Artificial intelligence (AI) is advancing at breakneck speed, and its rapid evolution is starting to shake the foundations of several legacy business models across software, cybersecurity, and the broader tech landscape. In recent weeks, global cybersecurity and software stocks have pulled back sharply as investors worry that AI-driven disruption could erode traditional revenue streams. FactSet Research Systems (FDS), the well-known financial data provider, has also felt the heat.

While the company remains profitable, it has been facing real challenges over the past year. Competition from AI-powered subscription alternatives is intensifying, and many of its core asset management clients are tightening budgets. As concerns mounted that AI could make financial data cheaper and easier to access elsewhere, FactSet’s shares slid to multi-year lows in early 2026. Investors worried the company might have to spend heavily on new technology to remain competitive.

However, a fresh dose of optimism presents itself for FDS investors. On Feb. 24, FactSet shares surged nearly 6% after news broke that a new tool enables users to bring financial market data from FactSet’s platform directly into Anthropic’s AI model, Claude. The integration was unveiled as part of a broader announcement from Anthropic and signaled that FactSet’s extensive financial database could play a critical role in powering next-generation AI applications.

The rebound provided a much-needed lift to shares that had been down sharply for the year. So, with this latest development in play, should investors seize the dip in FactSet, or wait for clearer signs that the AI-driven headwinds are turning into long-term tailwinds?

About FactSet Stock

FactSet has built its reputation on delivering the data and analytics that power decision-making across global financial markets. The company provides enterprise-level financial data and information solutions through a digital platform that combines its proprietary datasets with client data, third-party sources, and flexible technology tools. The Connecticut-based company’s services span the buy-side, sell-side, wealth management, private equity, and corporate sectors, helping firms manage research, portfolio analysis, and reporting in one integrated ecosystem.

With more than 47 years in the industry, offices across 19 countries, and broad multi-asset class coverage, FactSet has steadily evolved by incorporating advanced data connectivity, AI, and next-generation workflow tools. Today, the company serves over 9,000 institutional clients and more than 239,000 individual users worldwide, positioning itself as a key infrastructure provider in the global financial information landscape.

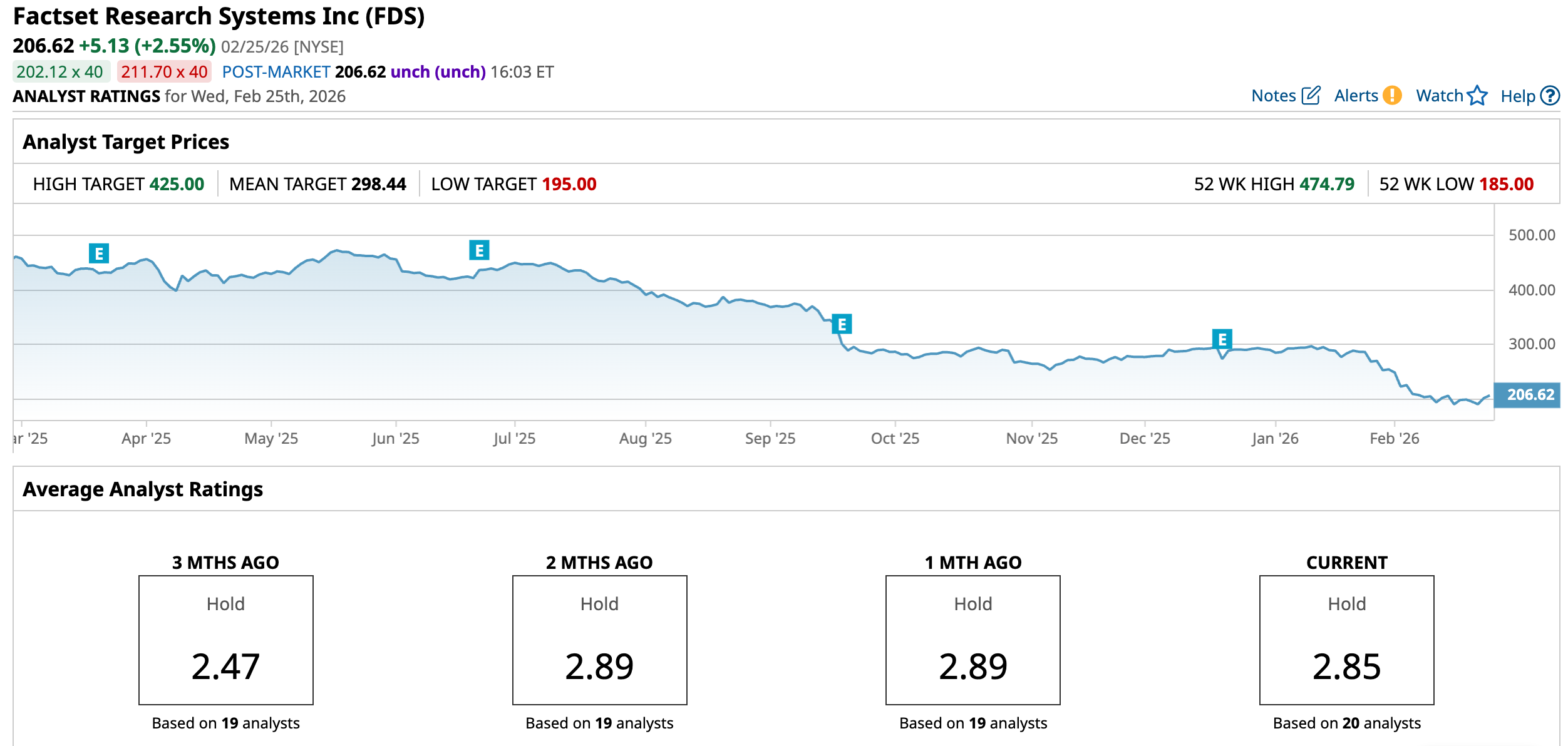

However, amid company-specific risks, broader industry headwinds, and the looming threat of AI disrupting FactSet’s traditional business model, the stock’s performance has been anything but impressive. Now carrying a market capitalization of roughly $7.5 billion, the financial data provider has seen its shares tumble nearly 55.36% in the past 52 weeks, followed by another steep 28.78% drop in 2026 alone. That’s a stark contrast to the broader market.

The S&P 500 Index ($SPX) surged about 16.67% in 2025 and has inched higher again this year by 1.5%. While the broader market has pushed to new gains, FactSet has been stuck in reverse, underscoring the degree of caution investors hold about its growth trajectory in an AI-driven world. In fact, after climbing to a year-to-date (YTD) high of $300.63 on Jan. 12, FactSet’s stock has since tumbled roughly 31.3% from that peak.

Although FactSet’s stock has struggled, it continues to return capital to shareholders. On Feb. 5, the company announced a quarterly dividend of $1.10 per share, payable on Mar. 19. That equates to a forward annualized dividend of $4.40 per share, offering a solid 2.31% yield, a meaningful cushion for investors during a volatile stretch. Valuation adds another layer to the story.

FactSet is currently trading at just 10.94 times forward earnings and 3.05 times forward sales, a sharp discount to its own five-year averages of 27.58x and 7.92x, respectively. In other words, while sentiment remains weak, the stock is now priced well below its historical norms, potentially setting the stage for value-focused investors to take notice.

Inside FactSet’s Q1 Performance

While FactSet’s shares have been under pressure, its underlying business performance tells a more resilient story. On Dec. 18, the company reported fiscal 2026 first-quarter results that comfortably beat Wall Street’s expectations on both the top and bottom lines. Revenue rose 6.9% year-over-year (YOY) to $607.6 million, ahead of the Street’s $599.5 million estimate. Organic revenue climbed 6% to $600 million, driven primarily by strength among institutional buy-side and dealmaker clients.

Regionally, growth was broad-based. Revenue from the Americas reached $396.2 million, up 7.9% from the prior year. The EMEA segment generated $149.5 million, reflecting 4% growth, while Asia Pacific contributed $61.9 million, marking a solid 7.3% increase. A closely watched metric, Annual Subscription Value (ASV), which represents forward-looking revenue for the next 12 months from all active subscription services, also improved.

ASV stood at $2.41 billion as of Nov. 30, 2025, compared with $2.27 billion a year earlier. FactSet added seven clients in the quarter, mainly from corporate and wealth management segments, bringing its total client base to 9,003. And, the company maintained a healthy 91% annual client retention rate. On the bottom line, adjusted EPS came in at $4.51, up 3.2% YOY and ahead of analysts’ estimates of $4.39.

FactSet ended the quarter with $275.5 million in cash and cash equivalents, compared with $337.7 million at the end of fiscal 2025’s fourth quarter. Long-term debt stood at $1.4 billion, unchanged from the previous quarter. During the period, the company generated $121.3 million in operating cash flow, while capital expenditures totaled $30.8 million.

Looking ahead, management expects fiscal 2026 revenue to land between $2.423 billion and $2.448 billion. Adjusted EPS is projected in the range of $16.90 to $17.60. Meanwhile, organic ASV growth is forecast to increase by $100 million to $150 million over the course of fiscal 2026.

How Are Analysts Viewing FactSet Stock?

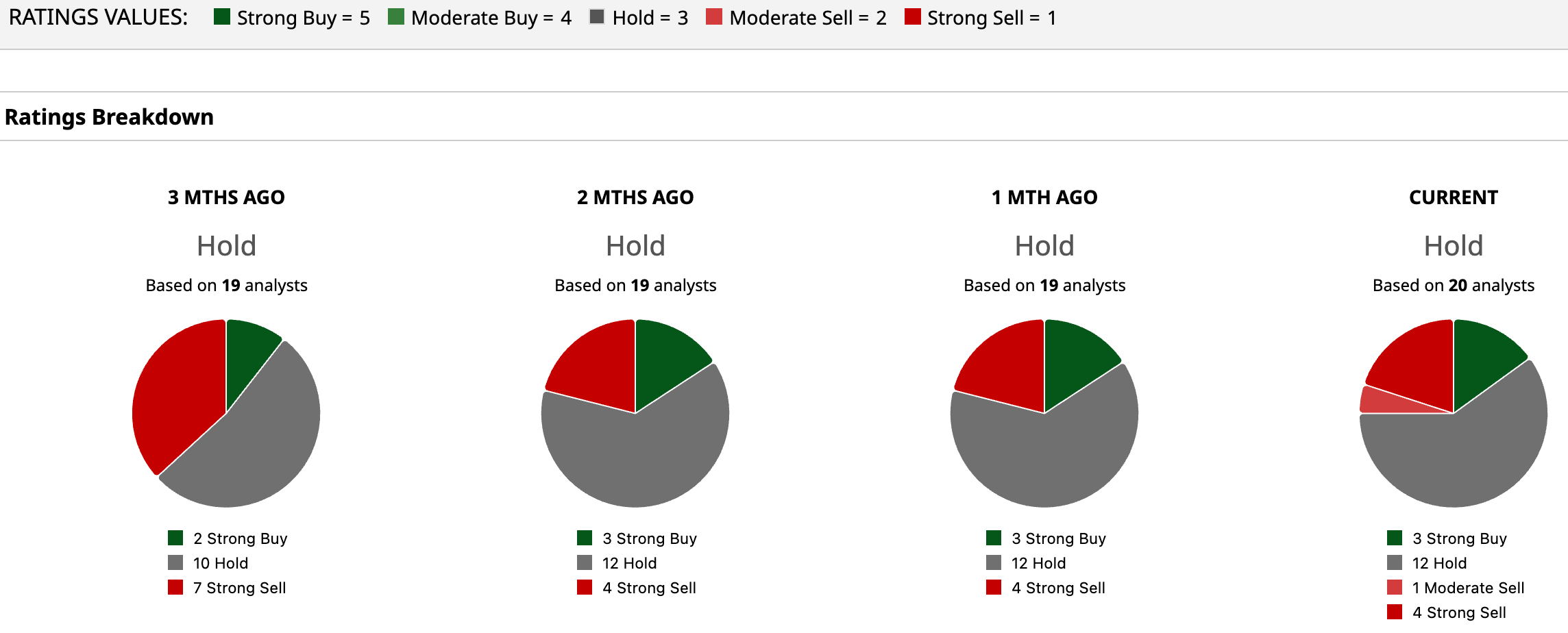

Overall, Wall Street remains cautious on FactSet, with the stock currently carrying a consensus “Hold” rating. Among the 20 analysts covering the name, only three rate it a “Strong Buy,” while 12 prefer to stay on the sidelines with a “Hold.” One analyst has issued a “Moderate Sell,” and four have gone as far as assigning a “Strong Sell” rating, highlighting the divided sentiment surrounding the stock.

Nevertheless, price targets tell a more optimistic story. The average target of $298.44 implies roughly 44.4% upside from current levels, while the Street-high estimate of $425 suggests a potential rally upwards of 105.7%.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart