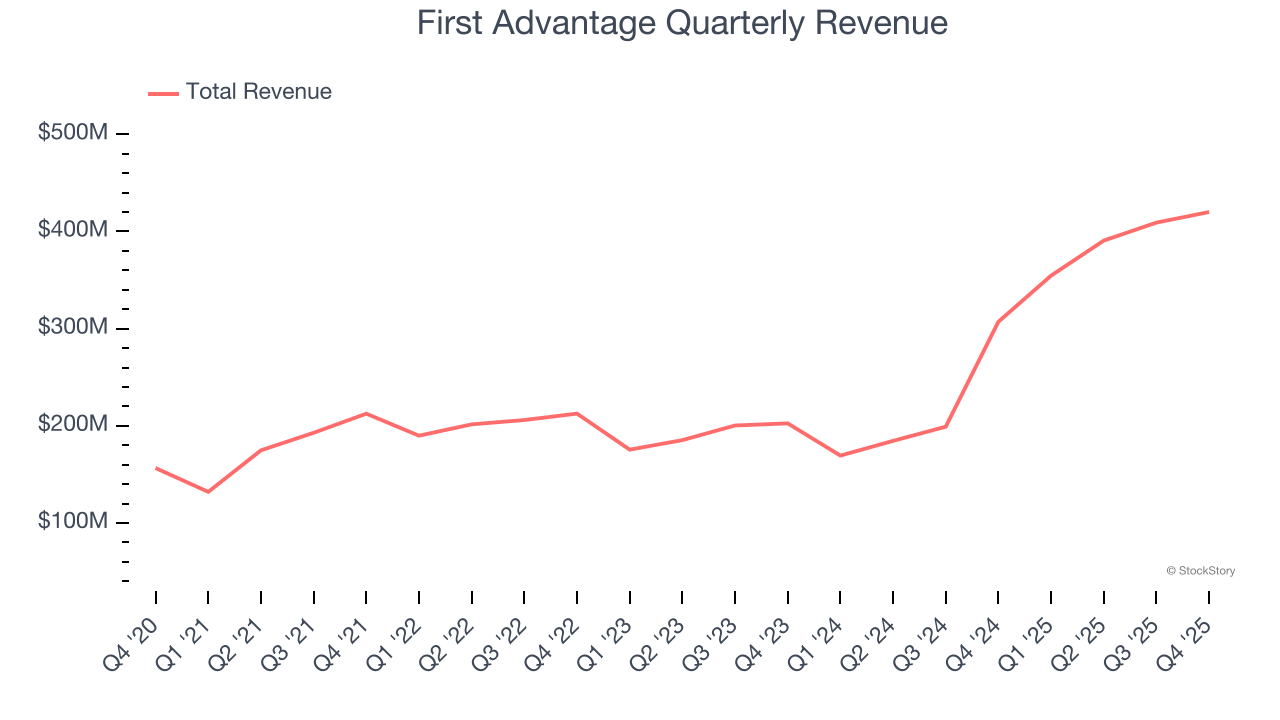

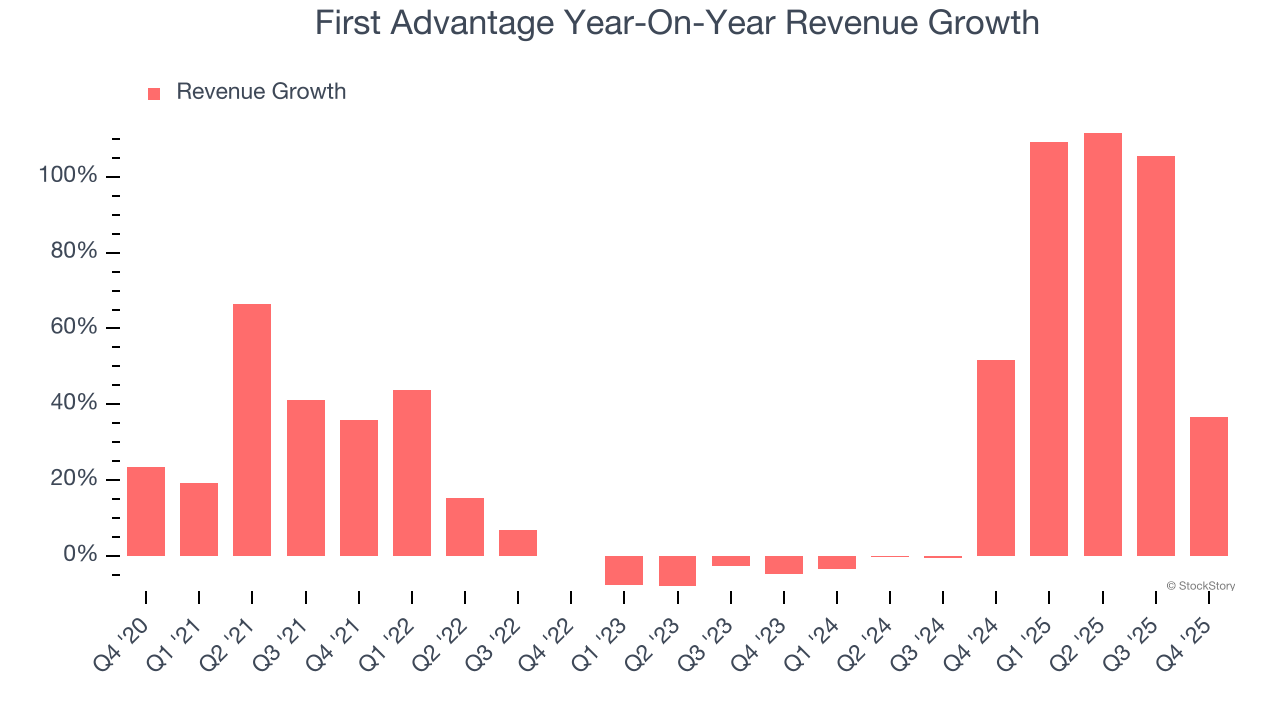

Background screening provider First Advantage (NASDAQ: FA) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 36.8% year on year to $420 million. The company’s full-year revenue guidance of $1.66 billion at the midpoint came in 2.4% above analysts’ estimates. Its non-GAAP profit of $0.30 per share was 13.7% above analysts’ consensus estimates.

Is now the time to buy First Advantage? Find out by accessing our full research report, it’s free.

First Advantage (FA) Q4 CY2025 Highlights:

- Revenue: $420 million vs analyst estimates of $391.3 million (36.8% year-on-year growth, 7.3% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.26 (13.7% beat)

- Adjusted EBITDA: $116.8 million vs analyst estimates of $110 million (27.8% margin, 6.2% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.20 at the midpoint, beating analyst estimates by 1.3%

- EBITDA guidance for the upcoming financial year 2026 is $472.5 million at the midpoint, in line with analyst expectations

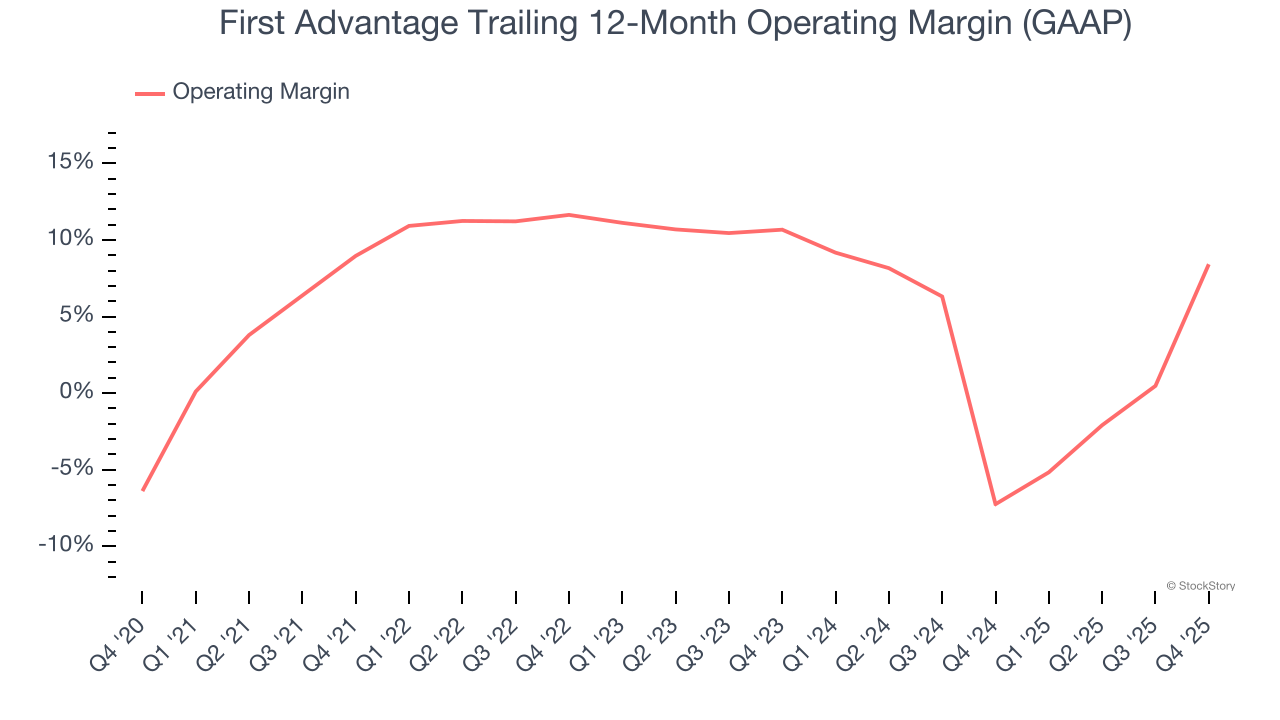

- Operating Margin: 10.7%, up from -26.3% in the same quarter last year

- Free Cash Flow was $65.94 million, up from -$96.16 million in the same quarter last year

- Market Capitalization: $1.66 billion

“In 2025, we delivered exceptional financial results with meaningful success across all pillars of our FA 5.0 growth strategy,” said Scott Staples, Chief Executive Officer.

Company Overview

Processing approximately 100 million background checks annually across more than 200 countries and territories, First Advantage (NASDAQ: FA) provides employment background screening, identity verification, and compliance solutions to help companies manage hiring risks.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.57 billion in revenue over the past 12 months, First Advantage is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, First Advantage’s 25.3% annualized revenue growth over the last five years was incredible. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. First Advantage’s annualized revenue growth of 43.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, First Advantage reported wonderful year-on-year revenue growth of 36.8%, and its $420 million of revenue exceeded Wall Street’s estimates by 7.3%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

First Advantage’s operating margin has risen over the last 12 months and averaged 6.6% over the last five years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports paltry profitability for a business services business.

Analyzing the trend in its profitability, First Advantage’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, First Advantage generated an operating margin profit margin of 10.7%, up 37 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

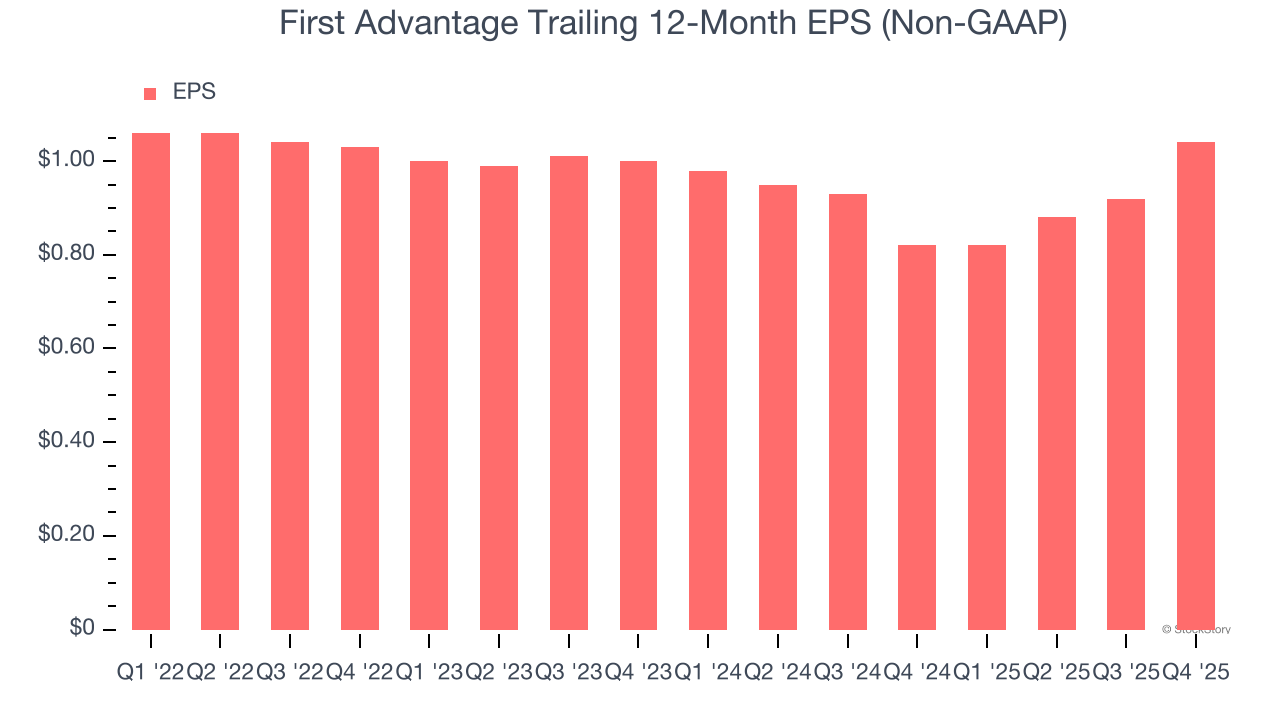

First Advantage’s full-year EPS was flat over the last four years, worse than the broader business services sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

First Advantage’s EPS grew at a weak 2% compounded annual growth rate over the last two years, lower than its 43.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

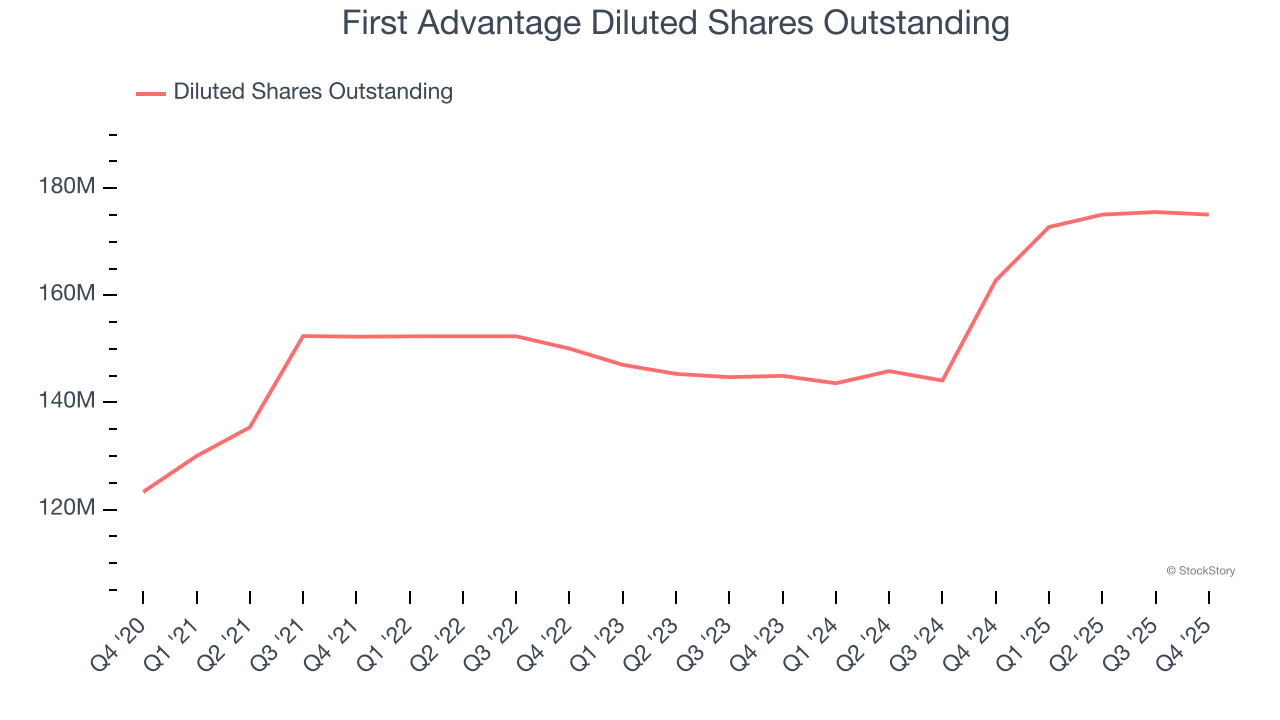

We can take a deeper look into First Advantage’s earnings to better understand the drivers of its performance. We mentioned earlier that First Advantage’s operating margin expanded this quarter, but a two-year view shows its margin has declinedwhile its share count has grown 20.8%. This means the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, First Advantage reported adjusted EPS of $0.30, up from $0.18 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects First Advantage’s full-year EPS of $1.04 to grow 15.8%.

Key Takeaways from First Advantage’s Q4 Results

We were impressed by how significantly First Advantage blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $9.52 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).