Airline stocks are hurting badly as the Iran overhaul has pushed crude oil prices near the $100/barrel mark. Last week, we were already experiencing the high costs of fuel and travel disruptions caused by U.S. carriers. On March 12, the price of oil rose 7% following tanker attacks in the Red Sea, which led to declines in airline stocks. American Airlines Group (AAL) and its competitors plummeted ahead of Thursday's trading, raising concerns about another turbulent period. Such issues contributed to the airline's vulnerability in the recent past: most U.S. airlines reduced capacity and raised fares late in 2025, thereby straining demand. Today, brokerages fear profit squeezes as the Iran tensions and increased oil prices are on the rise.

In this scenario, where AAL is facing high short interest, according to the latest data, approximately 7.7% of its float, traders are questioning: could there be a short squeeze in case the stock turns around as the price of fuel returns to normal? It preconditions a pullback in a bearish mood against any rally driver.

About American Airlines Stock

American Airlines is one of the world’s largest carriers, flying 6,000+ daily flights to 350+ destinations. It operates a broad domestic and international network. The airline prioritizes premium service, loyalty programs, and network expansion.

In 2026, American is adding dozens of new routes, e.g., LAX-Cleveland, ORD-Hawaii, and premium cabins. The carrier has a workforce of 130,000 and focuses on innovation in customer experience. As fuel costs and global events affect demand, AAL’s strategy emphasizes a mix of revenue management and cost control.

