American Airlines’s 24.1% return over the past six months has outpaced the S&P 500 by 9.9%, and its stock price has climbed to $14.23 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in American Airlines, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Do We Think American Airlines Will Underperform?

We’re glad investors have benefited from the price increase, but we don't have much confidence in American Airlines. Here are three reasons there are better opportunities than AAL and a stock we'd rather own.

1. Weak Growth in Revenue Passenger Miles Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like American Airlines, our preferred volume metric is revenue passenger miles). While both are important, the latter is the most critical to analyze because prices have a ceiling.

American Airlines’s revenue passenger miles came in at 66.58 billion in the latest quarter, and over the last two years, averaged 4.4% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

2. Free Cash Flow Projections Disappoint

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts’ consensus estimates show they’re expecting American Airlines’s free cash flow margin of 1.6% for the last 12 months to remain the same.

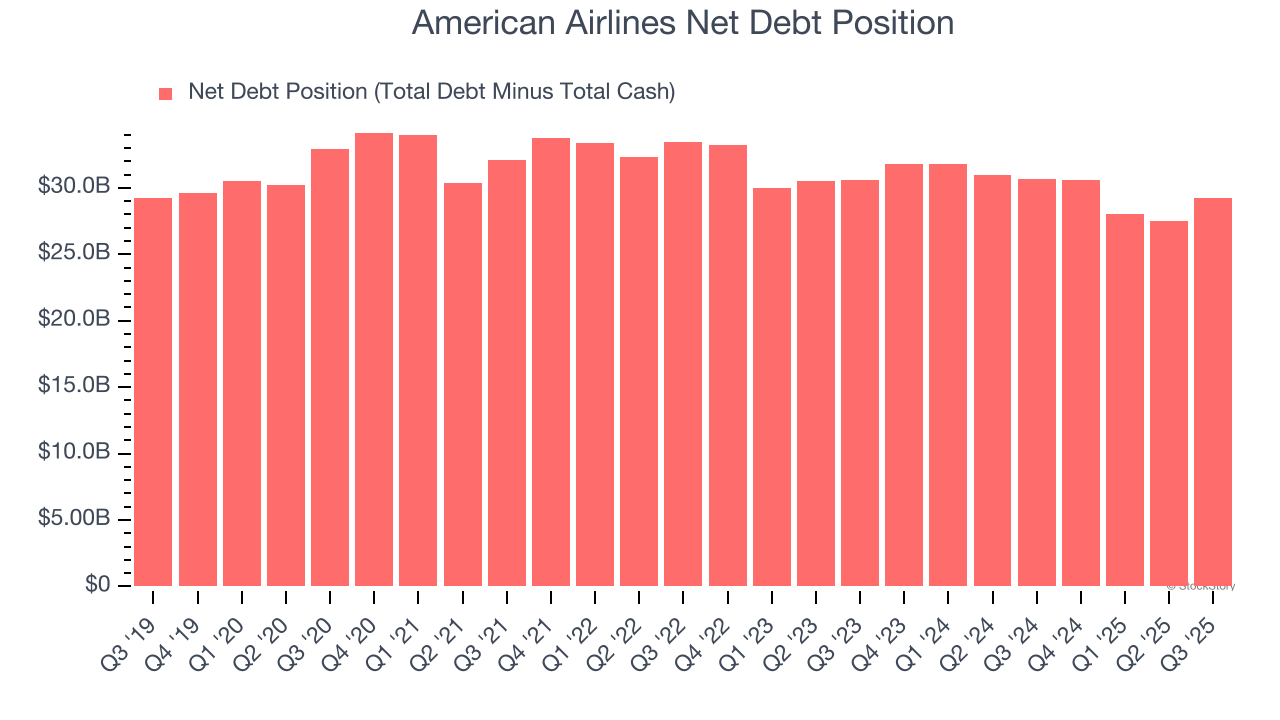

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

American Airlines’s $36.06 billion of debt exceeds the $6.86 billion of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $4.21 billion over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. American Airlines could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope American Airlines can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of American Airlines, we’ll be cheering from the sidelines. With its shares topping the market in recent months, the stock trades at 8.4× forward P/E (or $14.23 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.