 1.4 million shares — which have unsettled some retail investors.

Financials Not Taking Off

Joby may have reported a significant leap in revenues in the latest quarter, but its numbers still leave a lot to be desired. The fourth quarter of 2025 saw the company reporting revenues of $30.8 million, much higher than the previous year's figure of just $55,000. Moreover, losses also narrowed to $0.14 per share from $0.34 in the year-ago period, and came in narrower than the consensus estimate loss of $0.22 per share. This was a positive, as the company's losses had been coming in wider than the consensus estimates previously.

However, cash burn continues to remain an issue. Joby's net cash outflow from operating activities increased to $509.9 million in 2025 from $436.3 million in 2024 as the company continues to guzzle cash as it nears commercialization. Overall, the company closed the quarter with a cash balance of $240.8 million. This was much higher than its short-term debt levels of just $8.4 million, alleviating liquidity concerns in the near term.

Valuation-wise, Joby is not assessed on traditional metrics, as the company is yet to consistently generate profits. Yet, its price-to-sales (P/S) ratio of 171.6 times is much higher than the sector median.

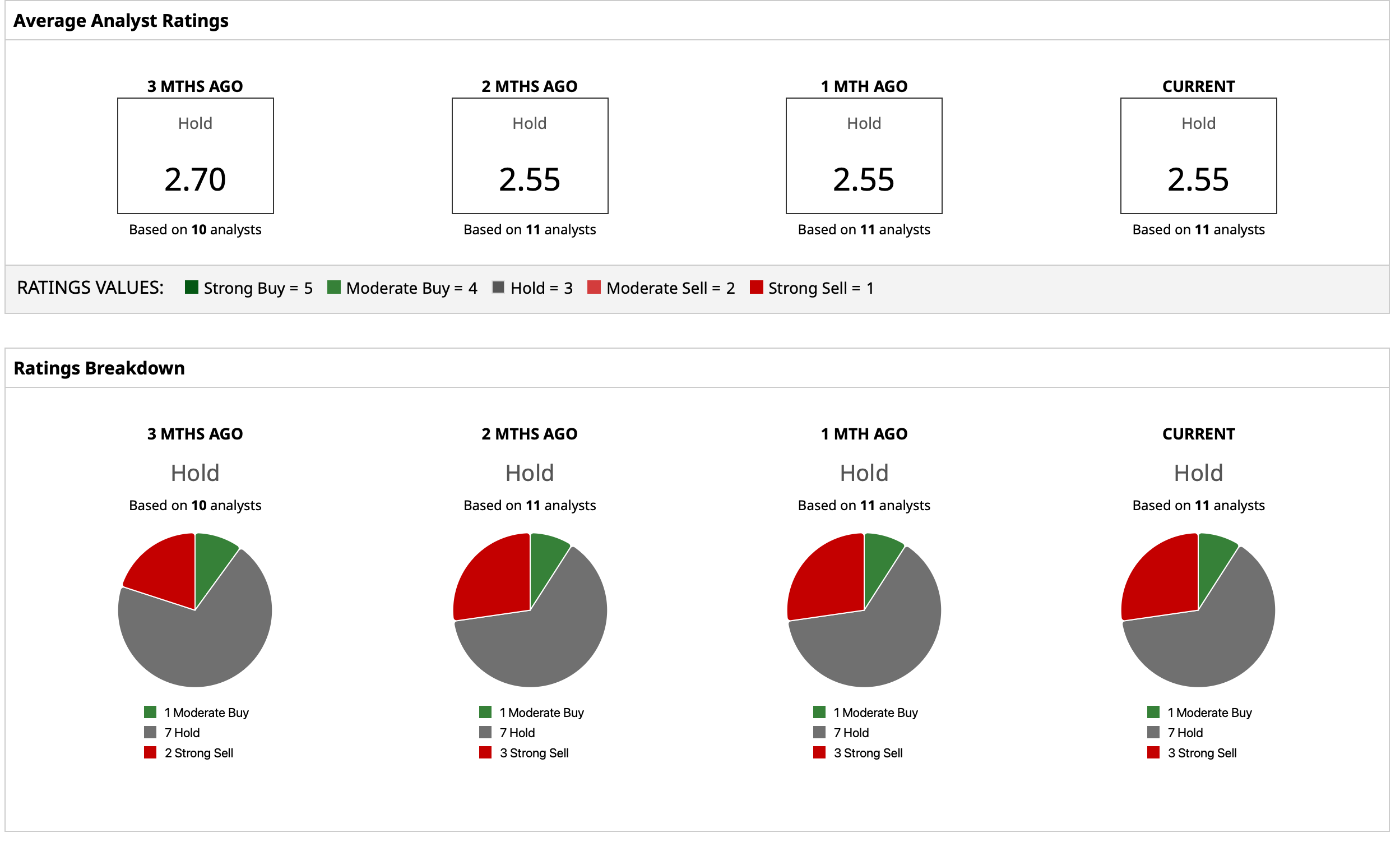

What Do Analysts Think of JOBY Stock?

Analysts have an overall rating of “Hold” for JOBY stock with a mean target price of $11.94, which denotes potential upside of about 16% from current levels. Out of 11 analysts covering the stock, one has a “Strong Buy” rating, one has a “Moderate Buy” rating, six have a “Hold” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart