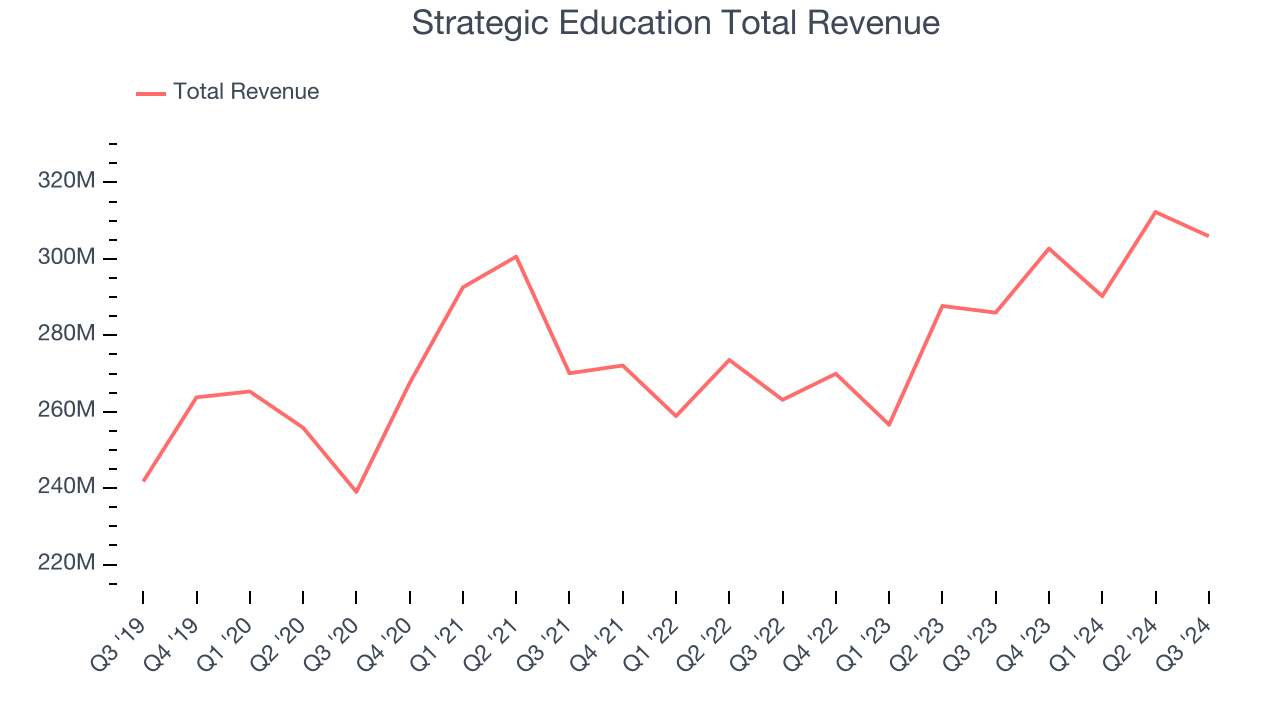

Higher education company Strategic Education (NASDAQ: STRA) announced better-than-expected revenue in Q3 CY2024, with sales up 7% year on year to $306 million. Its non-GAAP profit of $1.16 per share was also 44.4% above analysts’ consensus estimates.

Is now the time to buy Strategic Education? Find out by accessing our full research report, it’s free.

Strategic Education (STRA) Q3 CY2024 Highlights:

- Revenue: $306 million vs analyst estimates of $301.5 million (1.5% beat)

- Adjusted EPS: $1.16 vs analyst estimates of $0.80 (44.4% beat)

- EBITDA: $56.24 million vs analyst estimates of $45.07 million (24.8% beat)

