Marsh & McLennan Companies, Inc. (MMC), headquartered in New York, is a professional services company that provides advisory services and insurance solutions to clients in the areas of risk and strategy, as well as people worldwide. Valued at $89.6 billion by market cap, the company offers analysis, advice, and transactional capabilities.

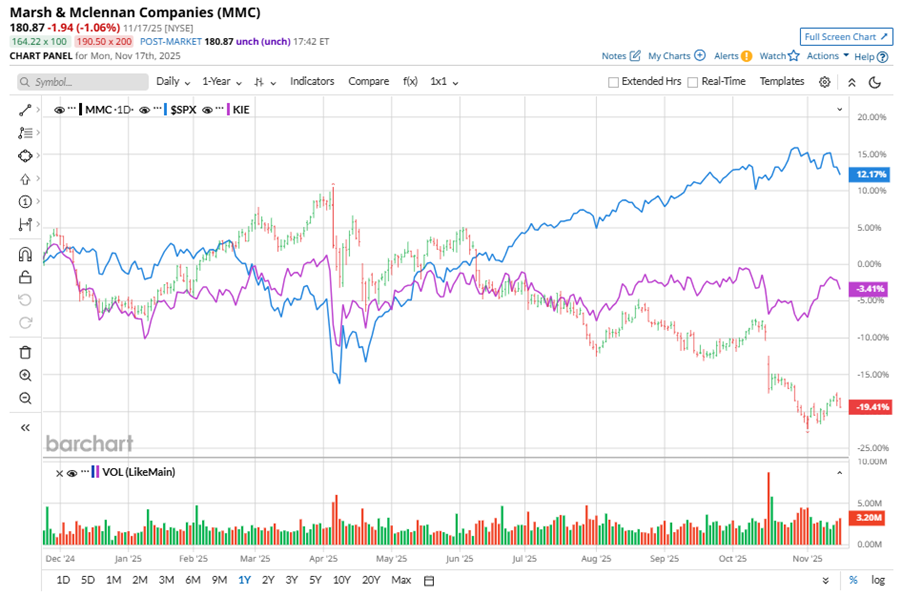

Shares of this leading professional services firm have considerably underperformed the broader market over the past year. MMC has declined 18.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 13.7%. In 2025, MMC’s stock fell 14.9%, compared to the SPX’s 13.4% rise on a YTD basis.

Narrowing the focus, MMC’s underperformance is also apparent compared to the SPDR S&P Insurance ETF (KIE). The exchange-traded fund has declined about 1.9% over the past year. Moreover, the ETF’s 3.2% returns on a YTD basis outshine the stock’s double-digit losses over the same time frame.

On Oct. 16, MMC shares closed down by 8.5% after reporting its Q3 results. Its adjusted EPS of $1.85 exceeded Wall Street expectations of $1.79. The company’s revenue was $6.4 billion, topping Wall Street forecasts of $6.3 billion.

For the current fiscal year, ending in December, analysts expect MMC’s EPS to grow 9.2% to $9.61 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

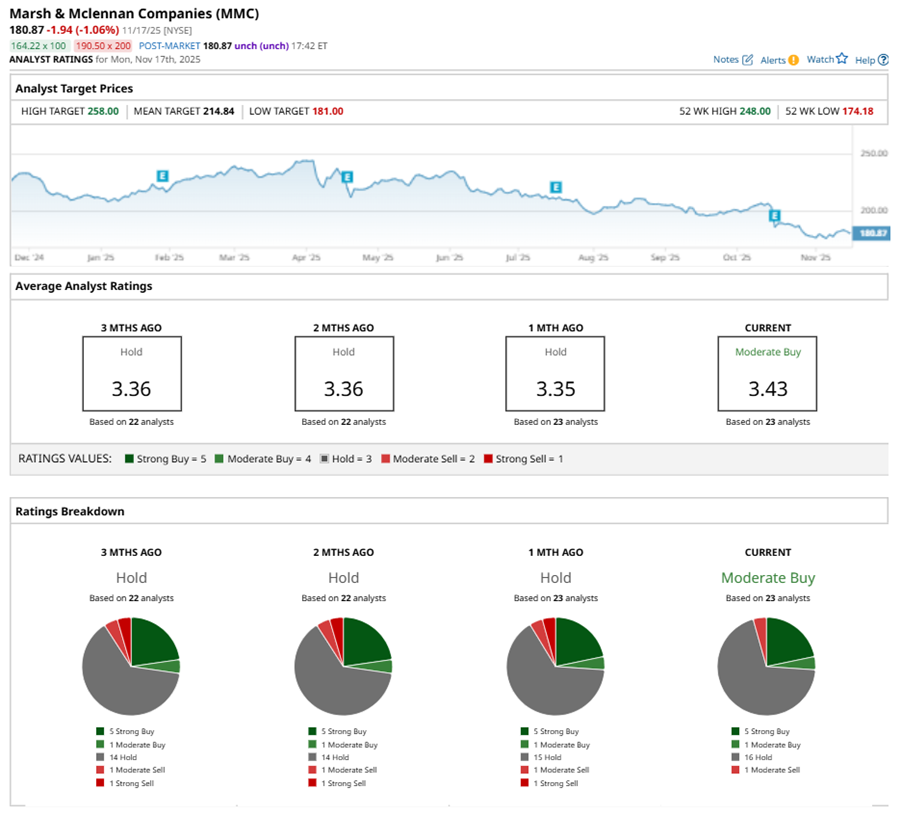

Among the 23 analysts covering MMC stock, the consensus is a “Moderate Buy.” That’s based on five “Strong Buy” ratings, one “Moderate Buy,” 16 “Holds,” and one “Moderate Sell.”

This configuration is less bearish than a month ago, with a “Hold” rating overall, consisting of one analyst suggesting a “Strong Sell.”

On Nov. 3, TD Cowen analyst Andrew Kligerman kept a “Hold” rating on MMC and lowered the price target to $200, implying a potential upside of 10.6% from current levels.

The mean price target of $214.84 represents an 18.8% premium to MMC’s current price levels. The Street-high price target of $258 suggests an ambitious upside potential of 42.6%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- S&P Futures Slip on Souring Risk Sentiment

- Think AI Stocks Are Overvalued? Invest in These Data Center Power Trades for the Next Growth Phase.

- This High-Yield Dividend Stock Is Beaten Down, But Wall Street Still Loves It

- Unusual Options Activity Shows 71,000 Calls Hit the Tape for Applied Digital Stock – How You Should Play APLD Here