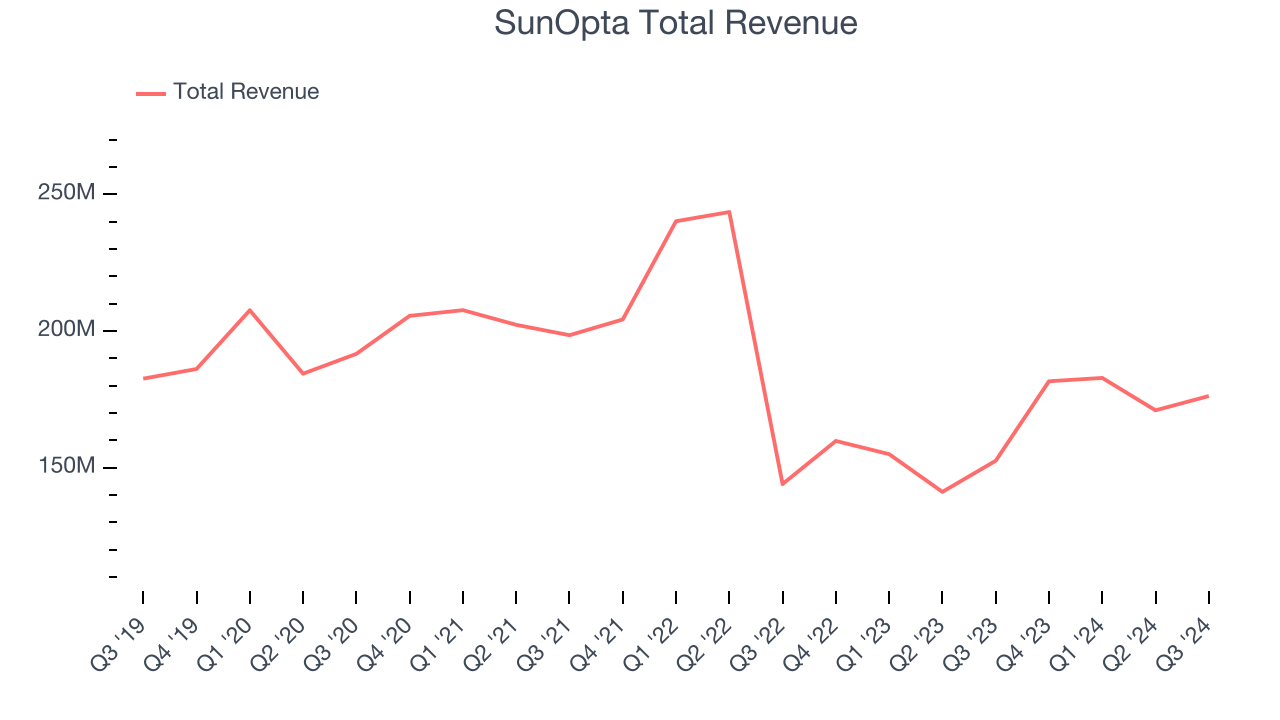

Plant-based food and beverage company SunOpta (NASDAQ: STKL) reported revenue ahead of Wall Street’s expectations in Q3 CY2024, with sales up 15.5% year on year to $176.2 million. The company expects the full year’s revenue to be around $720 million, close to analysts’ estimates. Its non-GAAP profit of $0.02 per share was 7.7% below analysts’ consensus estimates.

Is now the time to buy SunOpta? Find out by accessing our full research report, it’s free.

SunOpta (STKL) Q3 CY2024 Highlights:

- Revenue: $176.2 million vs analyst estimates of $173 million (1.8% beat)

- Adjusted EPS: $0.02 vs analyst expectations of $0.02 (7.7% miss)

- EBITDA: $21.5 million vs analyst estimates of $21.37 million (small beat)

- The company reconfirmed its revenue guidance for the full year of $720 million at the midpoint

- EBITDA guidance for the full year is $90 million at the midpoint, in line with analyst expectations

- Gross Margin (GAAP): 13.4%, down from 16.4% in the same quarter last year

- Operating Margin: 0.9%, in line with the same quarter last year

- EBITDA Margin: 12.2%, in line with the same quarter last year

- Free Cash Flow was $11.67 million, up from -$14.05 million in the same quarter last year

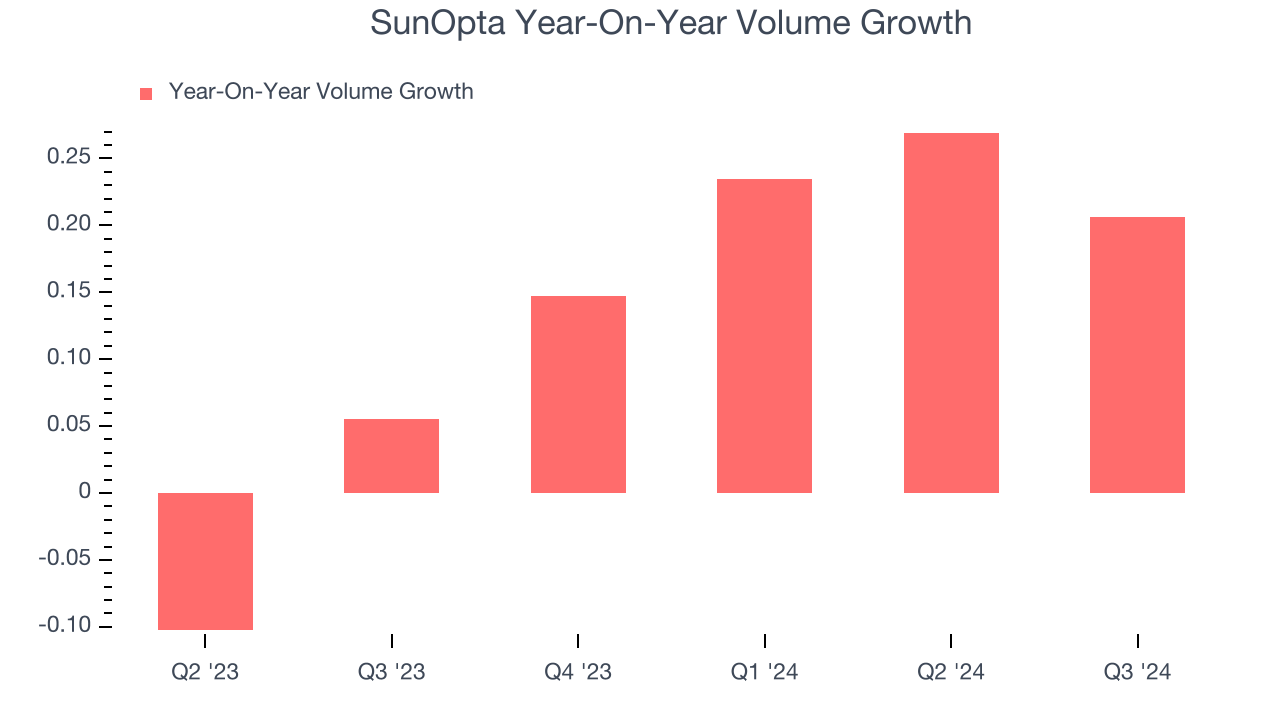

- Sales Volumes rose 20.6% year on year (5.5% in the same quarter last year)

- Market Capitalization: $806.3 million

“The third quarter unfolded as expected,” said Brian Kocher, Chief Executive Officer of SunOpta.

Company Overview

Committed to clean-label foods, SunOpta (NASDAQ: STKL) is a sustainability-focused food and beverage company specializing in the sourcing, processing, and packaging of natural and organic products.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years.

SunOpta is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from economies of scale.

As you can see below, SunOpta’s revenue declined by 4.4% per year over the last three years despite consumers buying more of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, SunOpta reported year-on-year revenue growth of 15.5%, and its $176.2 million of revenue exceeded Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 7.9% over the next 12 months, an acceleration versus the last three years. This projection is above average for the sector and shows the market thinks its newer products will catalyze higher growth rates.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

SunOpta’s average quarterly volume growth of 13.5% over the last two years has beaten the competition by a long shot. This is great because companies with significant volume growth are needles in a haystack in the stable consumer staples sector.

In SunOpta’s Q3 2024, sales volumes jumped 20.6% year on year. This result was an acceleration from the 5.5% year-on-year increase it posted 12 months ago, certainly a positive signal.

Key Takeaways from SunOpta’s Q3 Results

It was good to see SunOpta beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance came in higher than Wall Street’s estimates. On the other hand, its gross margin and EPS missed. Overall, this quarter was mixed. The stock traded up 2.5% to $6.96 immediately following the results.

Is SunOpta an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.