Netflix (NFLX) shook up the media and entertainment industry last year when it announced the acquisition of Warner Bros. Discovery’s (WBD) studio and streaming assets, intending to unite major content libraries like HBO with Netflix’s global platform. Recently, Netflix modified the deal to an all-cash transaction, offering roughly $27.75 per WBD share. However, the deal has now sparked a bidding war with other suitors like Paramount Skydance (PSKY) raising offers and triggering regulatory reviews and political scrutiny. This has led investors to raise concerns about debt burden and integration risk.

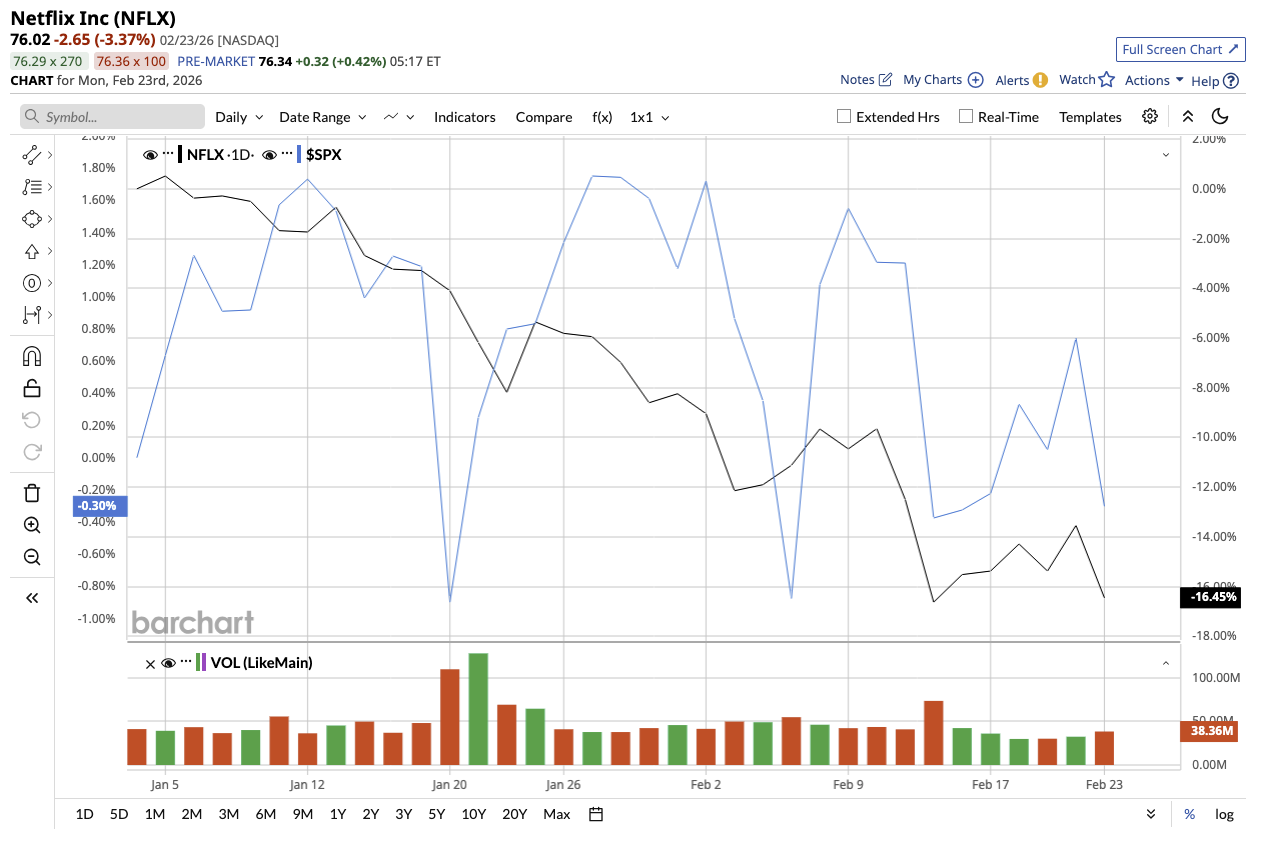

Netflix’s stock has taken a hard hit as investors weigh whether the acquisition will ultimately go through. NFLX stock is down 19% so far this year and down 43% from its 52-week high. However, Netflix’s fundamentals remain rock solid and show no signs of weakness. So is this dip a rare buying opportunity for long-term investors who can ignore the noise?

A Media Superpower in the Making

After years of dominating the streaming wars, Netflix finds itself in a tough spot as the stock has pulled back despite the company reporting solid earnings and continued subscriber growth for 2025.

In the fourth quarter, total revenue increased 18% year-over-year (YoY) to $12.05 billion, while diluted earnings per share rose 31% YoY to $0.56. For the full year 2025, paid memberships crossed 325 million, resulting in a 16% YoY revenue increase of $45.2 billion. While its advertising business is still in early stages, it is growing rapidly. Ad revenue grew more than 2.5x, surpassing $1.5 billion. Operating margin expanded to 25% in Q4 and 29.5% for the full year.

Netflix ended the year with $9 billion in cash and $14.5 billion in gross debt but also generated $9.5 billion in free cash flow. It implies the company is in a manageable position given its scale and profitability. Management anticipates sustained growth in 2026, with revenue increasing from 12% to 14% to between $50.7 billion and $51.7 billion. Ad revenue could nearly double to $3 billion, with the operating margin increasing to 31.5%. Netflix is also expanding its ecosystem beyond streaming to include live programming, gaming, and video podcasts.

If Fundamentals Are Strong, Why Is Netflix Stock Down?

Even if the deal fails, the bull case for Netflix remains strong. The company is reporting double-digit revenue growth with expanding operating margins even though streaming growth has slowed down due to mature markets. Furthermore, ads are scaling rapidly, and the free cash flow balance is approaching $11 billion.

On the flip side, experts argue that Netflix might be taking an unnecessary risk. After facing intense competition from legacy players like the Walt Disney Company (DIS) and tech giant Amazon (AMZN), Netflix has recently stabilized its financials, which are based solely on organic growth rather than M&A. That suggests the core business alone has meaningful runway.

If Netflix overpays or regulators intervene, the stock could remain volatile for months. And if the deal doesn't go through, investors’ confidence may further suffer. That said, the stock’s recent dip reflects acquisition uncertainty and not weakness in operations.

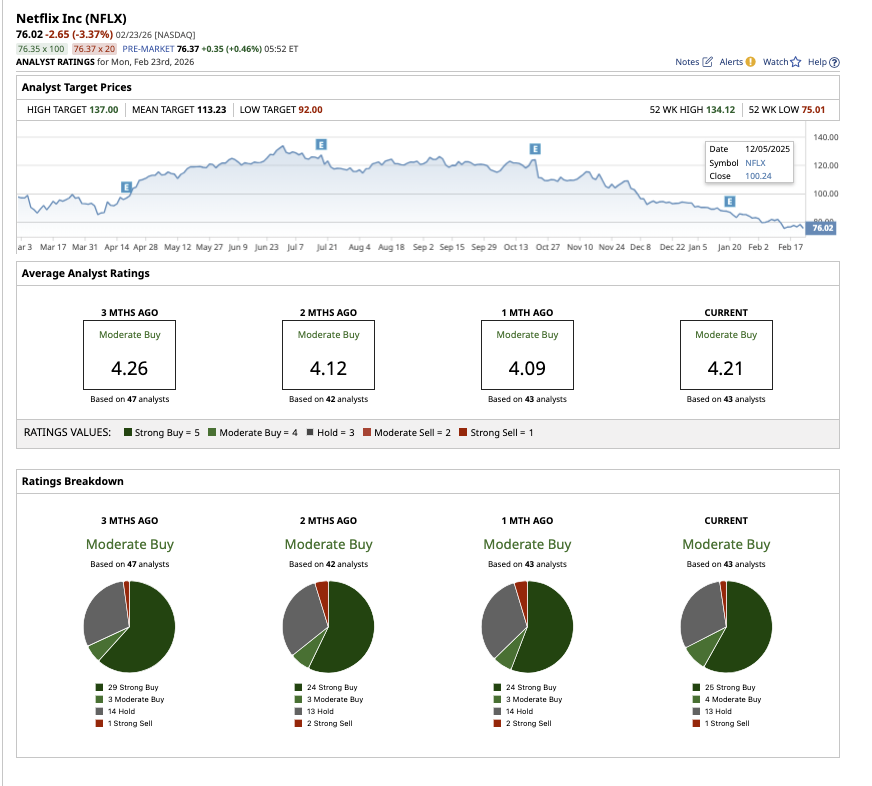

Currently, Netflix’s shares are valued at 24 times forward earnings, which seems reasonable, given that analysts expect earnings to increase by 23.3% and 21.1% over the next two years.

What Does Wall Street Say About NFLX Stock Now?

Overall, Wall Street says Netflix stock is a “Moderate Buy.” Of the 43 analysts covering the stock, 25 recommend a “Strong Buy,” four rate it as a “Moderate Buy,” 13 suggest holding, and one says it is a “Strong Sell.” Based on an average price target of $113.23, Wall Street anticipates a potential upside of around 49% over the next 12 months. The Street-high estimate of $137 indicates the stock could gain as much as 80.2% this year.

The Final Verdict

Netflix, in my opinion, is a profitable, margin-expanding, cash-generating global leader that is choosing to be aggressive from a position of strength. While volatility could persist until a decision is made on the acquisition, this dip may be the last chance for long-term investors before Netflix transforms from a streaming giant to a full-spectrum entertainment empire.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart