Headquartered in Indianapolis, Indiana, Eli Lilly and Company (LLY) researches, develops, and markets medicines across cardiometabolic disease, oncology, immunology, neuroscience, and beyond.

With a market capitalization of nearly $952.3 billion, it occupies “mega-cap” territory, an exclusive club reserved for companies valued above $200 billion. The scale allows the company to bankroll innovation, fortify global partnerships, and strengthen licensing alliances that keep its pipeline both deep and defensible.

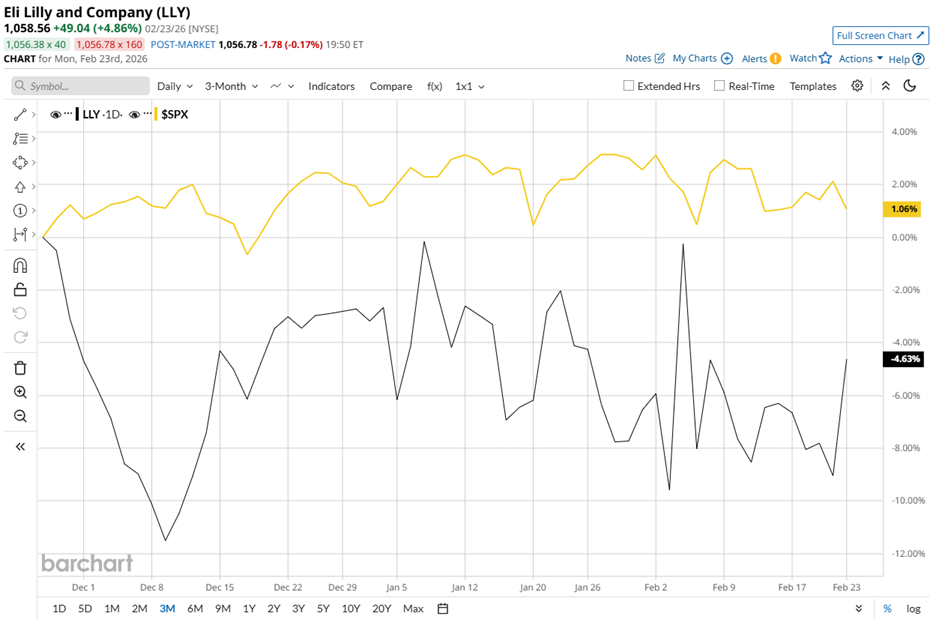

In terms of price performance, LLY stock is currently trading 6.7% below its January high of $1,133.95, and it has edged down only marginally over the past three months. Meanwhile, the S&P 500 Index ($SPX) has gained 3.6% during the same stretch.

Over the last 52 weeks, however, LLY stock has appreciated 21.2%, comfortably surpassing the index’s 13.7% gain. Year-to-date (YTD), Eli Lilly’s shares slipped 1.5%, while the broader benchmark declined only marginally.

Technical indicators reinforce the constructive backdrop. Since early October, LLY stock has held above its 50-day moving average of $1,052.05, aside from a brief January-end pullback that buyers quickly erased. More importantly, it has remained firmly above its 200-day moving average of $868.80 throughout the same period.

On Feb. 4, fundamentals provided fresh validation following the company’s Q4 fiscal 2025 results as shares surged 10.3% immediately after the announcement. Revenue increased 42.6% year over year to $19.29 billion, exceeding analyst expectations of $17.96 billion. Adjusted EPS climbed 41.7% to $7.54, surpassing the Street’s forecast of $6.93.

The quarterly strength was fueled by robust demand for Zepbound and Mounjaro, as both products captured accelerating adoption in the rapidly expanding weight-loss and diabetes markets.

Looking ahead, Eli Lilly’s management forecasts fiscal 2026 revenue in the range of $80 billion to $83 billion and non-GAAP EPS between $33.50 and $35.00. These projections communicate assertive confidence and signal management’s expectation that current momentum will translate into durable, scaled profitability.

To sharpen the comparison, Eli Lilly’s rival Johnson & Johnson (JNJ) has delivered a 51.5% gain over the past 52 weeks and an 18.9% rise YTD. The outperformance sets a demanding pace and, more importantly, highlights the performance gap Lilly can still close.

Yet analysts do not flinch. Among 29 analysts covering the stock, the overall rating stands at a “Strong Buy.” Moreover, the average price target of $1,233.65 signaling 16.5% potential upside from current levels, makes it clear that the Street expects Eli Lilly to translate operational strength into sustained market leadership and continued shareholder gains.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Walmart Raises Its Dividend 5%, Should You Buy WMT Stock?

- Novo Nordisk Stock Is Deeply Oversold on Weight Loss Drug Fail. Should You Buy the Dip?

- Should You Buy Dell Stock Before February 26? This Analyst Says Yes.

- Everything You Need to Know About Musk’s ‘Self-Growing’ Moon City as He Races to ‘Secure the Future of Civilization’