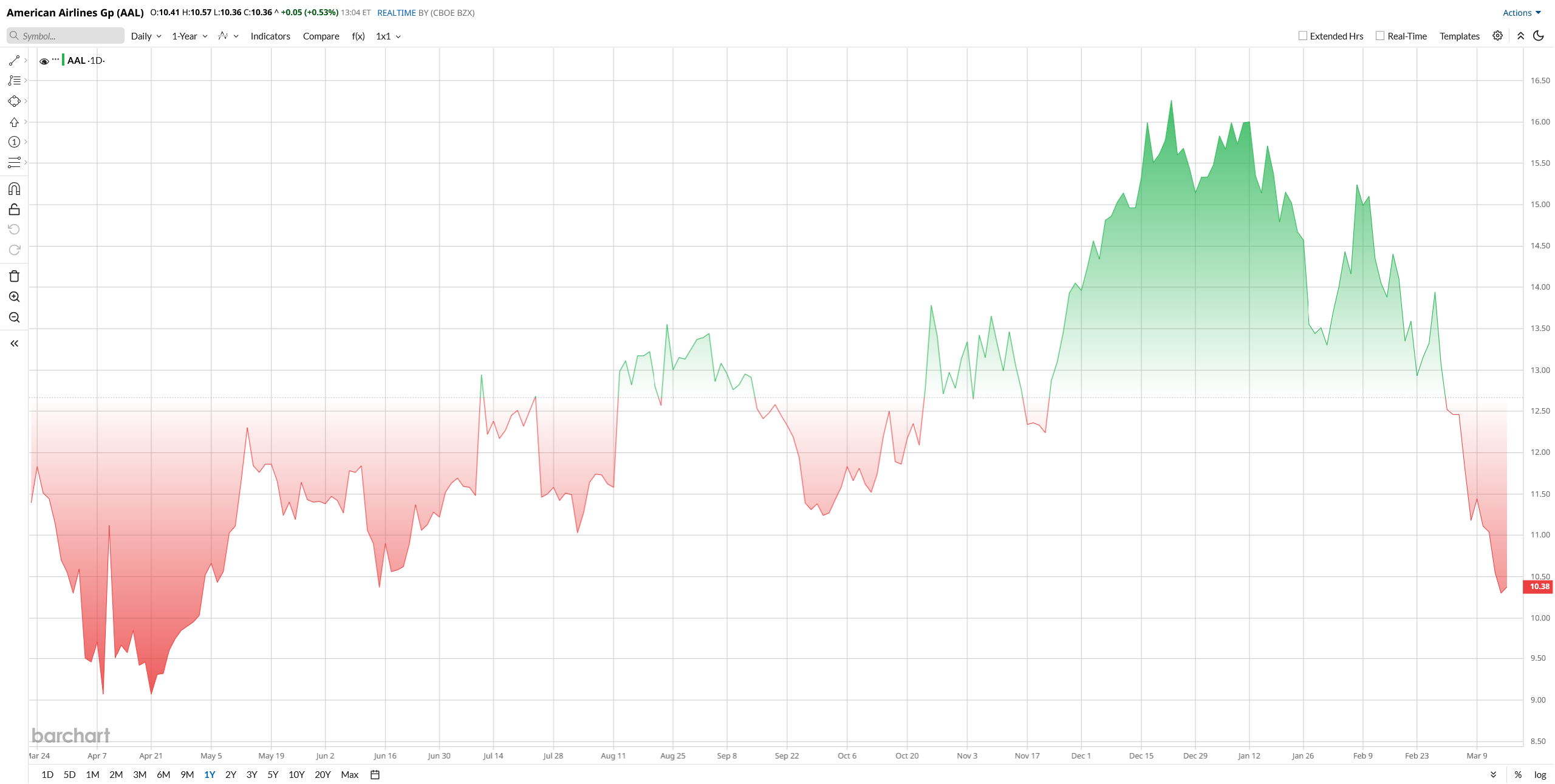

AAL stock has been battered over the past 12 months. Its 52-week range spans roughly between $8.50 and $17.50, and shares are down 32% year-to-date (YTD). The slide stems from skyrocketing jet fuel peaking around $4.50/gal and wary investors trimming airline exposure amid geopolitical jitters. Strong travel demand in 2024 had lifted airline profits, but as oil surged from $70 to $119 in recent weeks, carriers’ margins came under siege.

After the selloff, AAL’s valuation looks historically cheap. Its forward P/E is only 5×, one of the lowest in the S&P 500, compared to the sector median of around 19×. AAL’s EV/EBITDA is roughly 9×, versus 14× for stronger airlines. So it means the stock is deeply discounted and could be an opportunity to buy the current dip at low prices.

Iran War Impact and Short-Interest News

So the news broke that nearly 7.7% of AAL’s float was sold short by mid-February, well above the typical level for a major airline. Traders have noted that if AAL shares rally, these shorts could rush to cover. The Iran war context intensified this dynamic: oil’s surge on Middle East tensions hammered AAL down 8% in one session, yet some speculators see it as a contrarian opportunity.

Analysts warn that prolonged high fuel prices would squeeze airline profits. However, a rebound catalyst, such as de-escalation or stabilizing fuel, could spark a quick squeeze. So far, investor reaction to the news has been mixed. Retail buzz suggests some are positioning for a bounce, but hedge funds remain cautious; for now, the stock’s drop has mostly reflected fear, not forced short squeezes. If oil retreats or demand surprises, the high short interest means any sudden buying could be amplified, adding upside to the recovery.

AAL Misses Q4 Estimates as Fuel Costs Surge

America’s Q4 showed some major ongoing challenges. The airline reported $13.99 billion in revenue for Q4, roughly flat year-over-year (YoY), slightly below the consensus of $14.0 billion. The full-year 2025 total was a record $54.6 billion, but the quarter lagged forecasts due to the U.S. government shutdown dampening travel and cargo revenue by about $325 million.

Profitability took a major hit. The company reported EPS of $0.16 in Q4, a sharp miss from the $0.38 consensus. Jet fuel cost was about $3.15 billion in the quarter, rising 40% YoY. American ended 2025 with $9.95 per share in cash, roughly $6.4 billion total, and 70% institutional ownership, giving it a runway despite losses. Free cash flow guidance is modest yet; AA expects to remain near breakeven in early 2026.

The earnings call highlighted cost controls and outlook. CEO Robert Isom emphasized premium offerings and loyalty: “We’re a premium global airline,” he said, and noted improvements to the AAdvantage program. The company also signaled cautious optimism. For 2026, American sees EPS in the $1.70 to $2.70 range, implying a rebound as oil moderates. It expects capacity to grow 3 to 5% in Q1 2026 with revenue growth of 7 to 10% from the prior year.

Notably, management has targeted net debt below $35 billion by the end of 2026 and projected free cash flow exceeding $2 billion. No traditional guidance was given beyond these ranges, but analysts at TD Cowen note the guidance implies 2026 EPS around $2.15. For Q1 2026, consensus estimates call for roughly $12.5 billion in revenue and a loss of $0.32 EPS.

Analysts’ Take and Price Targets

Wall Street analysts are usually split on AAL’s path but lean towards being more bullish. J.P. Morgan’s Jamie Baker maintains an “Overweight” rating, raising his 12-month price target to $22 from $20, citing strong demand forecasts and fuel hedges.

Similarly, Susquehanna upgraded its view to “Positive” and lifted its target to $20, highlighting the potential upside as oil normalizes. TD Cowen continues to rate AA as a “Buy” with a $19 target, up from $16, noting that the selloff already prices in much pain.

On the bearish side, Rothschild/Redburn just cut their stance to “Neutral” with a $12.50 target, warning that higher fuel costs and a modest outlook may keep profits muted.

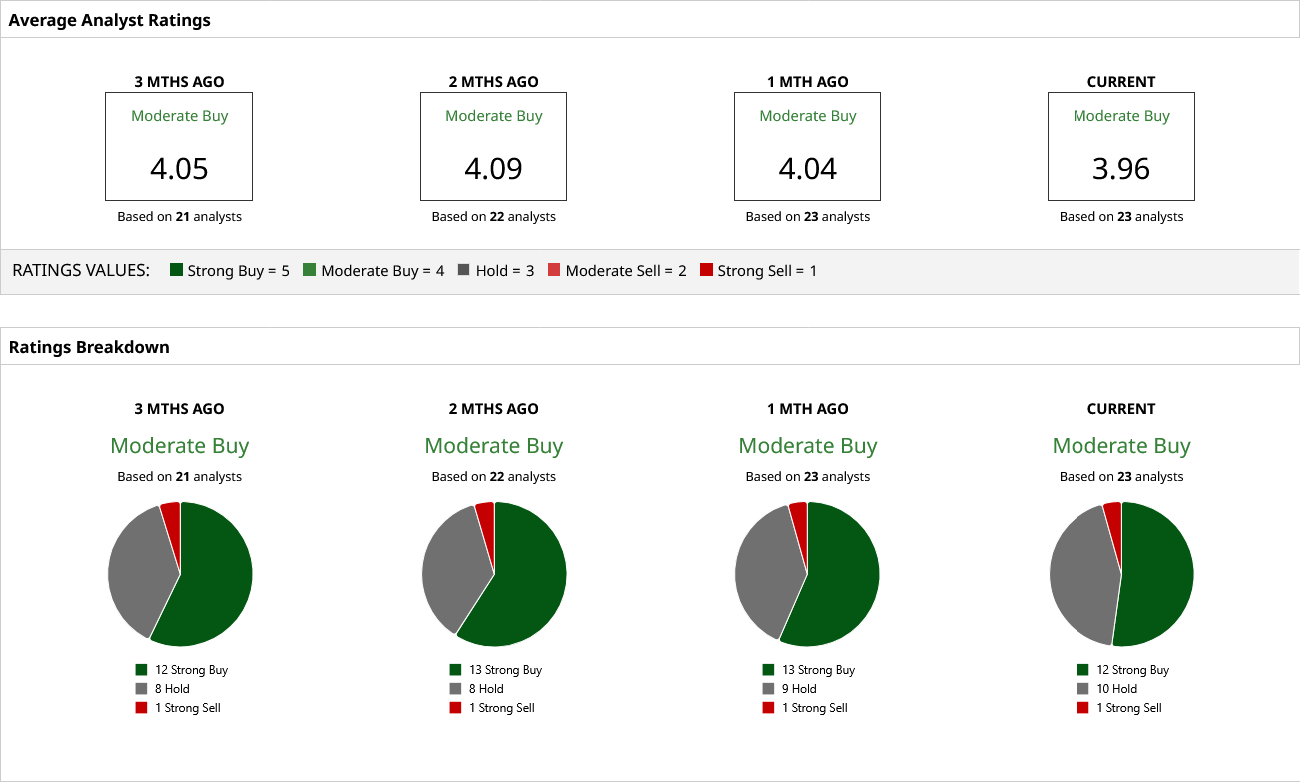

Overall, the consensus among 23 analysts is “Moderate Buy,” and the average analyst target sits around $17, which gives more than 70% upside premium. But here is the case: if oil stays elevated, airlines will underperform, also warned an analyst at one major bank. However, AA’s premium strategy, as Isom put it, could capture more revenue in recovery.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart