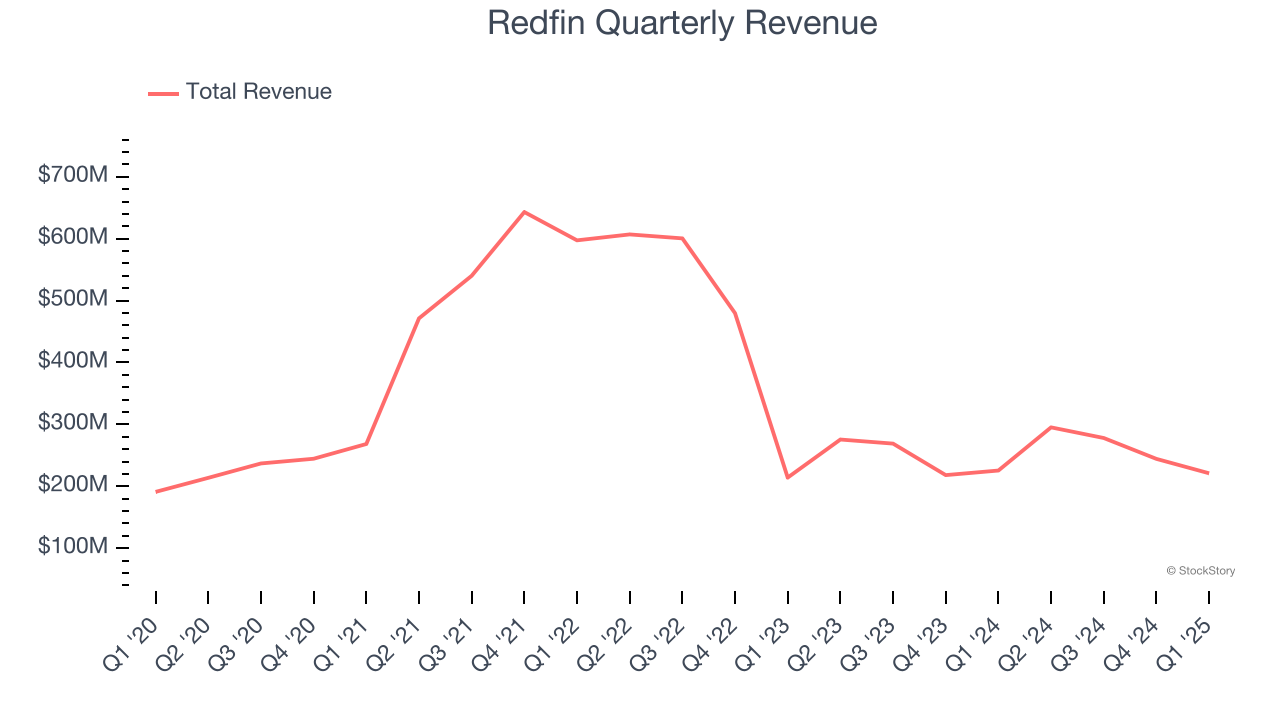

Real estate technology company Redfin (NASDAQ: RDFN) met Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 2% year on year to $221 million. Its GAAP loss of $0.73 per share was 4.7% below analysts’ consensus estimates.

Is now the time to buy Redfin? Find out by accessing our full research report, it’s free.

Redfin (RDFN) Q1 CY2025 Highlights:

- Revenue: $221 million vs analyst estimates of $221 million (2% year-on-year decline, in line)

- EPS (GAAP): -$0.73 vs analyst expectations of -$0.70 (4.7% miss)

- Adjusted EBITDA: -$31.96 million vs analyst estimates of -$34.93 million (-14.5% margin, 8.5% beat)

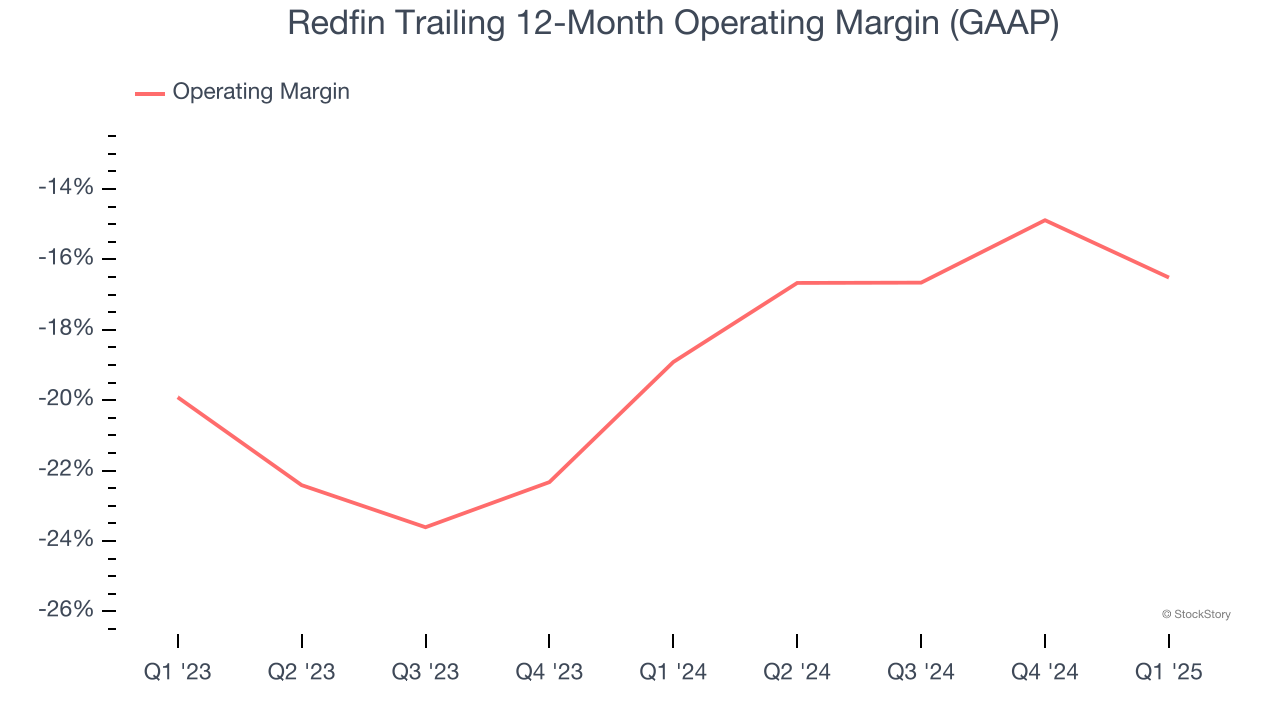

- Operating Margin: -38.7%, down from -30.7% in the same quarter last year

- Free Cash Flow was $34.64 million, up from -$49.54 million in the same quarter last year