- Gross Margin (GAAP): 46.8%, up from 45.5% in the same quarter last year

- Operating Margin: 11.9%, up from 9% in the same quarter last year

- EBITDA Margin: 18.4%, up from 17.3% in the same quarter last year

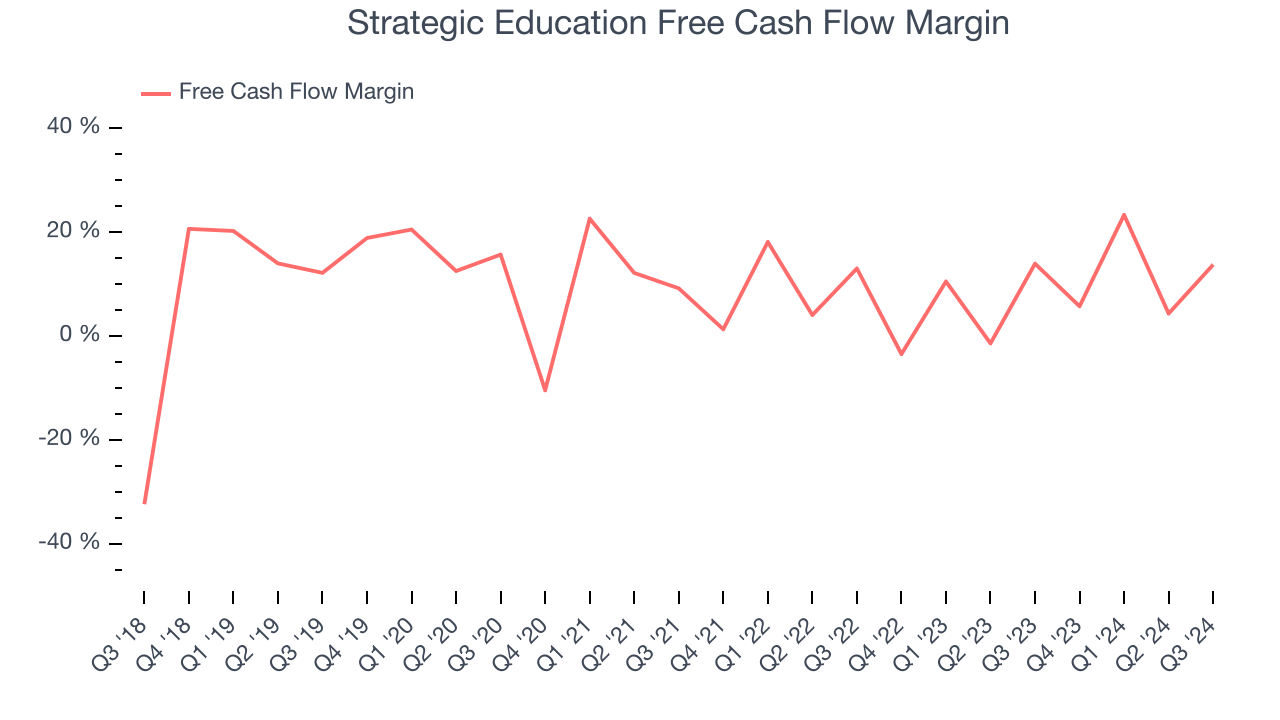

- Free Cash Flow Margin: 13.8%, similar to the same quarter last year

- Domestic Students: 86,533 at quarter end

- Market Capitalization: $2.35 billion

“Our third quarter results reflect continued growth across our business, including strong employer affiliated enrollment in the U.S. Higher Education segment; strong growth from Sophia subscriptions in the Education Technology Services segment; and another quarter of total enrollment growth in the Australia/New Zealand segment,” said Karl McDonnell, Chief Executive Officer of Strategic Education.

Company Overview

Formed through the merger of Strayer Education and Capella Education in 2018, Strategic Education (NASDAQ: STRA) is a career-focused higher education provider.

Education Services

A whole industry has emerged to address the problem of rising education costs, offering consumers alternatives to traditional education paths such as four-year colleges. These alternative paths, which may include online courses or flexible schedules, make education more accessible to those with work or child-rearing obligations. However, some have run into issues around the value of the degrees and certifications they provide and whether customers are getting a good deal. Those who don’t prove their value could struggle to retain students, or even worse, invite the heavy hand of regulation.

