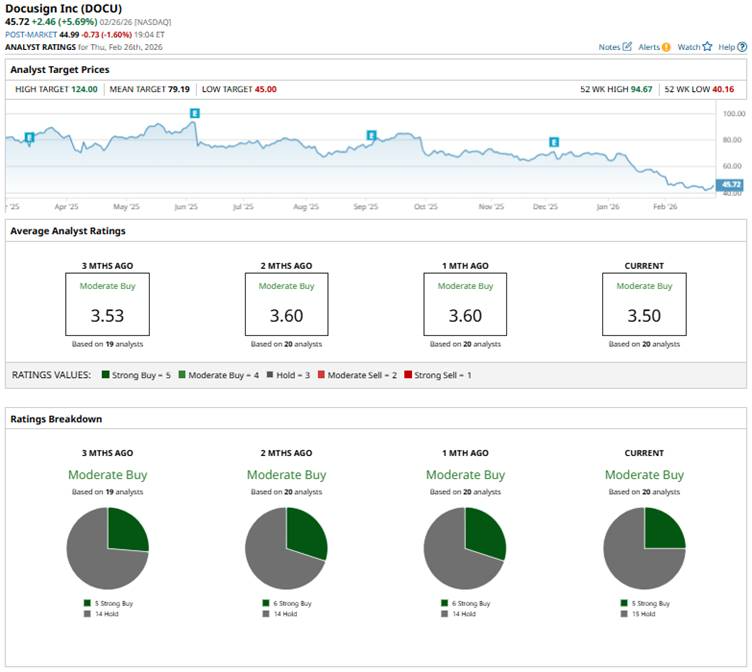

Despite challenging market conditions and a pullback in shares, DocuSign (DOCU) remains on the radar of some bullish analysts, anchored by its Street-high price target of $124 set by Citizens analyst Patrick Walravens, which implies 171.2% upside from recent share prices.

Analysts at Citizens, which maintains a “Market Outperform” rating on DOCU, view DocuSign as a compelling capital appreciation opportunity, citing its dominant e-signature franchise and its strong total addressable market as compelling long-term growth drivers.

This bullish valuation underscores a dramatic potential turnaround for a stock that’s been under pressure amid slower e-signature billings, suggesting, among some strategists, that DocuSign could deliver substantial appreciation through 2026.

About DocuSign Stock

DocuSign is a software company headquartered in San Francisco, California, that provides cloud-based electronic signature and digital agreement management solutions to businesses and organizations worldwide. The company’s platform enables users to prepare, sign, act on, and manage agreements securely on various devices, and it has expanded into broader agreement automation and intelligent contract-lifecycle offerings. DocuSign’s market cap stands at around $9.2 billion.

DocuSign’s share price has experienced significant weakness over the past year and into 2026, reflecting both company-specific execution challenges and broader sell-offs in software stocks. Over the past 52 weeks, DOCU has fallen sharply by 52% from its highs of around $94.67, reached in June 2025. The stock is down 44.25% over the past year.

Year-to-date (YTD), DocuSign’s stock has continued to struggle, down around 33.76% YTD, underperforming broader major indices and reinforcing the bear-leaning trend. Moreover, the stock slumped to its 52-week low of $40.16 on Feb. 25.

DocuSign’s stock is declining in 2026 largely due to weakening investor confidence, broad software sector pressure as investors rotated out of growth names, and negative analyst actions. Additionally, skepticism around the company’s ability to rapidly re-accelerate growth, particularly in its transition to the Intelligent Agreement Management (IAM) platform, relatively conservative guidance for billings, and revenue weighed on sentiment.

The stock is currently trading at 2.94 times sales, which is a discount to the sector median.

Mixed Financial Performance

DocuSign’s third quarter fiscal 2026 results, released on Dec. 4, 2025 for the period ended Oct. 31, showed a continuation of modest growth with several key metrics improving year-over-year (YOY) but also highlighted why investors are cautious about the company’s growth trajectory.

Total revenue came in at $818.4 million, representing an 8% increase compared to the prior year, while subscription revenue, the core of DocuSign’s SaaS business, grew 9% to $801 million, and billings rose 10% to $829.5 million.

Non-GAAP gross margin dipped slightly to 81.8%, and profitability improved meaningfully with non-GAAP EPS of $1.01, above the prior-year quarter’s $0.90 and above the consensus estimate.

The company also reported stronger cash flow, with net cash from operating activities at about $290.3 million and free cash flow of $262.9 million, both higher than the year-ago period.

Despite these positives, professional services revenue declined 14%, and margin compression in certain areas underscored mixed execution dynamics.

For the quarter ending Jan. 31, 2026, DocuSign guided to $825 million to $829 million in total revenue (7% YOY growth), $808 million to $812 million in subscription revenue (also 7% YOY), and $992 million to $1.002 billion in billings (about 8% YOY), while reiterating full-year fiscal 2026 expectations of roughly $3.208 billion to $3.212 billion in revenue and $3.379 billion to $3.389 billion in billings.

This combination of solid top line expansion but middling guidance tempered enthusiasm, as the market sought evidence of more robust acceleration in growth beyond mid-single-digit increases.

Analysts forecast EPS of $1.43 for fiscal 2026, a 22.2% YOY jump, followed by a further 12.6% rise to $1.61 in 2027.

What Do Analysts Expect for DocuSign Stock?

While firms like Citizens remain constructive on DocuSign, some analysts have turned more cautious in recent weeks.

Most notably, Jefferies downgraded the stock from “Buy” to “Hold,” with analyst Brent Thill slashing the price target from $105 to $45, a steep 57.1% reduction.

Also, on Feb. 18, BTIG analyst Allan Verkhovski reiterated a “Buy” rating but reduced his price target from $88 to $70, marking a 20.5% downward revision.

Overall, DOCU has a consensus “Moderate Buy” rating. Of the 20 analysts covering the stock, five advise a “Strong Buy,” and the remaining 15 analysts give it a “Hold” rating.

The average price target of $79.19 suggests an upside potential of 73.2% from current prices.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart