Sao Paulo, Brazil – November 13, 2025 – The global coffee market is currently experiencing significant turbulence, with coffee futures on the rise due to a severe and prolonged drought in Brazil, the world's largest coffee producer. This climatic challenge, coupled with other market dynamics, is having immediate and far-reaching implications for global coffee prices, shaping a volatile and predominantly bullish market sentiment as of today. Consumers worldwide are already feeling the pinch, with the daily cup of coffee becoming an increasingly expensive indulgence, and the industry grappling with unprecedented strain.

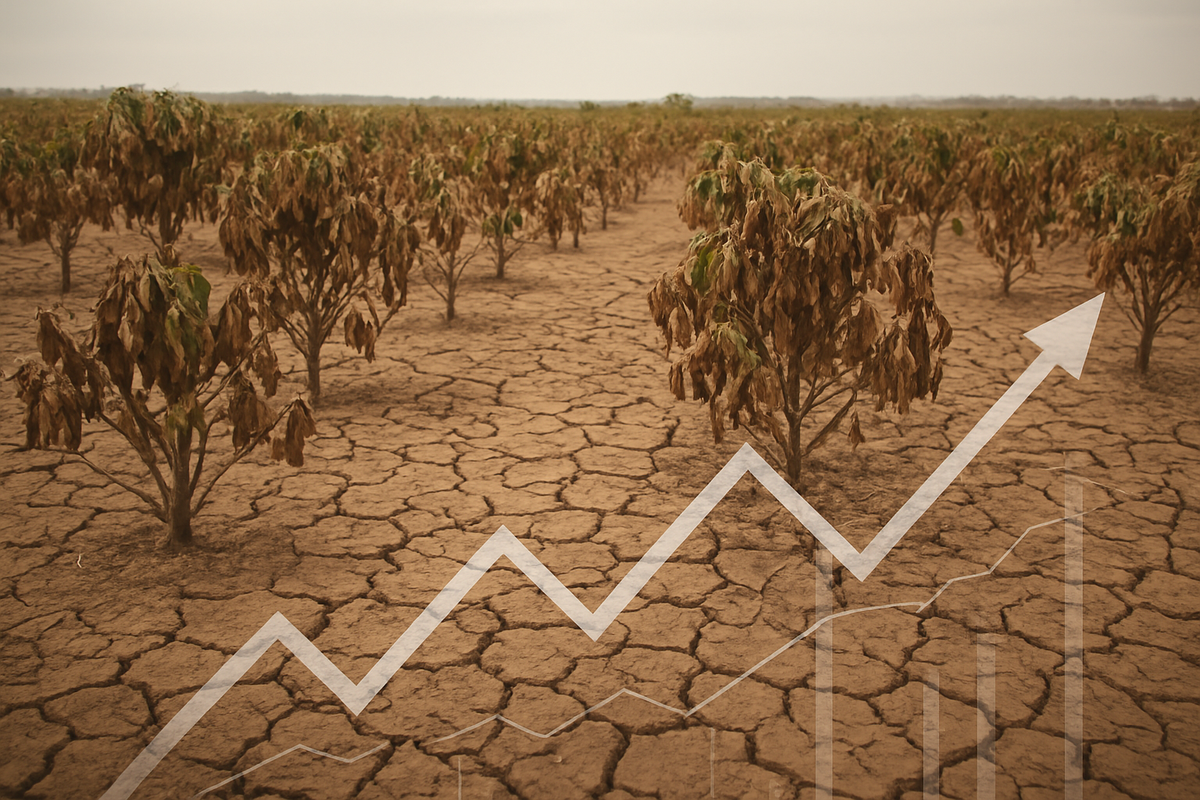

The persistent drought in Brazil's key coffee-growing regions, particularly Minas Gerais, has severely impacted crop yields and development, directly driving up coffee futures prices. Minas Gerais, the heart of Brazil's Arabica belt, has received significantly below-average rainfall, with reports indicating as little as 1% of normal rainfall in some critical weeks in late October 2025, threatening the flowering and bean development for the crucial 2026/27 crop. This climatic event is not an isolated incident but the latest in a series of weather-related disruptions that have plagued the region for several years.

Drought's Grip Tightens on Coffee Belt, Sending Prices Skyward

The impact of Brazil's drought has been swift and dramatic on the futures market. Arabica coffee futures have reached multi-month highs, with some reports indicating all-time highs of $4.36 per pound in November 2025, a level not seen since 1977. Robusta prices have also surged, more doubling compared to the previous year. This sharp rise is creating significant challenges for traders, especially those who hold short positions in futures markets to hedge risks. Brazilian trading firms like Atlantica Exportação e Importação SA and Cafebras Comércio de Cafés do Brasil SA have reportedly sought court-supervised debt restructuring as surging prices made hedging unmanageable and led to producer contract defaults. Many traders are closing out their short positions, inadvertently pushing prices even higher.

Supply shortfalls are a major concern. Brazil's crop agency, Conab, has cut its 2025 Arabica estimate by 4.9% to 35.2 million bags. Trading firm Volcafe projects a global Arabica deficit of 8.5 million bags for the 2025/26 season, marking the fifth consecutive year of undersupply. This situation is further complicated by 50% US tariffs on Brazilian coffee imports, which have contributed to record-low exchange inventories since 2024 and led American buyers to cancel new contracts for Brazilian beans, tightening supply in the US market. While global coffee production for 2025/26 is forecast to reach a record high of 178.7 million bags, this is primarily driven by an increase in Robusta output, while Arabica output is expected to fall. The rise in coffee futures is translating directly into higher global coffee prices across the supply chain. Retail prices have surged over 50% since August, leading major roasters like Nestlé S.A. (OTC: NSRGY) to announce price increases and even package size reductions. Consumers worldwide are experiencing coffee as an increasingly expensive indulgence, with some speculations that coffee could reach $12 per cup by the end of the year. The increased costs are hitting independent coffee shops and larger chains alike, with many struggling and some filing for bankruptcy due to elevated ingredient prices, rents, and labor costs. The World Bank's beverage price index surged 18% in December, reflecting the widespread impact of these price increases.

Brewing Winners and Losers: Corporate Fortunes in a Volatile Market

The surge in coffee futures creates a distinct divide between potential winners and losers across the global coffee supply chain. Companies in the coffee roasting and retailing sectors are generally expected to be the "losers" as they face higher raw material costs, which can squeeze margins or force them to raise consumer prices, potentially impacting demand.

Leading the list of those likely to be negatively impacted is Starbucks Corporation (NASDAQ: SBUX), the largest coffeehouse chain globally. While Starbucks utilizes futures contracts to hedge against price volatility, persistent high prices will undoubtedly pressure its profit margins. Management expects elevated coffee prices to pressure margins through at least the first half of fiscal 2026. Nestlé S.A. (OTC: NSRGY), the world's largest coffee company, has already implemented price hikes and reduced package sizes. The J.M. Smucker Co. (NYSE: SJM), owning brands like Folgers and Café Bustelo, sees coffee sales as approximately 32% of its total net sales, making it highly susceptible. Other significant players facing similar headwinds include Keurig Dr Pepper Inc. (NASDAQ: KDP), JDE Peet's N.V. (Euronext Amsterdam: JDEP), Dutch Bros Inc. (NYSE: BROS), Restaurant Brands International Inc. (NYSE: QSR) through its Tim Hortons brand, and Black Rock Coffee Bar, Inc. (NASDAQ: BRCB), which recently reported a quarterly loss despite revenue growth.

Identifying direct "winners" among publicly traded pure-play coffee producers is more challenging, as many are private or diversified agricultural businesses. However, agricultural companies with significant coffee operations in regions unaffected by the Brazilian drought, able to sell their unaffected harvests at higher global prices, could see increased revenues. Indirectly, companies like Breville Group Ltd (ASX: BRG), known for premium at-home coffee machines, may benefit. As cafe prices increase, consumers might shift towards brewing coffee at home to save costs, driving demand for Breville's products.

A Wider Significance: Climate, Policy, and Historical Echoes

The current surge in coffee futures due to Brazil's drought signifies a critical juncture for the global coffee industry, extending far beyond simple price fluctuations. This event is not an isolated incident but rather a symptom of deeper, interconnected trends, with profound ripple effects on all stakeholders and potential regulatory responses.

This situation fits into several broader industry trends, with climate change being the most prominent. The Brazilian drought is a clear indicator of climate change's intensifying impact on agriculture, leading to more frequent and severe extreme weather events globally. This drives a shift in production dynamics, with some farmers, particularly in Brazil, increasingly cultivating the more resilient Robusta beans (conilon) over Arabica. Despite supply challenges, global coffee consumption continues to rise, especially for premium and specialty varieties, further straining limited supplies. This crisis also underscores the urgency for sustainable and ethical sourcing, as consumers increasingly seek environmentally responsible brands. The surge has a cascading effect throughout the supply chain; roasters and cafe operators face difficult choices between absorbing costs or passing them to consumers, while other coffee-producing countries, if stable, could see increased demand. Regulatory bodies are also responding. The EU Deforestation Regulation (EUDR), effective at the end of 2024, adds compliance costs and necessitates enhanced traceability. Trade policies, such as the US's 50% tariff on Brazilian coffee, further complicate global trade dynamics.