Sales Growth

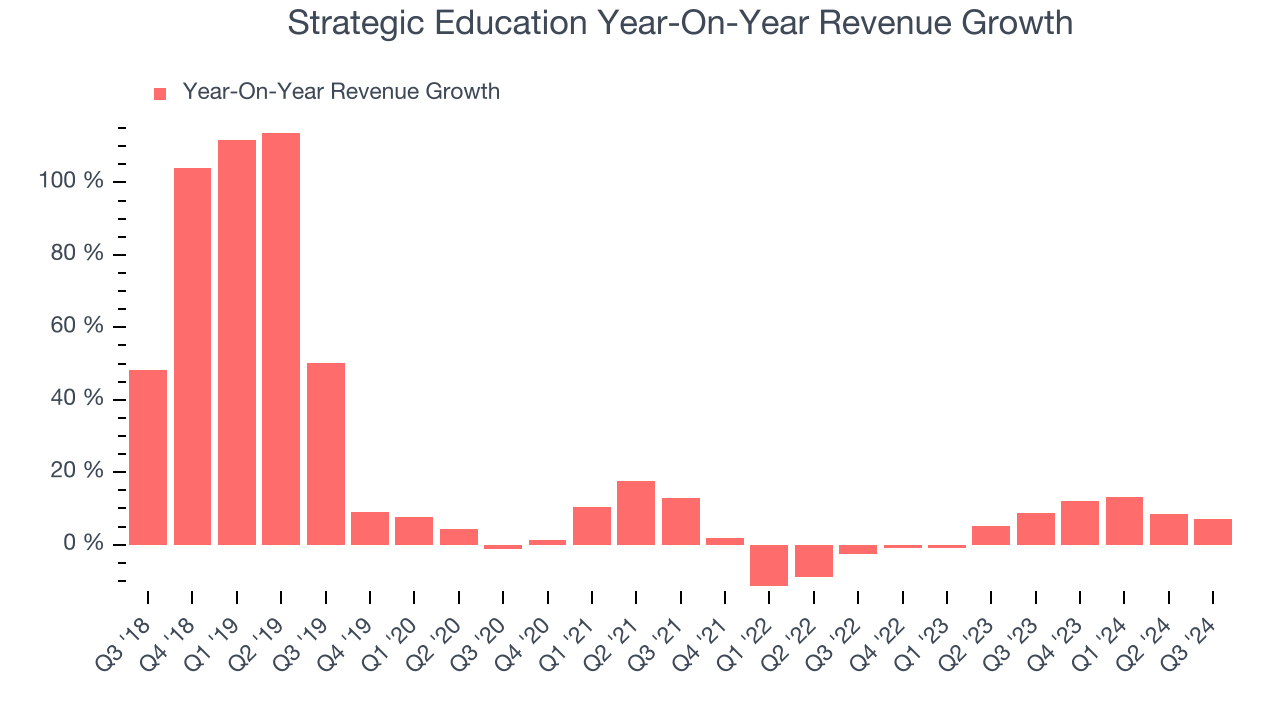

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Strategic Education grew its sales at a sluggish 4.4% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Strategic Education’s annualized revenue growth of 6.5% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Strategic Education reported year-on-year revenue growth of 7%, and its $306 million of revenue exceeded Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to grow 5.8% over the next 12 months, similar to its two-year rate. This projection is underwhelming and illustrates the market thinks its newer products and services will not lead to better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Strategic Education has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.4%, subpar for a consumer discretionary business.

Strategic Education’s free cash flow clocked in at $42.07 million in Q3, equivalent to a 13.8% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

Over the next year, analysts predict Strategic Education’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 11.6% for the last 12 months will decrease to 9.8%.

Key Takeaways from Strategic Education’s Q3 Results

We were impressed by how significantly Strategic Education blew past analysts’ revenue, EBITDA, and EPS expectations. Zooming out, we think this quarter featured some important positives. The stock traded up 3.7% to $100 immediately following the results.

Sure, Strategic Education had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.