After a strong performance in 2025, the rally in GE Vernova (GEV) stock has carried into 2026. GEV stock is up 34% so far this year and recently reached a record $894.93 on Feb. 25. Over the past 12 months, the stock has surged roughly 160%, driven by rising demand for electricity.

GE Vernova supplies power generation equipment and services, grid solutions, and energy storage systems. Demand for these offerings is accelerating as investment in artificial intelligence (AI) infrastructure, particularly data centers, continues to increase. At the same time, the ongoing electrification of transportation and commercial buildings is increasing power consumption. Moreover, the broader shift toward cleaner, more resilient energy systems is also driving a multi-year capital investment cycle in power infrastructure, creating sustained growth opportunities for the company.

The company’s expanding backlog and solid margins provide a strong base for growth in 2026 and beyond, boosting investor confidence. Adding to the positive outlook, GE Vernova announced plans to double its dividend in 2026 compared with 2025 and raised its share repurchase authorization to $10 billion from the previously approved $6 billion.

With demand accelerating and pricing trends remaining favorable, GE Vernova appears well-positioned to deliver continued growth, strengthening its investment case.

GE Vernova Is on a Solid Growth Trajectory

GE Vernova is on a solid growth trajectory, driven by continued momentum in the power and electrification segments. In 2025, orders climbed 34% organically to $59.3 billion, driven by robust equipment demand in both power and electrification, along with steady services growth across these segments. That surge pushed total backlog to $150 billion, providing significant revenue visibility.

Revenue for 2025 rose 9% year-over-year (YOY) to $38.1 billion, led by strength in electrification and gas power. More importantly, profitability improved significantly. Margins expanded meaningfully, supported by higher price realization, increased volumes, and operational productivity gains.

Supporting its profitability is the significant expansion in equipment backlog margin dollars. GE Vernova added $8 billion in equipment backlog margin dollars in 2025, more than the prior two years combined. Equipment backlog ended the year at $64 billion, roughly 50% higher YOY, with a six-point improvement in equipment margins. Within Power, margins increased by 11 points, largely due to strength in the gas power business.

Management expects this momentum to continue in 2026. Higher-priced gas slot reservation agreements are set to convert into orders, while grid equipment demand remains robust. Operationally, the company continues to focus on variable cost productivity, lean manufacturing, and capacity expansion. Gas turbine production capacity is set to increase to roughly 20 gigawatts annually beginning mid-2026, positioning the company to capitalize on sustained demand. At the same time, electrification margins are expected to benefit from pricing and volume leverage, as well as from the integration of the Prolec GE acquisition.

Guidance for 2026, now including the Prolec GE acquisition, reflects increased confidence. Revenue is projected at $44 billion to $45 billion, up from prior expectations of $41 billion to $42 billion. Adjusted EBITDA margins are expected to expand to 11% to 13%, versus 8.4% in 2025, as higher-priced backlog converts to revenue and execution improves. Earnings are expected to be weighted toward the second half, with the fourth quarter representing the peak in revenue and EBITDA.

Looking further, GE Vernova raised its 2028 outlook. The company now targets at least $56 billion in revenue by 2028, implying a low-teens compound annual growth rate (CAGR) from current levels. Adjusted EBITDA margins are projected to reach 20%, more than double 2025 levels.

With a rapidly expanding backlog, improving margins, and rising cash generation, GE Vernova appears well-positioned to deliver sustained, profitable growth, which could provide meaningful support for its share price.

Investors May Want to Hold GEV Stock With Partial Profit-Taking

GE Vernova’s rally to record highs is supported by strong demand and improving profitability. Order growth, a $150 billion backlog, expanding equipment margins, and raised 2026 and 2028 guidance indicate strong earnings ahead.

Looking forward, strong demand trends, accelerating free cash flow, dividend growth, and expanded buyback authorization support continued upside potential.

After a strong rally, investors may consider locking in partial gains. However, GEV stock’s underlying growth trajectory suggests its momentum will likely sustain. That implies investors may want to hold GEV stock and let it run.

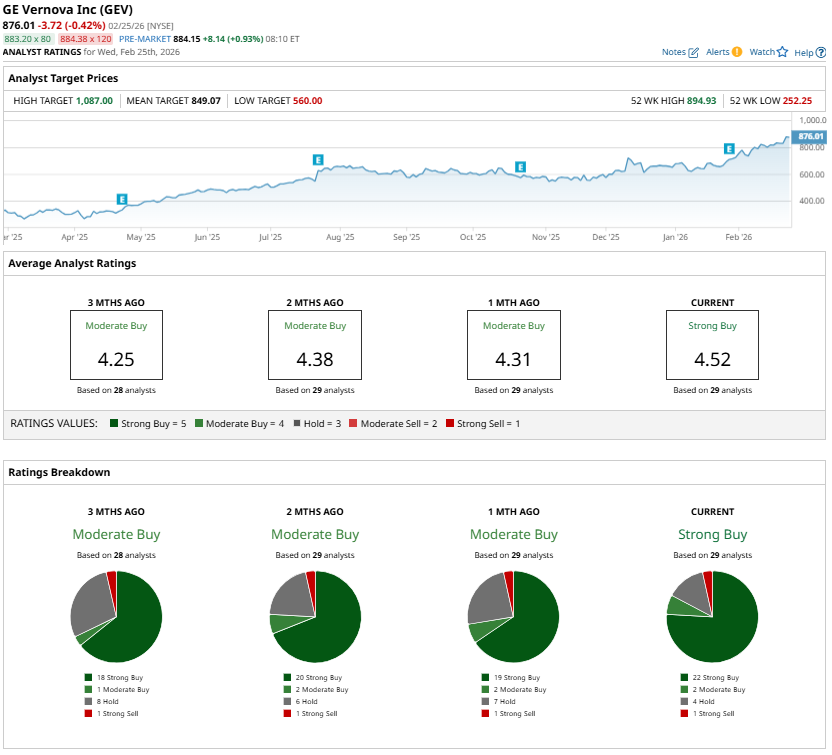

Analysts are also bullish on GEV stock, maintaining a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart