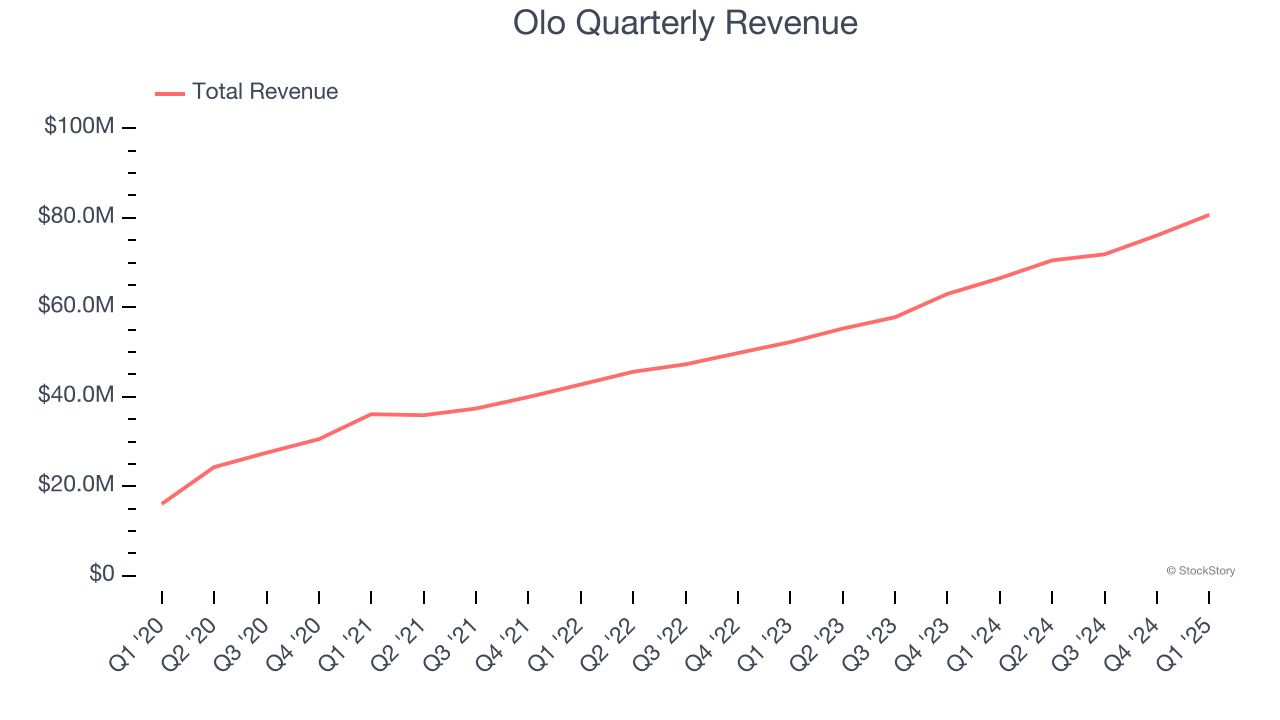

Restaurant software company (NYSE: OLO) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 21.3% year on year to $80.68 million. Guidance for next quarter’s revenue was better than expected at $82.25 million at the midpoint, 0.5% above analysts’ estimates. Its non-GAAP profit of $0.07 per share was in line with analysts’ consensus estimates.

Is now the time to buy Olo? Find out by accessing our full research report, it’s free.

Olo (OLO) Q1 CY2025 Highlights:

- Revenue: $80.68 million vs analyst estimates of $77.47 million (21.3% year-on-year growth, 4.1% beat)

- Adjusted EPS: $0.07 vs analyst estimates of $0.06 (in line)

- Adjusted Operating Income: $11.53 million vs analyst estimates of $8.66 million (14.3% margin, 33.1% beat)

- The company lifted its revenue guidance for the full year to $339.3 million at the midpoint from $334.5 million, a 1.4% increase

- Operating Margin: -3%, up from -10.8% in the same quarter last year

- Free Cash Flow was -$1.90 million, down from $6.85 million in the previous quarter

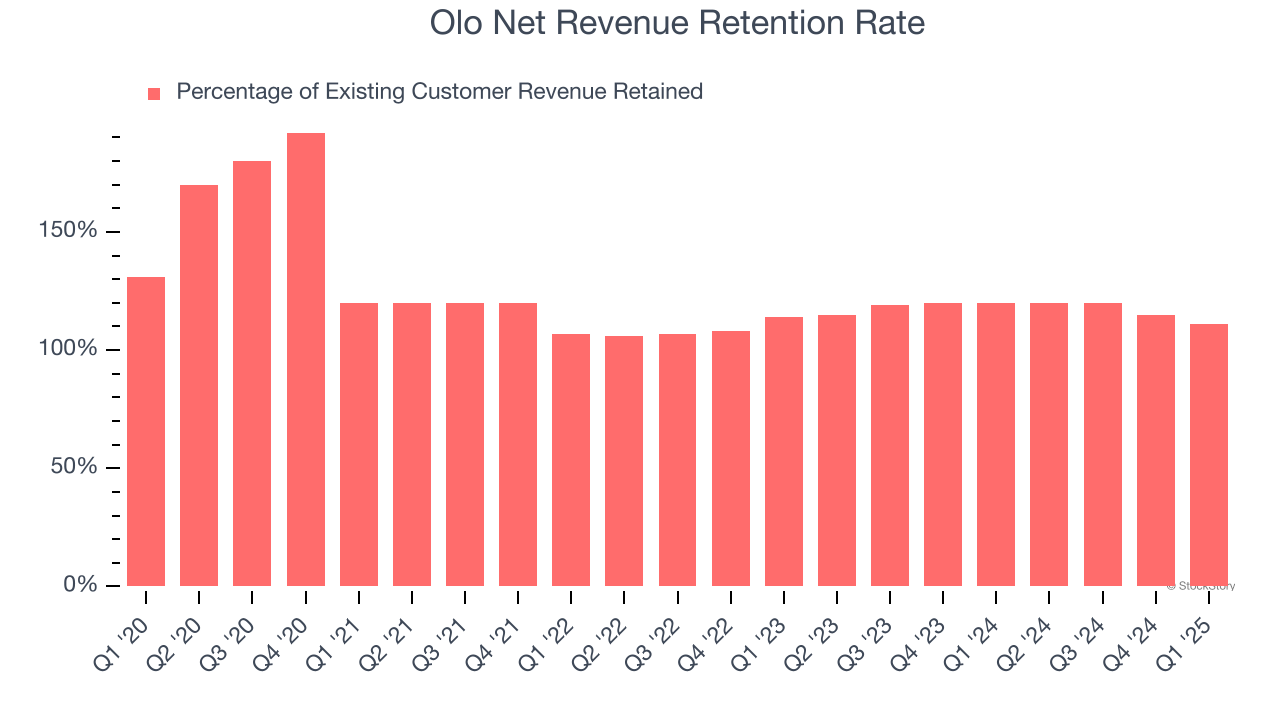

- Net Revenue Retention Rate: 111%, down from 115% in the previous quarter

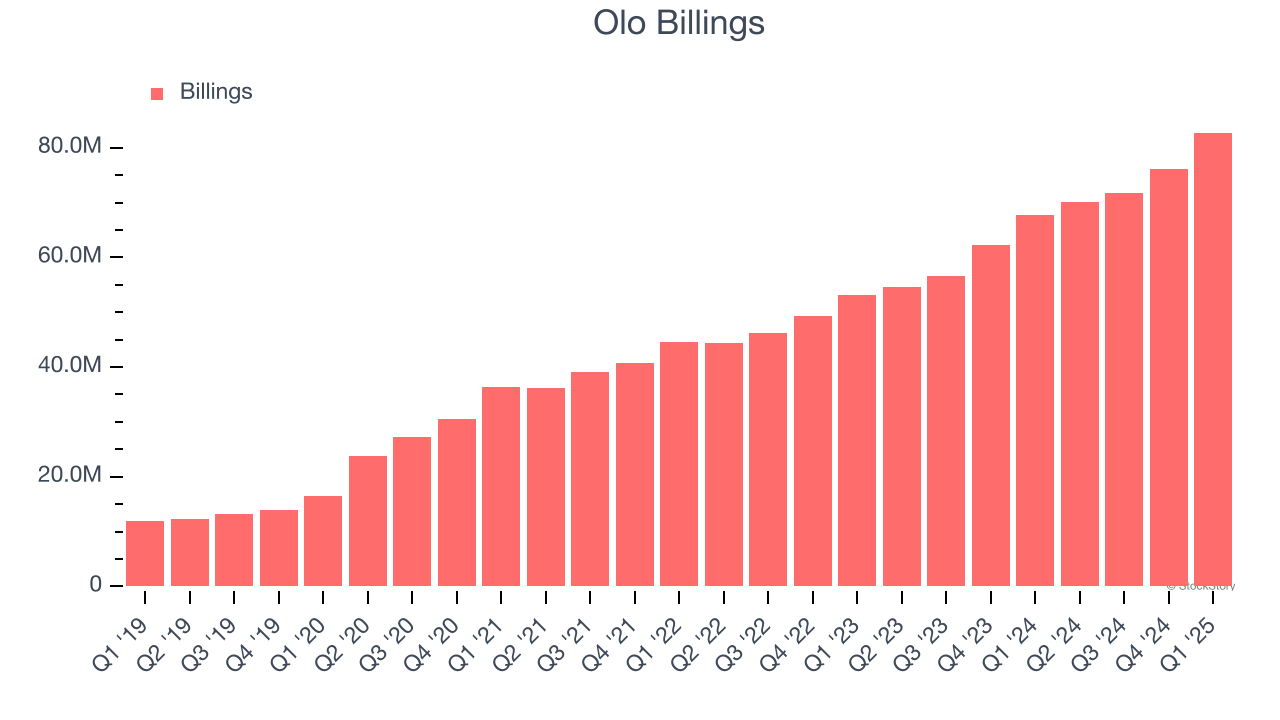

- Billings: $82.76 million at quarter end, up 22.2% year on year

- Market Capitalization: $1.25 billion

Company Overview

Founded by Noah Glass, who wanted to get a cup of coffee faster on his way to work, Olo (NYSE: OLO) provides restaurants and food retailers with software to manage food orders and delivery.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Olo grew its sales at a solid 24.2% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers.

This quarter, Olo reported robust year-on-year revenue growth of 21.3%, and its $80.68 million of revenue topped Wall Street estimates by 4.1%. Company management is currently guiding for a 16.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 17.2% over the next 12 months, a deceleration versus the last three years. Still, this projection is commendable and implies the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Olo’s billings punched in at $82.76 million in Q1, and over the last four quarters, its growth was impressive as it averaged 24.9% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Olo’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 117% in Q1. This means Olo would’ve grown its revenue by 16.5% even if it didn’t win any new customers over the last 12 months.

Despite falling over the last year, Olo still has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

Key Takeaways from Olo’s Q1 Results

We were impressed by how significantly Olo blew past analysts’ revenue, billings, and adjusted operating income expectations this quarter. We were also happy it lifted its full-year revenue guidance. On the other hand, its net revenue retention fell, but we still think this was a solid quarter with some key areas of upside. The stock traded up 4.1% to $8.37 immediately after reporting.

Olo put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.