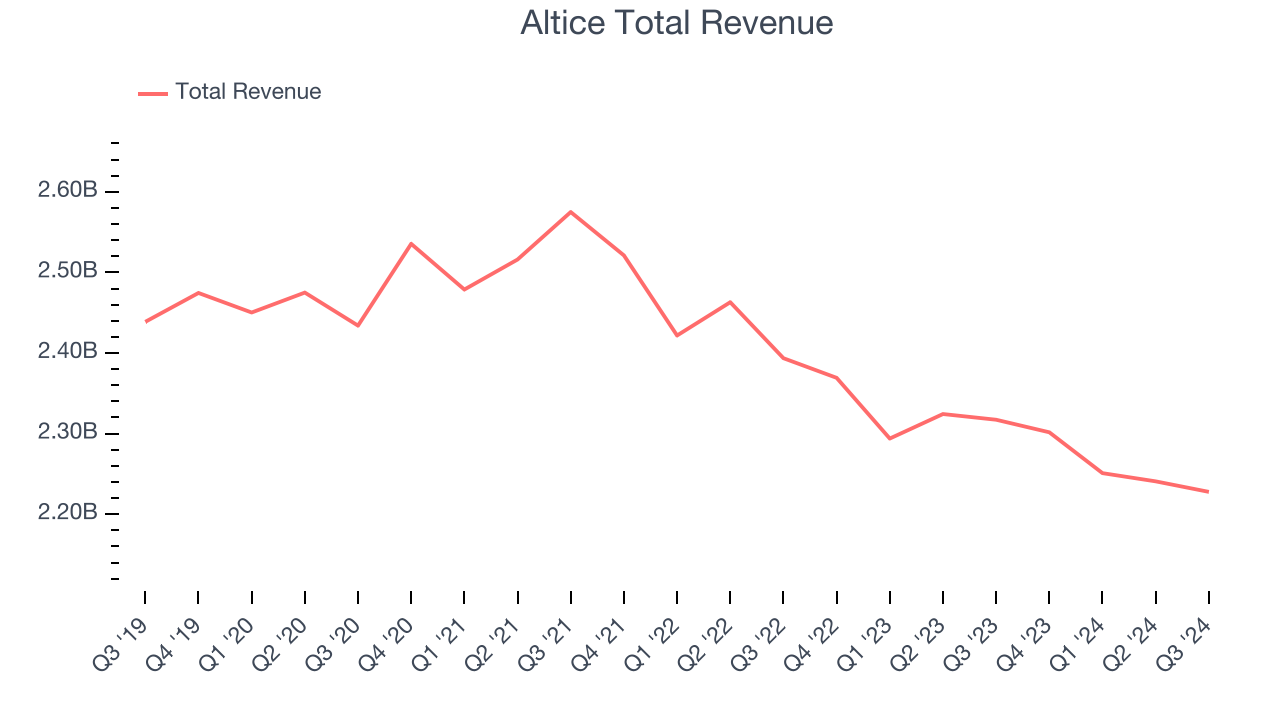

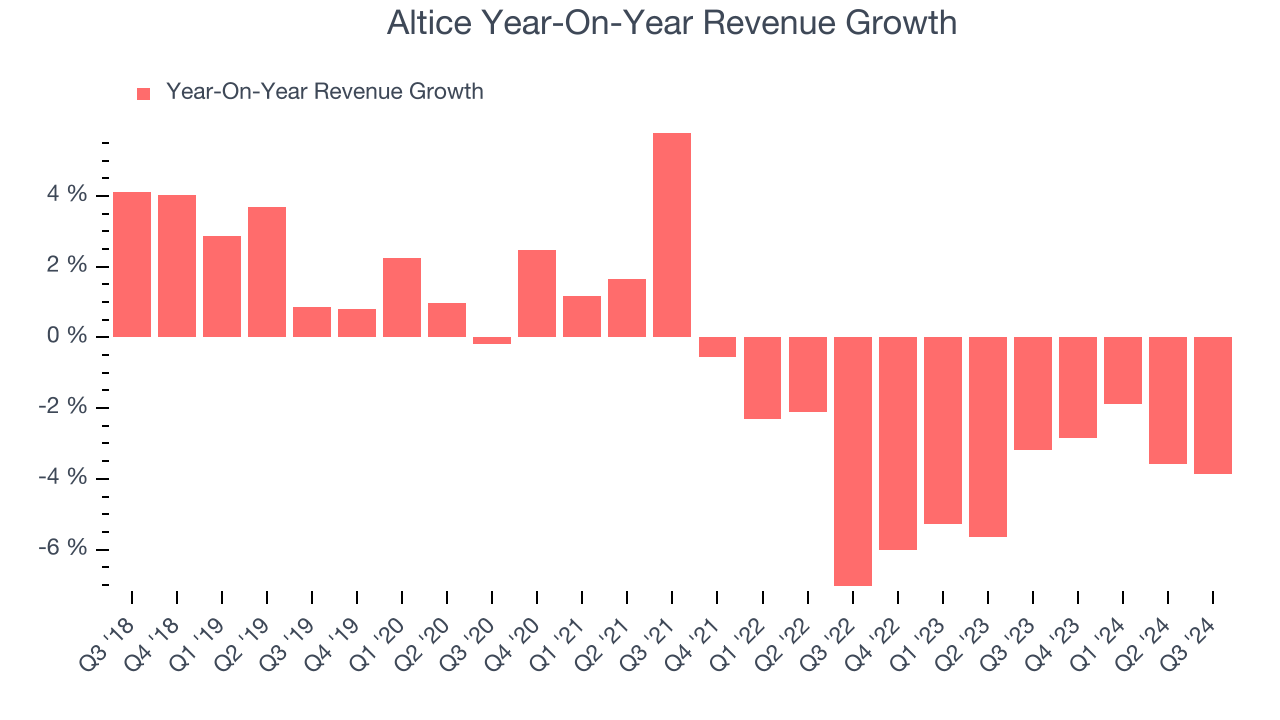

Telecommunications and cable services provider Altice USA (NYSE: ATUS) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 3.9% year on year to $2.23 billion. Its GAAP loss of $0.09 per share was 294% below analysts’ consensus estimates.

Is now the time to buy Altice? Find out by accessing our full research report, it’s free.

Altice (ATUS) Q3 CY2024 Highlights:

- Revenue: $2.23 billion vs analyst estimates of $2.24 billion (in line)

- EPS: -$0.09 vs analyst estimates of $0.05 (-$0.14 miss)

- EBITDA: $862 million vs analyst estimates of $873.8 million (1.4% miss)

