Telecommunications infrastructure company Lumen Technologies (NYSE: LUMN) announced better-than-expected revenue in Q3 CY2025, but sales fell by 4.2% year on year to $3.09 billion. Its non-GAAP loss of $0.20 per share was 25% above analysts’ consensus estimates.

Is now the time to buy Lumen? Find out by accessing our full research report, it’s free for active Edge members.

Lumen (LUMN) Q3 CY2025 Highlights:

- Revenue: $3.09 billion vs analyst estimates of $3.06 billion (4.2% year-on-year decline, 0.9% beat)

- Adjusted EPS: -$0.20 vs analyst estimates of -$0.27 (25% beat)

- Adjusted EBITDA: $216 million vs analyst estimates of $761.7 million (7% margin, 71.6% miss)

- EBITDA guidance for the full year is $3.3 billion at the midpoint, below analyst estimates of $3.37 billion

- Operating Margin: -3.8%, down from 3.9% in the same quarter last year

- Free Cash Flow Margin: 47.6%, up from 37.2% in the same quarter last year

- Market Capitalization: $11.29 billion

“This quarter, we demonstrated what disciplined execution and bold ambition can achieve,” said Kate Johnson, president and CEO of Lumen Technologies.

Company Overview

With approximately 350,000 route miles of fiber optic cable spanning North America and the Asia Pacific, Lumen Technologies (NYSE: LUMN) operates a vast fiber optic network that provides communications, cloud connectivity, security, and IT solutions to businesses and consumers.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $12.69 billion in revenue over the past 12 months, Lumen is larger than most business services companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices. However, its scale is a double-edged sword because finding new avenues for growth becomes difficult when you already have a substantial market presence. To expand meaningfully, Lumen likely needs to tweak its prices, innovate with new offerings, or enter new markets.

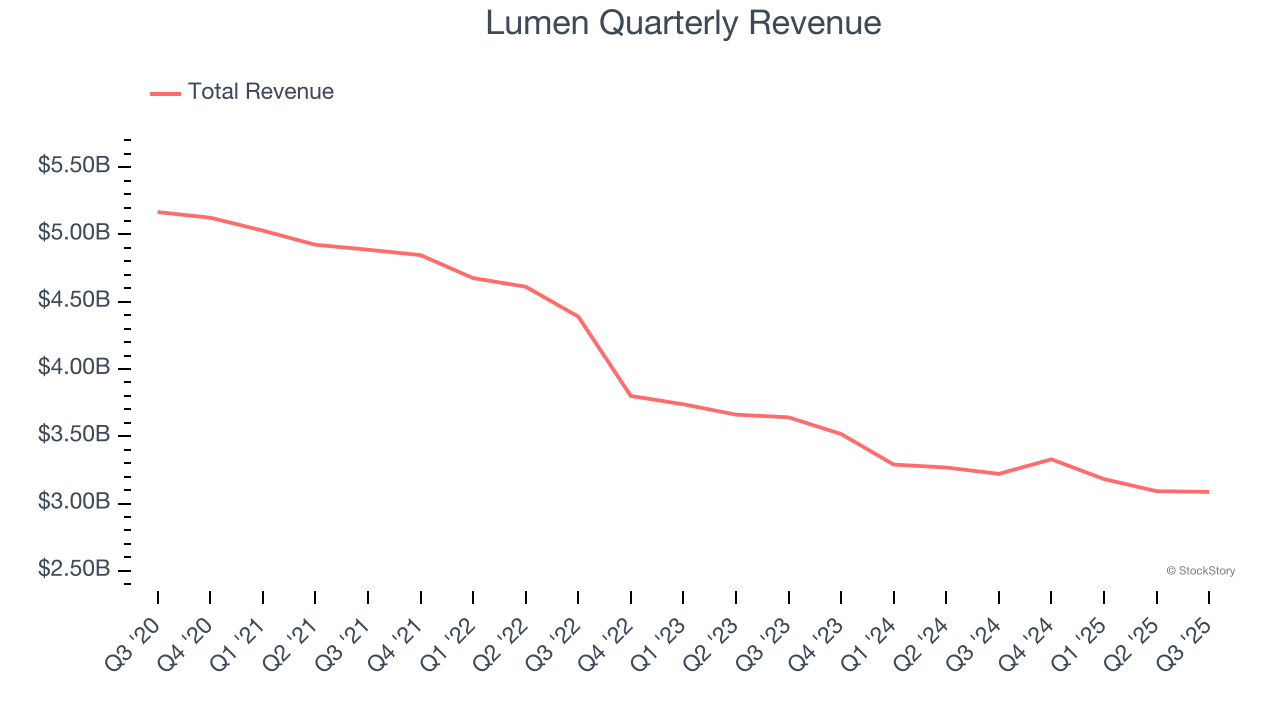

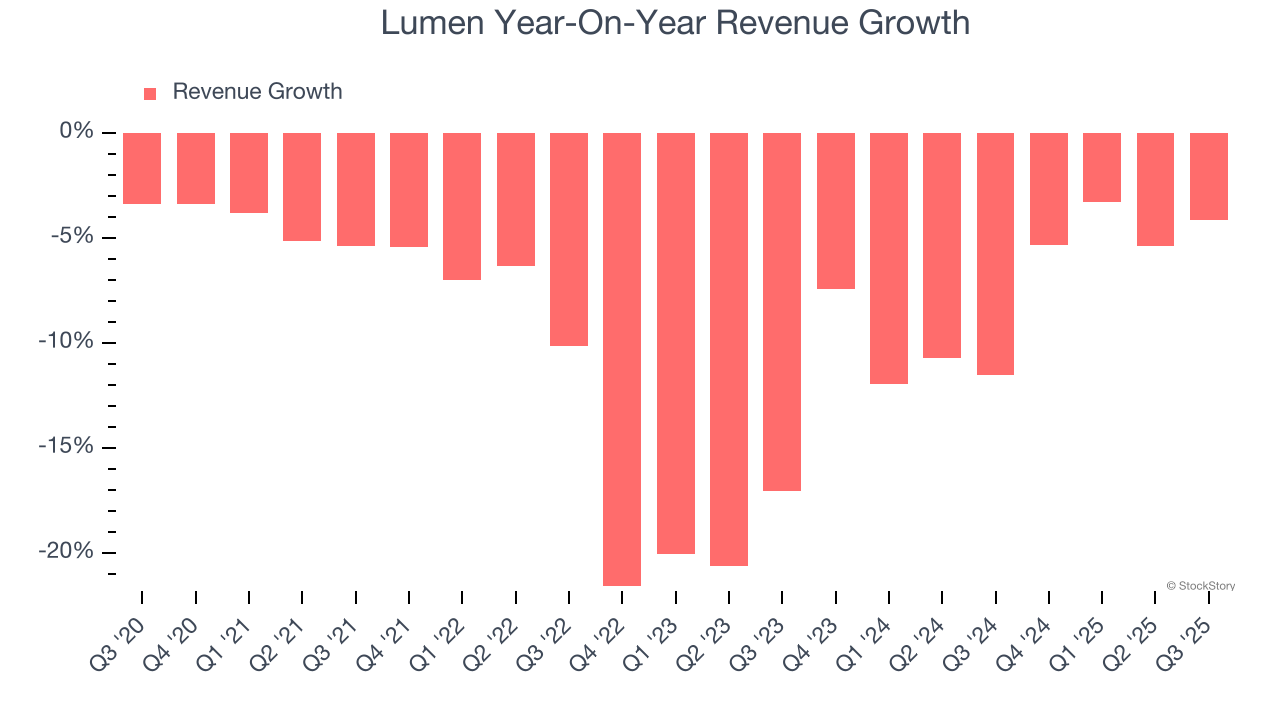

As you can see below, Lumen struggled to generate demand over the last five years. Its sales dropped by 9.5% annually, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Lumen’s annualized revenue declines of 7.5% over the last two years suggest its demand continued shrinking.

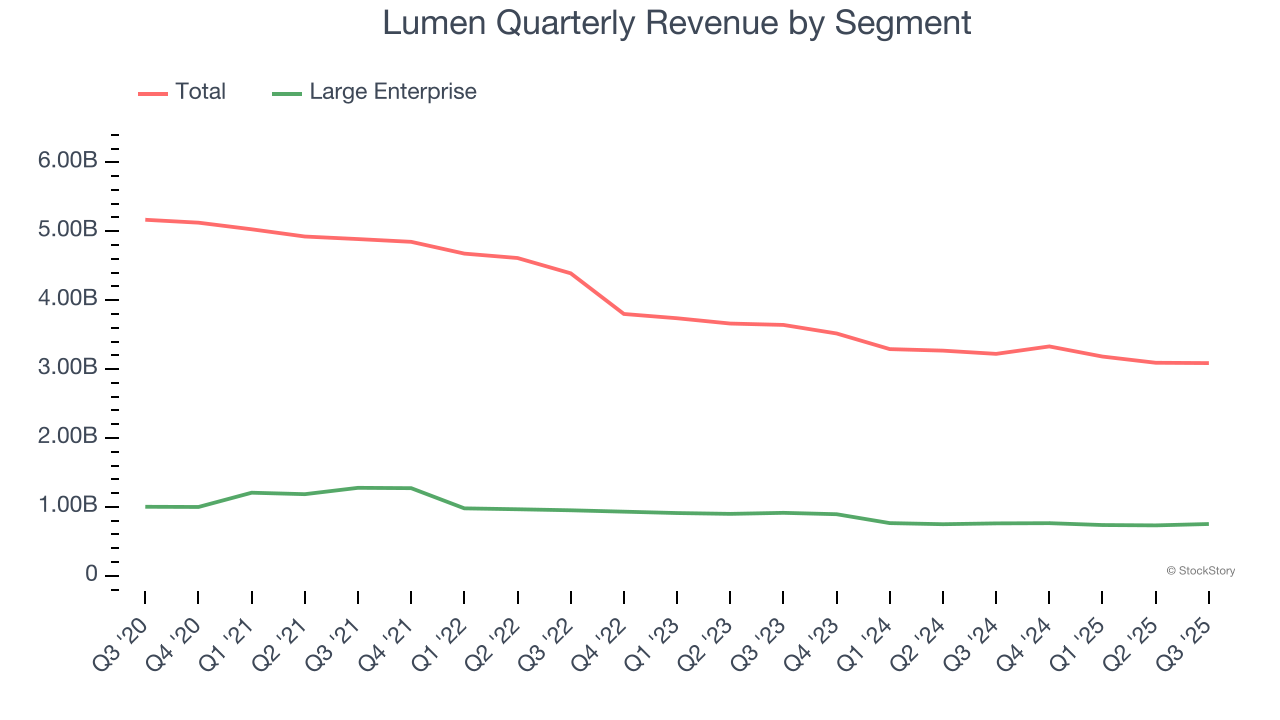

Lumen also breaks out the revenue for its most important segment, Large Enterprise. Over the last two years, Lumen’s Large Enterprise revenue (services provided to businesses) averaged 9.4% year-on-year declines. This segment has lagged the company’s overall sales.

This quarter, Lumen’s revenue fell by 4.2% year on year to $3.09 billion but beat Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to decline by 7% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not lead to better top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

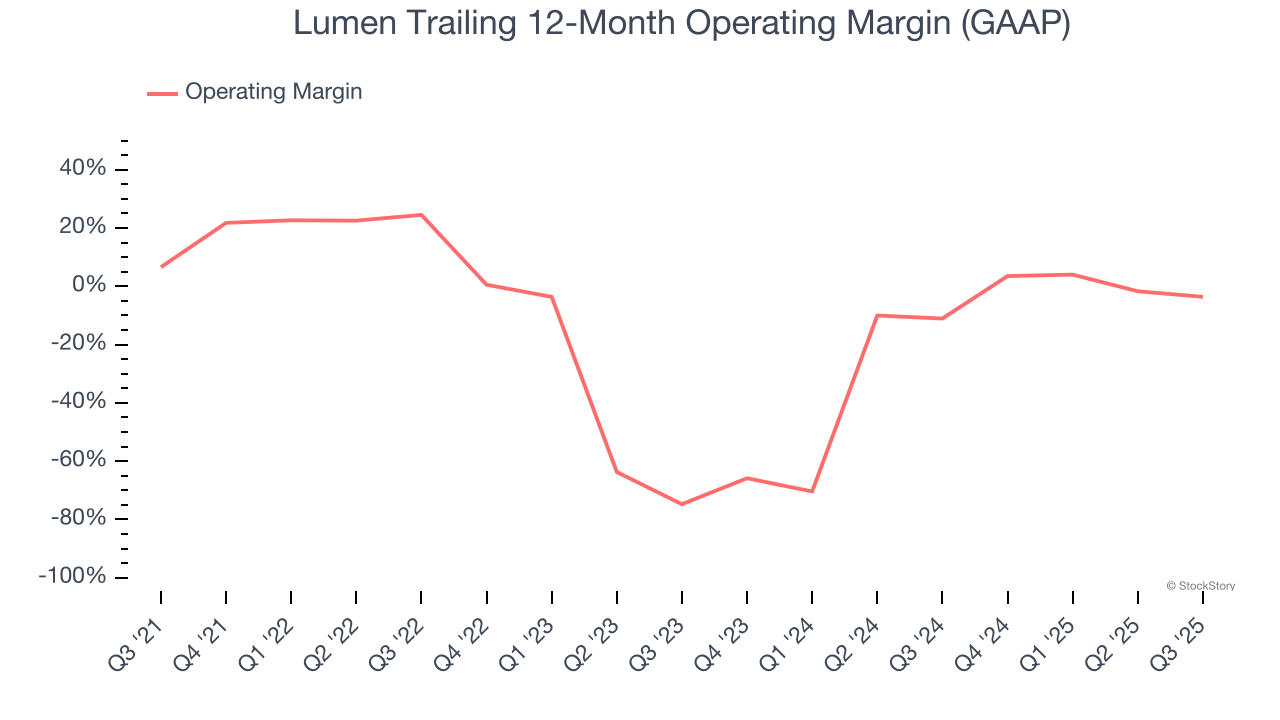

Lumen’s high expenses have contributed to an average operating margin of negative 9% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Lumen’s operating margin decreased by 10.2 percentage points over the last five years. Lumen’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q3, Lumen generated a negative 3.8% operating margin. The company's consistent lack of profits raise a flag.

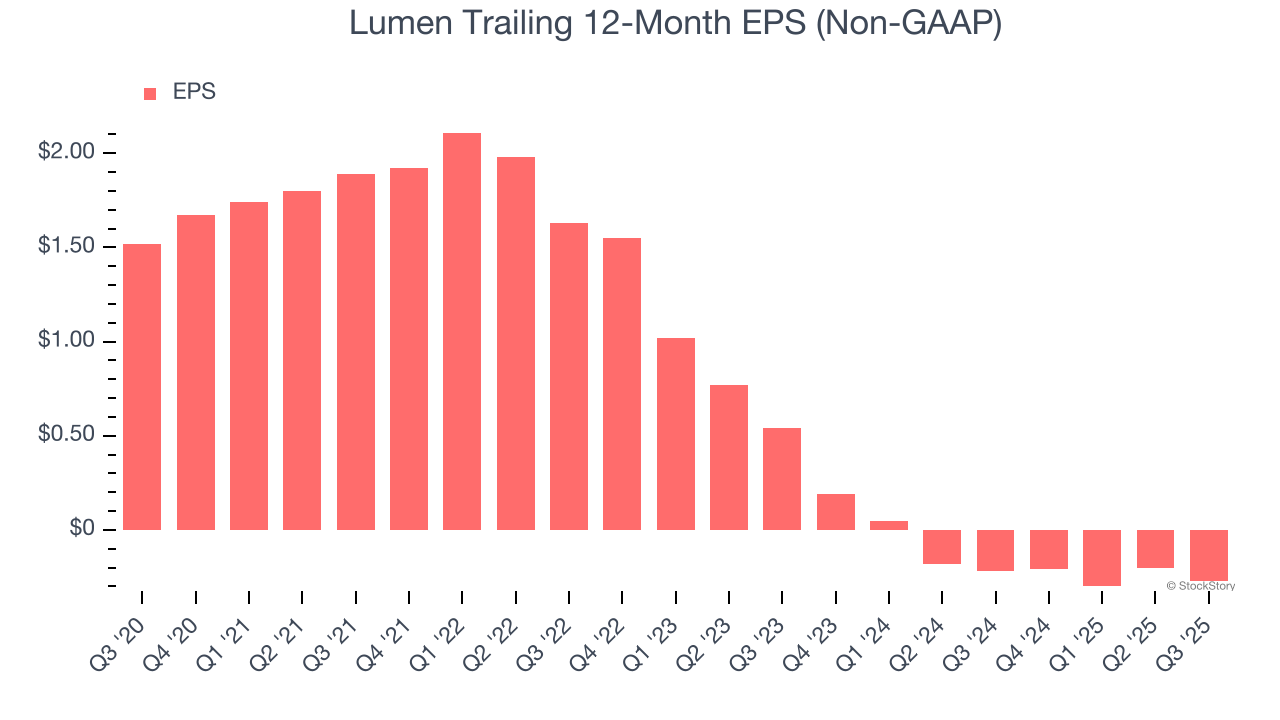

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Lumen, its EPS declined by 16.8% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

We can take a deeper look into Lumen’s earnings to better understand the drivers of its performance. As we mentioned earlier, Lumen’s operating margin declined by 10.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Lumen, its two-year annual EPS declines of 58.1% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Lumen reported adjusted EPS of negative $0.20, down from negative $0.13 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Lumen to perform poorly. Analysts forecast its full-year EPS of negative $0.27 will tumble to negative $0.87.

Key Takeaways from Lumen’s Q3 Results

It was good to see Lumen beat analysts’ revenue and EPS expectations this quarter. On the other hand, its EBITDA and full-year EBITDA guidance fell short of Wall Street’s estimates. Zooming out, we think this quarter was mixed but featured some positives. The stock traded up 6.1% to $10.97 immediately after reporting.

Lumen may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.