The current situation draws comparisons to several significant historical events in the coffee market. The most frequently cited precedent is the 1977 Brazilian Frost, which decimated plantations and caused Arabica prices to surge to levels (adjusted for inflation, a staggering $17.68 per pound today) not seen since. Other weather-related declines in 1975 and 1985 also triggered price spikes. The dissolution of the International Coffee Agreement in 1989 led to a dramatic plummet in prices, demonstrating the impact of policy shifts. More recently, a severe drought in Brazil in May 2021, followed by a frost in July 2021, wiped out about 20% of the Arabica crop, causing significant price increases between 2021 and 2024, showing a pattern of increasing climate-driven supply shocks. As of November 13, 2025, world coffee stocks are at a 25-year low, making the market extremely sensitive to any further disruptions.

What Comes Next: Navigating a Volatile Future

The global coffee market is at a critical juncture, facing continued uncertainty and elevated prices in the short term. Consumers can expect to face higher prices at coffee shops and grocery stores as roasters and retailers pass on increased costs. Global coffee supplies will likely remain tight due to the lingering effects of droughts in Brazil and Vietnam, impacting the 2025/26 crop cycle. This may lead to shifts in consumer behavior, with some reducing consumption or switching to more affordable alternatives. Roasters will likely intensify efforts to diversify their sourcing away from heavily impacted regions.

The long-term outlook is fundamentally shaped by climate change, necessitating profound adaptations. Rising temperatures and unpredictable weather are projected to shrink suitable land for coffee cultivation by as much as half by 2050, particularly for vulnerable Arabica. This also increases the proliferation of pests and diseases, and threatens the extinction of wild coffee species. Strategic pivots are essential, including investing in climate-resilient cultivation with drought-resistant varieties, widespread adoption of sustainable farming practices like agroforestry, and robust supply chain diversification. Technological innovation in processing and brewing, alongside fairer trade practices, will also be crucial.

Market opportunities include the explosive growth of the specialty coffee segment, especially in emerging markets, and product innovation in brewing methods and flavors. The ready-to-drink (RTD) coffee segment also shows strong growth. However, significant challenges remain, including the unpredictable nature of climate change, persistent price volatility, fragile supply chains, rising production costs for farmers, and balancing these costs with consumer affordability.

Potential scenarios range from a worst-case where unmitigated climate crisis leads to a dramatic decrease in global supply, making coffee a luxury commodity, to a best-case where widespread sustainable transformation ensures access to diverse, high-quality, and ethically produced coffees. The most likely scenario involves an adaptive and bifurcated market, with a thriving high-end specialty segment and a mass market increasingly relying on more resilient Robusta varieties or blended products, alongside significant investments in climate-resilient farming and technological innovations.

A Bitter Brew or a Sustainable Future: The Coffee Market's Crossroads

In summary, the recent surge in coffee futures, primarily driven by Brazil's devastating drought, is not merely a transient price spike but a profound indicator of fundamental shifts in the global coffee landscape. The key takeaways from this turbulent period include critically low global inventories, significant financial strain on traders and roasters, and a clear signal that climate change is the most significant long-term threat to coffee production. This reality is forcing the industry to adapt, with increased emphasis on sustainable and ethical sourcing, as well as the development of climate-resilient coffee varieties.

Moving forward, the market is expected to remain highly volatile. While some forecasts cautiously project price relief in the latter half of 2025 and into 2026, contingent on weather stabilization and stock replenishment, the road ahead remains uncertain. For stakeholders across the value chain, the implications are profound. Smallholder farmers face heightened vulnerability, while roasters grapple with higher green bean prices, leading to strategic shifts towards diversifying blends and sourcing from less expensive origins, costs ultimately passed on to consumers. Technological innovations, such as predictive analytics and AI, are gaining traction as essential tools for enhancing supply chain resilience.

Investors in the coffee sector should remain vigilant and adopt a strategic approach in the coming months. It is crucial to monitor weather reports closely from major coffee-producing nations, track geopolitical and trade developments (especially the U.S. tariffs on Brazilian coffee), and keep a close eye on ICE-certified Arabica and Robusta stock levels. Additionally, currency fluctuations of the Brazilian real and the performance of the specialty coffee segment will be key indicators. While short-term volatility offers trading opportunities, the underlying long-term trend appears bullish due to climate change and rising demand. The coffee market is currently navigating a "perfect storm" of challenges, and investors must stay informed and agile to navigate what promises to be a continuously evolving and high-stakes market.

This content is intended for informational purposes only and is not financial advice