- Gross Margin (GAAP): 68.1%, in line with the same quarter last year

- Operating Margin: 20%, down from 21.3% in the same quarter last year

- EBITDA Margin: 38.7%, in line with the same quarter last year

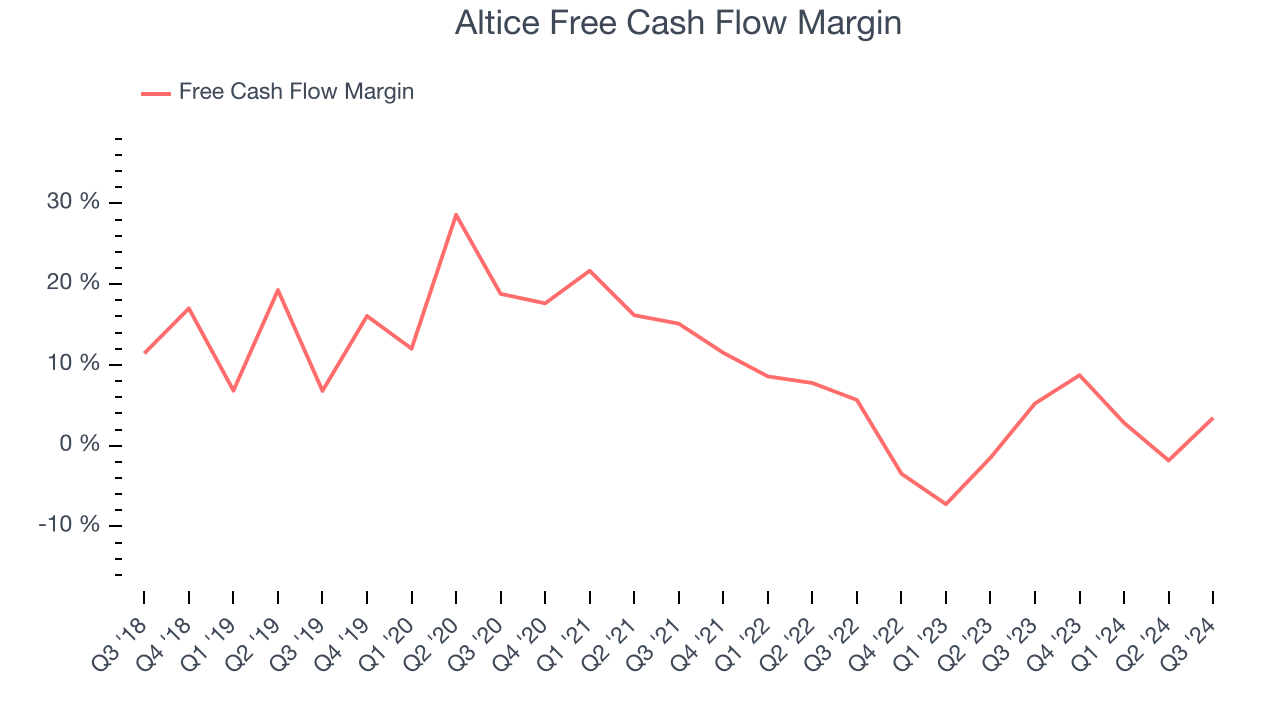

- Free Cash Flow Margin: 3.5%, down from 5.2% in the same quarter last year

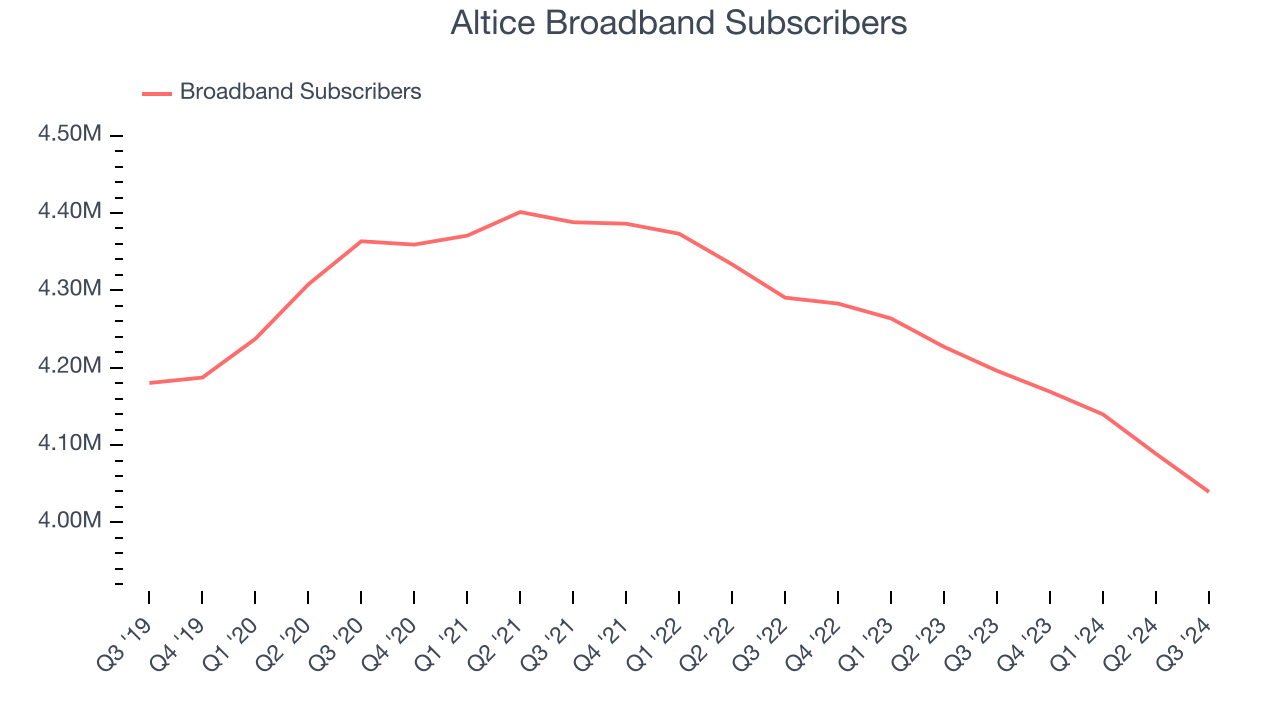

- Broadband Subscribers: 4.04 million, down 156,500 year on year

- Market Capitalization: $1.70 billion

Company Overview

Based in Long Island City, Altice USA (NYSE: ATUS) is a telecommunications company offering cable, internet, telephone, and television services across the United States.

Wireless, Cable and Satellite

The massive physical footprints of cell phone towers, fiber in the ground, or satellites in space make it challenging for companies in this industry to adjust to shifting consumer habits. Over the last decade-plus, consumers have ‘cut the cord’ to their landlines and traditional cable subscriptions in favor of wireless communications and streaming video. These trends do mean that more households need cell phone plans and high-speed internet. Companies that successfully serve customers can enjoy high retention rates and pricing power since the options for mobile and internet connectivity in any geography are usually limited.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last five years, Altice’s revenue declined by 1.5% per year. This shows demand was weak, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Altice’s recent history shows its demand has stayed suppressed as its revenue has declined by 4.1% annually over the last two years.

Altice also discloses its number of broadband subscribers and pay tv subscribers, which clocked in at 4.04 million and 1.94 million in the latest quarter. Over the last two years, Altice’s broadband subscribers averaged 2.8% year-on-year declines while its pay tv subscribers averaged 11.3% year-on-year declines.

This quarter, Altice reported a rather uninspiring 3.9% year-on-year revenue decline to $2.23 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline 2.8% over the next 12 months. Although this projection is better than its two-year trend it's tough to feel optimistic about a company facing demand difficulties.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Altice broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders. The divergence from its good operating margin stems from its capital-intensive business model, which requires Altice to make large cash investments in working capital and capital expenditures.

Altice’s free cash flow clocked in at $76.87 million in Q3, equivalent to a 3.5% margin. The company’s cash profitability regressed as it was 1.8 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

Key Takeaways from Altice’s Q3 Results

We struggled to find many strong positives in these results as its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 11.9% to $2.30 immediately following the results.

Altice underperformed this quarter, but does that create an opportunity to invest right now?When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.