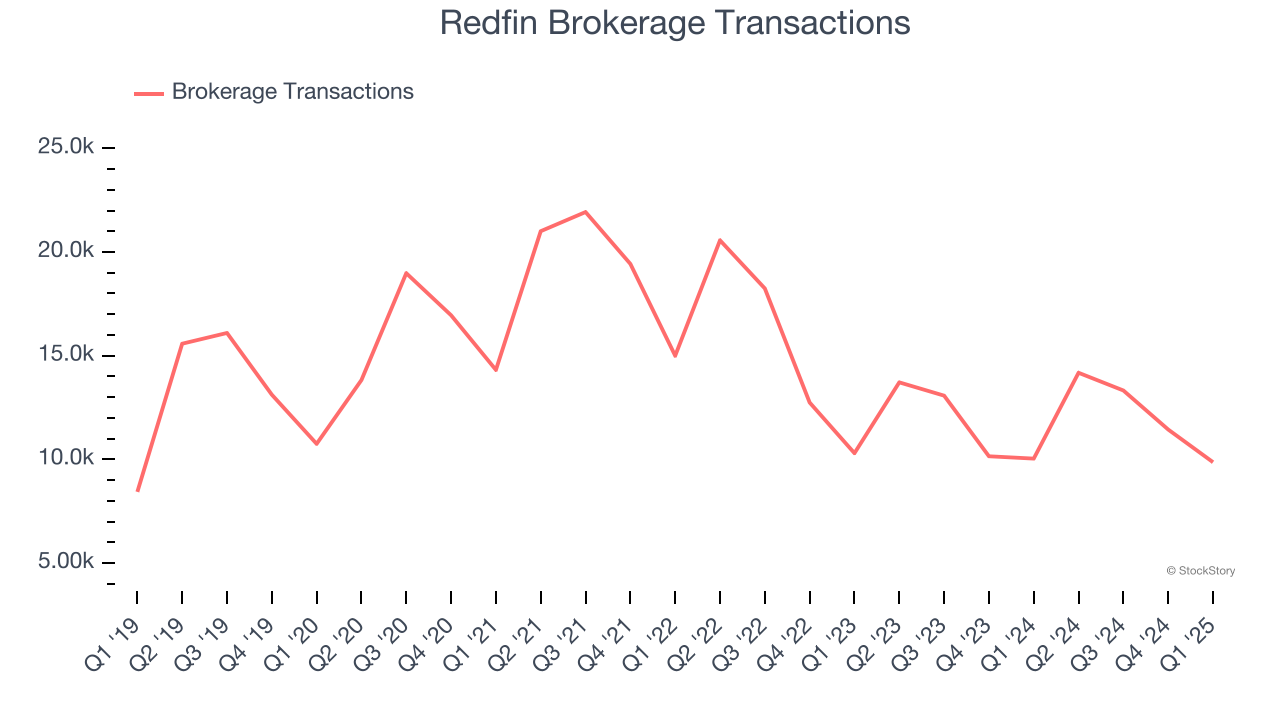

- Brokerage Transactions: 9,866, down 173 year on year

- Market Capitalization: $1.18 billion

"Redfin profits were at the high end of the guidance we gave investors in our last earnings call," said Redfin CEO Glenn Kelman.

Company Overview

Founded by a former medical school student, electrical engineer, and Amazon data engineer, Redfin (NASDAQ: RDFN) is a real estate company offering brokerage services through an online platform.

Sales Growth

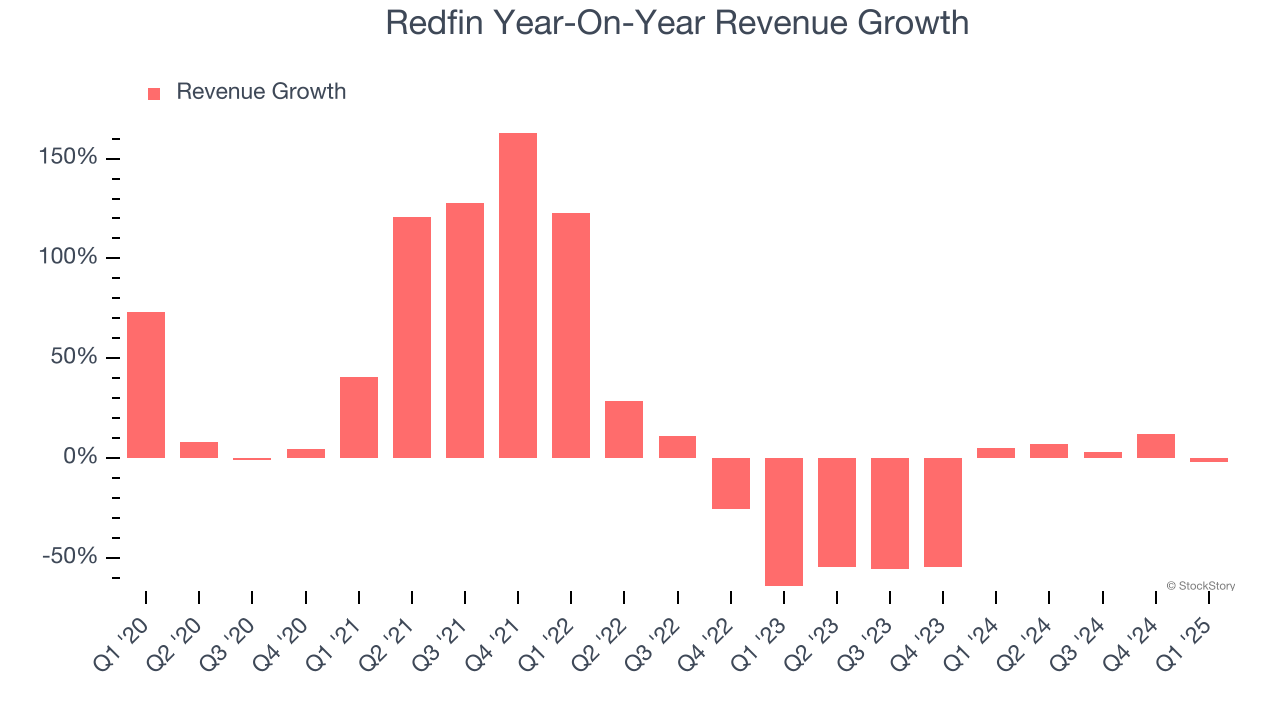

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Redfin grew its sales at a sluggish 3.8% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Redfin’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 26.1% annually.

We can dig further into the company’s revenue dynamics by analyzing its number of brokerage transactions and partner transactions, which clocked in at 9,866 and 2,389 in the latest quarter. Over the last two years, Redfin’s brokerage transactions averaged 8.5% year-on-year declines while its partner transactions averaged 3.8% year-on-year declines.

This quarter, Redfin reported a rather uninspiring 2% year-on-year revenue decline to $221 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Redfin’s operating margin has been trending up over the last 12 months, but it still averaged negative 17.7% over the last two years. This is due to its large expense base and inefficient cost structure.

Redfin’s operating margin was negative 38.7% this quarter. The company's consistent lack of profits raise a flag.

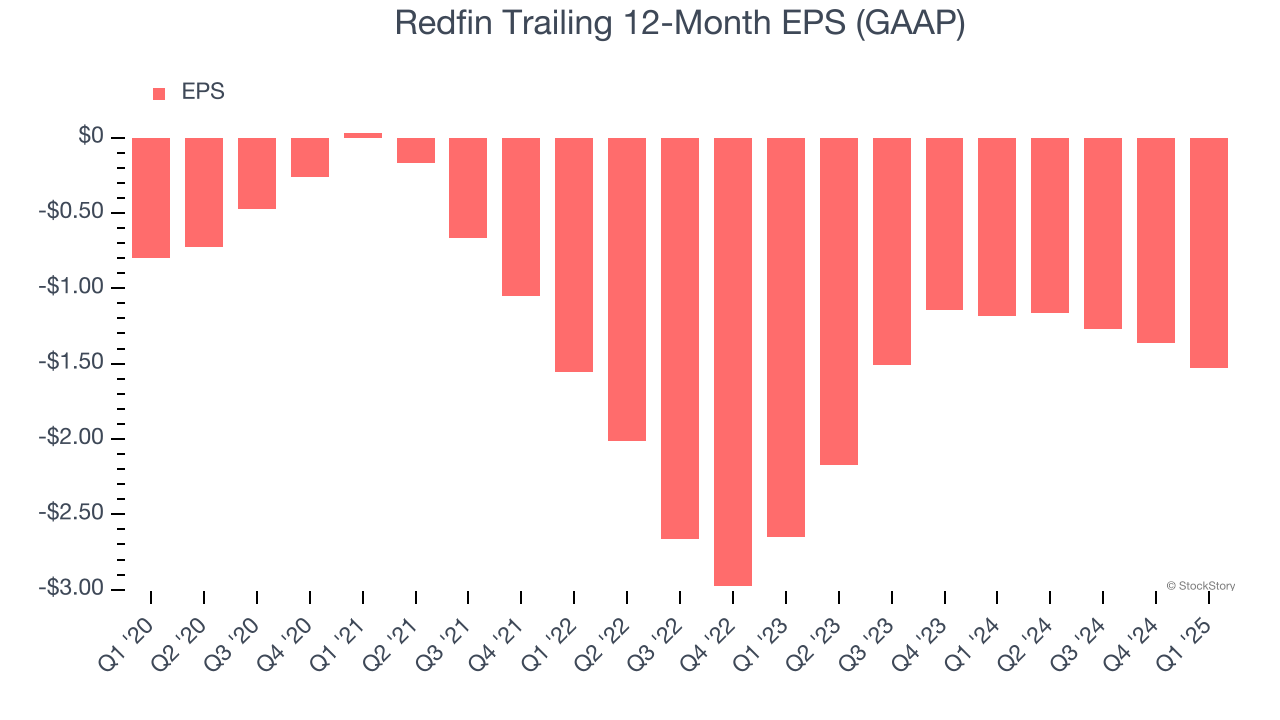

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Redfin’s earnings losses deepened over the last five years as its EPS dropped 13.9% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Redfin’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, Redfin reported EPS at negative $0.73, down from negative $0.56 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Redfin to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.53 will advance to negative $0.86.

Key Takeaways from Redfin’s Q1 Results

It was encouraging to see Redfin beat analysts’ EBITDA expectations this quarter. On the other hand, its number of brokerage transactions and EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $8.91 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.